Our Network: Issue #57

Coverage on Index Coop, Hegic, PoolTogether, and Nexus Mutual.

Click here to join Our Network Alerts on Telegram.

This is issue #57 of the on-chain analytics newsletter that reaches nearly 8000 crypto investors every week 📈

✨ Together with our partners:

1inch, whose v2 offers the best rates by discovering the most efficient swapping routes across all DEXes—swap on the customizable new UI. And also Aave, where you can experience DeFi: Deposit, Earn, & Borrow on Aave.

This week our contributor analysts cover DeFi: Index Coop, Hegic, PoolTogether, and Nexus Mutual.

① Index Coop

Contributors: LemonadeAlpha & Greg Docter at Index Coop

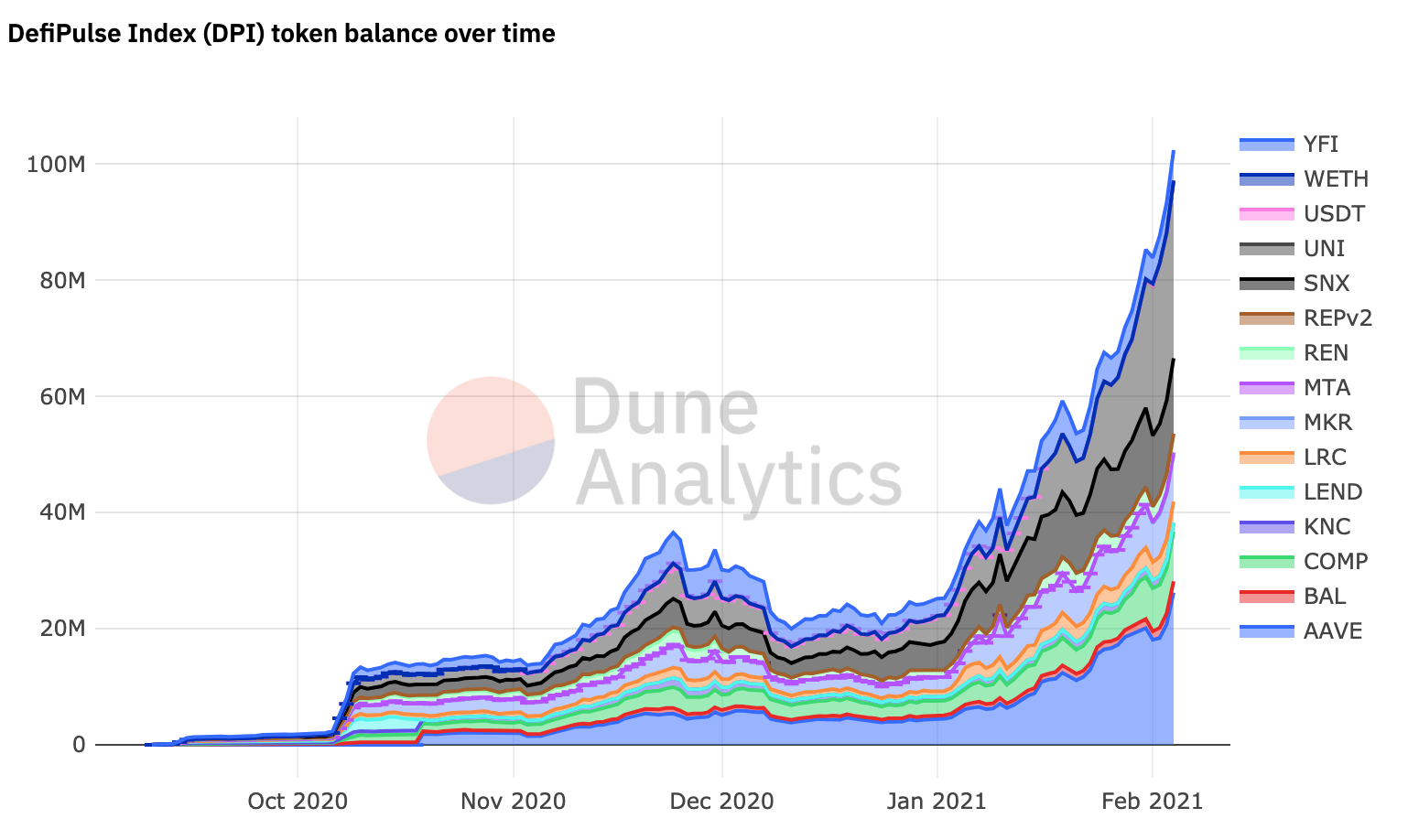

We last updated you two months ago in Issue #49. Since then, the Index Coop’s flagship product, the DeFi Pulse Index (DPI), has continued to gain traction. As of writing, DPI market cap exceeds $117MM, up from December’s $31MM. The number of DPI holders has more than doubled from December and now sits at over 9,200.

The Index Coop is a data-driven community. Three metrics we believe are crucial for understanding the success of products we support are: (1) general retention, (2) unit retention, and (3) unincentivized TVL.

General retention is improving, as DPI appears to be getting more sticky as time goes on. This indicates that DPI holders are now buying DPI for its intended purpose of broad DeFi exposure, rather than yield farming.

