Continued from Part 1.

(Decred, cont.) Similar to On-Chain Balance, we can track the volume-weighted average purchase price of Decred tickets over a period of time. During bullish markets, where demand for tickets is strong, these moving averages will 'keep pace' with price as larger volumes of DCR are pushed into staking.

This manifests as values of TVWAP ratio close to 1.0 which generally support bullish sentiment. The 14-day and 28-day TVWAPs are following price extremely closely whilst the 142-day TVWAP is reversing from the lowest value since June 2017. This indicates a strong increase in recent demand for staking DCR, turning around the slower long period TVWAP Ratio.

Staking within the Decred ecosystem is a pseudo-random timelock of value representing “skin in the game”. Stakers relinquish coin liquidity to secure the network and voting rights in return for a share of the block reward.

The charts below track the USD & BTC prices where DCRs have been staked over the network’s lifetime. By analyzing this data, we can track potential profit, loss, and breakeven levels for Decred’s biggest bulls.

Only 17% of DCR ever staked has occurred above $40, signaling DCR stakers are currently in reasonable profit on a USD basis.

Staker breakeven level is around ~.004 DCR/BTC. Above this level, approximately 60% of stakers will be in profit on a BTC basis.

⑤ Polkadot

Contributor: Bill Laboon, Technical Education Lead at Web3 Foundation

Polkadot’s staking system consists of validators (block-producing nodes) and nominators (accounts which provide stake). The number of validators have been increasing, by acts of on-chain governance, on both Polkadot and Kusama (Polkadot’s “canary network”). Polkadot currently has 297 validators in the active set, with 400 other potential validators. Kusama currently has 897 validators in the active set, along with 383 waiting. There are 6,975 accounts nominating on Polkadot, compared to 3,146 on Kusama. Approximately 59.6% of all DOT (~ 619,040,872) are currently locked in staking, compared to 49.1% (~ 5,209,416) of all KSM on Kusama. There is therefore a mean 2,084,312 DOT backing each validator, ranging from a low of 1,668,791 DOT to a high of 3,995,259 DOT. On Kusama, there is a mean of 5,833 KSM backing each of the 897 active validators, with stake ranging between 3,351 KSM and 25,558 KSM.

Polkadot can modify the blockchain using on-chain governance, from small changes such as increasing the number of potential validators to replacing the actual runtime code. Polkadot stakeholders are currently voting on its fifteenth referendum, with ten having passed, three failed, one cancelled, and one ongoing. Kusama, which has a faster voting cycle and has been running for longer (over 5.9 million blocks compared to Polkadot’s approximately 3.5 million blocks) is on its 99th referendum.

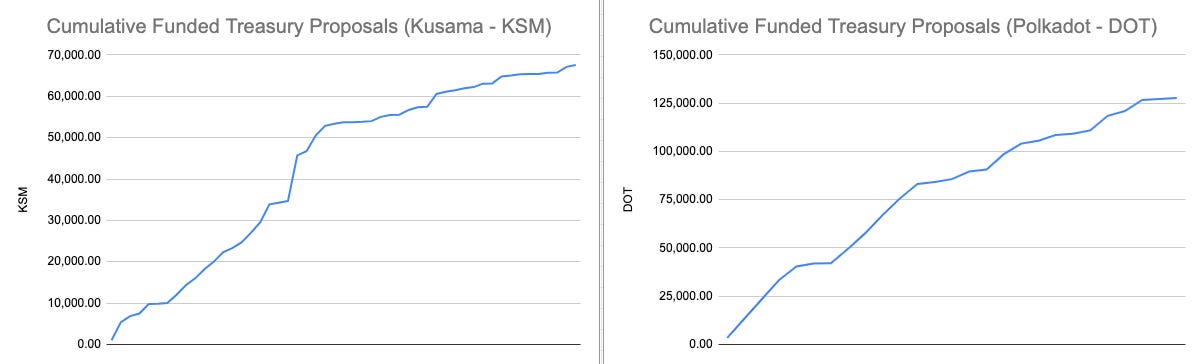

The Polkadot and Kusama treasuries receive funding from network activity. Users of the network can make Treasury Proposals to improve the ecosystem, which are then approved by the Polkadot Council. The Kusama Council has approved 67,550.89 KSM for various projects, and the Polkadot Council 127,622.06 DOT. Over 50% of the funding has been used for infrastructure deployment and maintenance of various common good software. Approximately 70% of accepted Polkadot proposals have successfully completed their milestones, and approximately 68% of all accepted Kusama proposals. As of this writing (29 Jan 2021), there is ~ 11,382,800 DOT available in the Polkadot Treasury and ~ 279,087 KSM available in the Kusama Treasury.

Activity has been steadily increasing on both networks. There have been over 2,000 new accounts created and over 5,000 transactions processed on Polkadot every day for the last 30 days. Kusama has had fewer daily new accounts and transactions - around 250 and 1,400 on average, respectively - over the last 30 days. (Info courtesy of polkascan.io)