Our Network: Issue #49

Coverage on Lending Rates, Compound, INDEX Coop, and Balancer.

Our Network is now live on Gitcoin Grants! Donations very much appreciated.

This is issue #49 of the on-chain analytics newsletter that reaches nearly 6500 crypto investors every week 📈

✨ Together with our partners:

1inch, whose v2 offers the best rates by discovering the most efficient swapping routes across all DEXes—swap on the customizable new UI. And also Aave, where you can experience DeFi: Deposit, Earn, & Borrow on Aave.

This week our contributor analysts cover DeFi: Lending Rates, Compound, INDEX Coop, and Balancer.

① Lending Rates

Contributor: Lucas Campbell, Analyst at Bankless

DeFi continues to offer high yielding interest rates for crypto dollar depositors. Even the most battle-hardened interest rate protocols dwarf traditional finance and create a compelling alternative to the negative interest rate environment we currently live in. You throw in additional subsidies from yield farming and it’s not even close.

The two major interest rate protocols, Aave and Compound, offer lower rates on DAI than some of the other players with 4.2% and 3.1% APY, respectively. However, when you factor in COMP incentives (2.4%), the DAI lending rate on Compound beats out Aave at 5.5% APY. With that said, Aave just launched V2 and will soon introduce AAVE yield farming into its money markets.

In terms of borrowing DAI, Maker continues to act as one of the best sources for leverage in the ecosystem. Users can collateralize ETH at a low APY of 2.00% or WBTC for 4.00%, making lending on other third party protocols a profitable opportunity. Similar to above, Compound also offers an interesting place to borrow DAI as users effectively receive a 3% “cash-back” in COMP, driving down the real rate to 1%.

On average, USDC rates are higher on all protocols when compared to DAI. dYdX and Aave both offer high annual yields of 6.9% and 5.0%, respectively, while Compound only gives depositors 3.7% APY. Again when factoring in the COMP subsidy, USDC rates rise to over 6% on Compound.

U.S. crypto bank BlockFi is also in the mix as it offers depositors 8.6% APY on USDC. It’s important to note that BlockFi actually lends out your capital, meaning there’s an additional risk for loans to default — something that’s not necessarily associated in DeFi as all loans are over-collateralized by the borrower.

Lastly, we have ETH. Despite the launch of Eth2 staking earlier in the week, interest rates haven’t budged much (if at all). This is something that will likely change as Eth2 staking becomes more accessible and tokenized staked ETH becomes liquid on the Eth1 chain, driving lending rates and staking rates closer to parity. With that, there are only two places that are offering anything remotely attractive for ETH depositors: BlockFi and Bitfinex. While the 30-day averages for both firms seem close, BlockFi recently raised ETH deposit rates to 5.25%, beating out Bitfinex at 4.5%.

In terms of borrowing ETH, there are some compelling options out there. dYdX and Aave both offer cheap rates for borrowing ETH with the lowest 30-day average being dYdX at 0.5% APY while Aave sits at 1.5%. The dark horse here is Compound. At current rates, anyone can get paid ~0.7% APY for borrowing ETH when you factor in COMP subsidies.

② Compound

Contributor: Nick Martitsch, Business Development Associate at Compound Labs

On November 11th, the total value of assets supplied to Compound surpassed $3B for the first time in the protocol’s history, up from $2.47B at the start of November. Users have added $6.2B of gross supply in the last 30 days, with 43% of this volume in ETH, 24% in DAI, 21% in USDC, and 9% in WBTC. Supply volumes dipped to a low of $2.7B on November 27th after record liquidations in the DAI market, but have since quickly bounced back to $3.3B at the time of writing.

The number of unique Compound users has grown 290% since the launch of Coinbase Earn Advanced Tasks, from 52,035 on October 14 to 225,999 on November 27. 173,655 Coinbase users supplied $3 worth of USDC to Compound, representing nearly 87% of all active users. 23,198 of these users supplied additional assets and 67 borrowed assets, demonstrating how centralized exchanges can be an effective onboarding user mechanism for DeFi protocols.

WBTC supplied to Compound has increased by 967% in the last 2 months, going from 2,120 on October 1 to 22,615 on December 1. cWBTC is now the fourth-largest market on Compound by supply volume and the single largest holder of WBTC among various DeFi protocols. This increase is likely due in part to the Compound community voting to increase the collateral factor of WBTC from 40% to 60% on October 1st, making it a more efficient collateral option for borrowing stablecoins. The rising price of BTC during the current bull run has also likely contributed to this growth, as traders are less concerned about liquidations stemming from the falling price of WBTC collateral.