We use a metric we call “unit retention” to measure repeat buying behavior; unit retention reveals that DPI owners are increasing their exposure by nearly 70% in the first 50 days after the initial purchase. This behavior further indicates that DPI’s value proposition resonates with its owners.

Unincentivized TVL is also trending positively. Today, nearly 70% of DPI TVL is outside of the Uniswap liquidity mining pool, up from 20% in early December. This data makes clear the demand for DPI absent incentivization. Despite fewer incentives, DPI unit growth continues to increase.

One thing that hasn’t changed since Issue #49 is that liquidity remains a strength of DPI. DPI-ETH liquidity on Uniswap is at an all-time high, and 24-hour trade volume now routinely surpasses $6MM.

② Nexus Mutual

Contributor: Richard Chen, Partner at 1confirmation

Active cover amount reached an all-time high of $667M, which is already almost a 10x growth in covers since the start of 2021! Much of the new cover purchases were from the launch of Armor.Fi, a third-party distributor for Nexus in which users can purchase covers without KYC and soon stream covers in a “pay-as-you-go” model. (Source)

Covers on many DeFi projects are maxed out right now: Balancer, Compound, Curve, MakerDAO, Ren, Uniswap, and Yearn are all around $52M in active covers each. 2.3% of total value locked in DeFi is currently being insured, and the maxed out covers show growing demand for DeFi insurance. (Source)

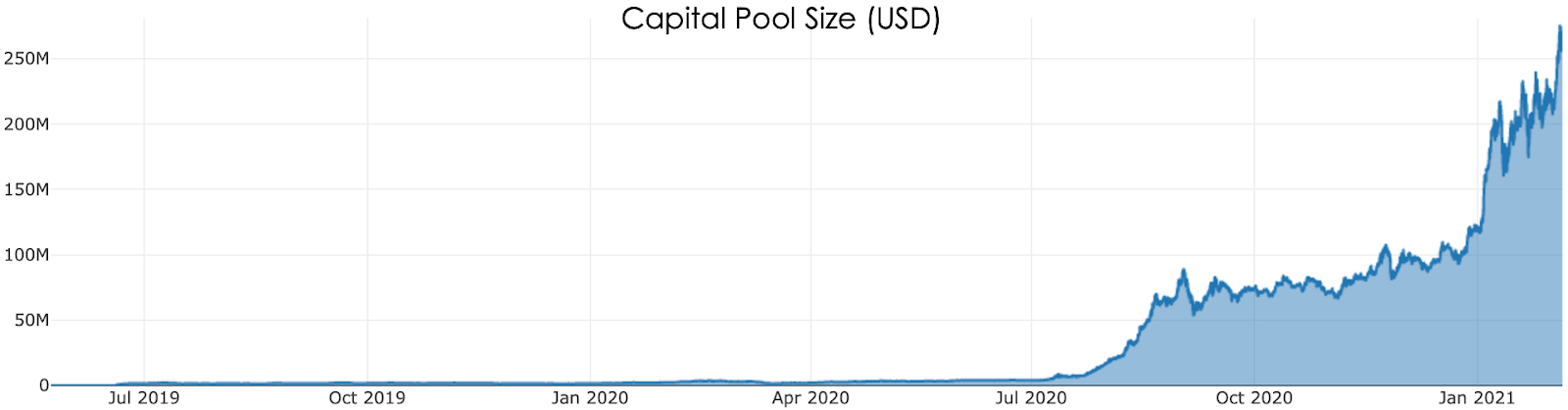

The capital pool size is at an all-time high of $263M. One big advantage of the mutual model for insurance is that it is capital efficient – there can be more active covers than the capital pool that backs potential claims. Nexus is currently leveraged 2.5x and can be leveraged up to 5-6x to underwrite more covers. (Source)

Armor.Fi launched the arNXM vault, which allows users to stake wNXM on projects in Nexus and also not pay gas to claim staking rewards. The arNXM vault opened up more than $250M in new cover capacity, notwithstanding the fact that the vault strategy returns around 52% APY right now. (Source)

Nexus recently launched centralized exchange covers and investment earnings. DeFi is now able to insure deposits in CeFi (e.g. Coinbase, Binance, Kraken, BlockFi, Celsius), while CeFi still struggles to get coverage from traditional insurers. Moreover, investment earnings allows the mutual to invest part of the capital pool in yield generating assets, such as Eth2 staking and on DeFi lending platforms. Insurance companies in traditional finance make most of their revenue from investment earnings, so this is a huge new revenue stream for Nexus and value accrual for NXM.