As a result of Proposal 29, the 12,949,954 market liquidity UNI in Compound is delegated to the community multi-sig, which can vote on Uniswap governance proposals as a block or even create its own proposals. The Compound community multi-sig is now the 4th largest UNI delegate, representing 14.4% of the total voting weight. The 2,233 unique cUNI holders are able to direct the multi-sig on how to participate in Uniswap governance while still earning 2.34% APY on their underlying UNI, showcasing the compatibility of governance tokens held in DeFi protocols.

③ Index Coop

Contributor: Greg Docter, Index Coop community member

The Index Cooperative is a community focused on enabling the creation and adoption of crypto index primitives. The first primitive governed by the Coop is the DeFi Pulse Index (DPI), which launched September 14, 2020. The DPI provides exposure to 10 DeFi assets through a single token redeemable for those same underlying assets.

The DPI is gaining traction. Since November 1, 2020 DPI’s market cap has grown 114% and currently exceeds $31MM. This growth was driven by the increased value of underlying assets, as well as a 20% increase in DPI supply. Further, DPI holders have grown from 1,608 to 3,043 over the same period, according to Nansen. This growth demonstrates demand for a blue-chip, capitalization-weighted DeFi index.

One hypothesis for why DPI adoption hasn’t grown more quickly is that the token is available on only a few exchanges today. Uniswap facilitates the most action. DPI-ETH liquidity on Uniswap is over $47MM, up 97% since November 1, 2020. Trade volume has also increased since that date, when it was just $495,165. As of writing, the 24-hour volume was $2,655,074. These numbers are likely influenced by ongoing farming incentives.

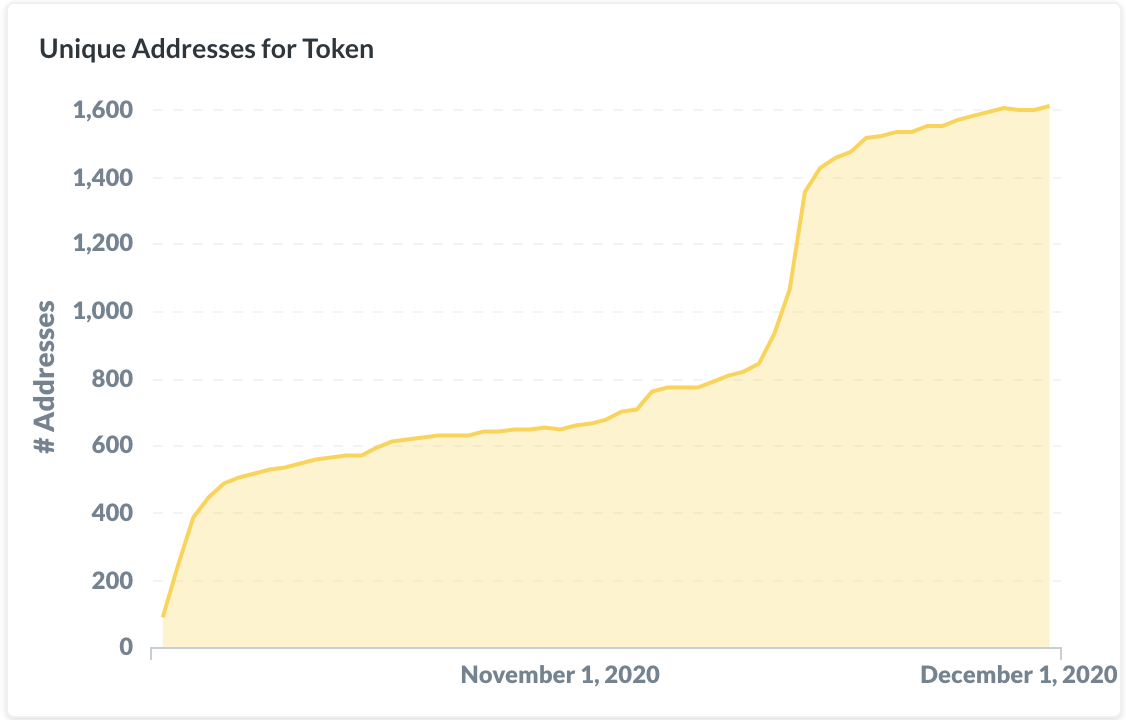

As DPI adoption increases, so does the governance power of the Index Coop and INDEX token holders. INDEX is the Coop’s native token that enables community ownership and governance. There are over 1,600 INDEX holders today who can guide DPI voting power in certain protocols’ governance. For example, DPI was the 3rd largest voter on Aave’s two most recent proposals and is already #17 on Compound's governance leaderboard.