③ PoolTogether

Contributor: Leighton Cusack, Core team at PoolTogether

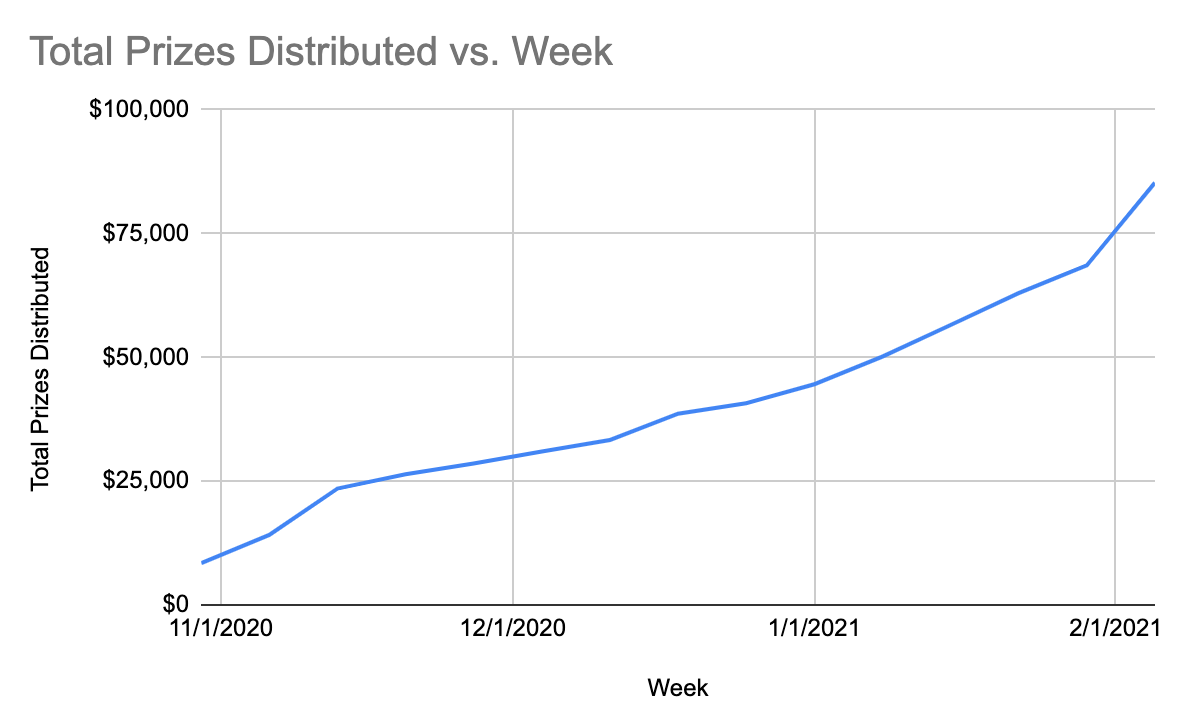

PoolTogether is a protocol for no-loss prize games. It enables depositors to have a chance to win large prizes without risking their deposit. A key metric is total prizes distributed by the protocol. The V3 of the protocol has been live for 15 weeks and has distributed over $85,000 in total prizes. The pace of prize distribution is accelerating with an all time high this week of $16,679 putting the protocol on track to distribute over $800,000 in prizes this year.

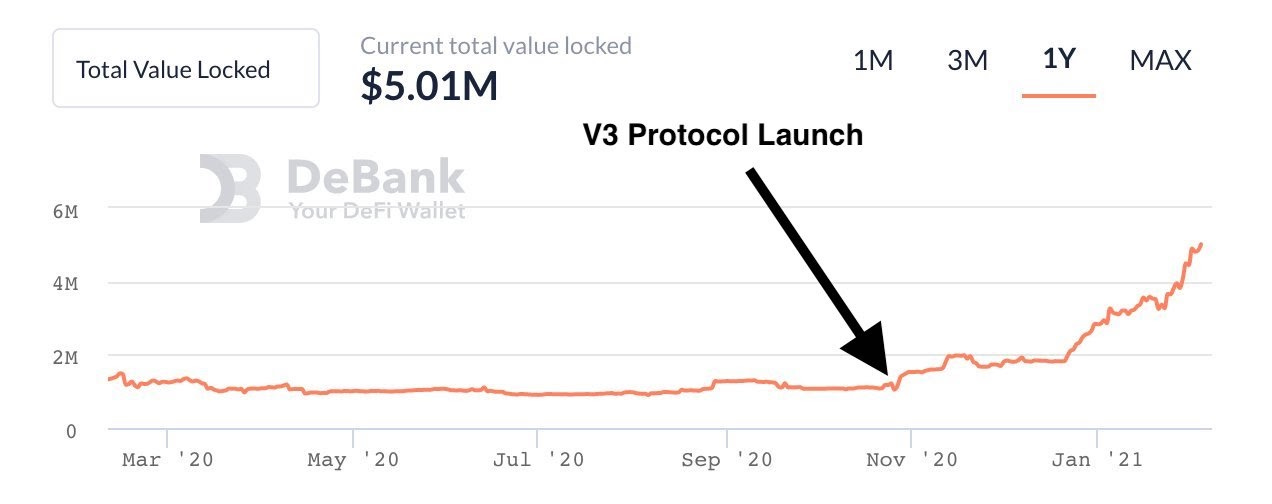

The prizes are derived from earning yield on deposited funds; therefore, a second key metric is the total amount of deposited funds. This has increased rapidly in the 15 weeks since the V3 launch just crossing $5 million this week.

The final key metric for the protocol is unique wallets holding deposits. On this metric, the protocol continues to be one of the most popular in decentralized finance. In the first 15 weeks, the Dai Prize Pool has grown to 3,718 unique wallets deposited. For comparison, there are currently 1,388 unique wallets holding V2 Aave Dai and 16,067 wallets holding Compound Dai which has been available for 12+ months.

The PoolTogether protocol enables anyone to permissionlessly add their own prizes to a pool. This has become a popular way for protocols to introduce their tokens to a new audience. In the current prize (below), $3,714 of value has been contributed by these permissionless prizes. Since its launch, a total of $17,572 in prizes (20% of all prizes awarded) have been added in this way.

The protocol enables permissionless prize pool creation. This means anyone can create a no-loss prize pool in the same way anyone can create a Uniswap trading pair. The first protocol utilizing this is Barn Bridge, creating a no-loss prize pool for their $BOND token. Launched four days ago this prize pool has $280,000 (~3,600 BOND token) deposited.