Our Network: Issue #56

Coverage on BTC, ATOM, ETH, DCR, and DOT.

Click here to join Our Network Alerts on Telegram.

This is issue #56 of the on-chain analytics newsletter that reaches 7500 crypto investors every week 📈

✨ Together with our partners:

1inch, whose v2 offers the best rates by discovering the most efficient swapping routes across all DEXes—swap on the customizable new UI. And also Aave, where you can experience DeFi: Deposit, Earn, & Borrow on Aave.

This week our contributor analysts cover L1 Blockchains: Bitcoin, Cosmos, Polkadot, Decred, and Ethereum.

① Bitcoin

Contributor: Nate Maddrey, Researcher at Coin Metrics

Throughout 2020 large companies including PayPal, Square, and MicroStrategy announced their involvement with BTC. But since the beginning of 2021, institutional interest appears to have jumped up to a new level. The amount of addresses holding large amounts of BTC (at least 1000) has soared since the start of the year to new all-time highs.

These large BTC holders are gobbling up more and more of the total supply. Addresses with at least 1K BTC now hold close to 30% of total supply. This is most likely good for the long-term stability of BTC supply - large institutions are typically long-term investors who will hold their position for many years.

Somewhat surprisingly, the percent of supply held by relatively small addresses is also increasing. Addresses holding between 0 and 1 BTC now hold close to 5.1% of total supply. The amount held by addresses holding 1-10 BTC has also increased, to about 9.4% of total supply. While large holders are accumulating, supply is also becoming more distributed amongst retail-level investors.

Looking at HODL waves gives a picture of how BTC’s supply has moved on-chain during the current run. HODL waves are created by grouping BTC’s supply by the age it was last moved on-chain, or in other words, the age that it was last sent as part of a transaction. Throughout early 2021 there’s been an uptick in the amount of supply that’s held for relatively short periods (180 days or less). But the amount of BTC held for 3 years or longer has actually increased since mid-2020, which shows that there’s a growing number of truly long-term holders.

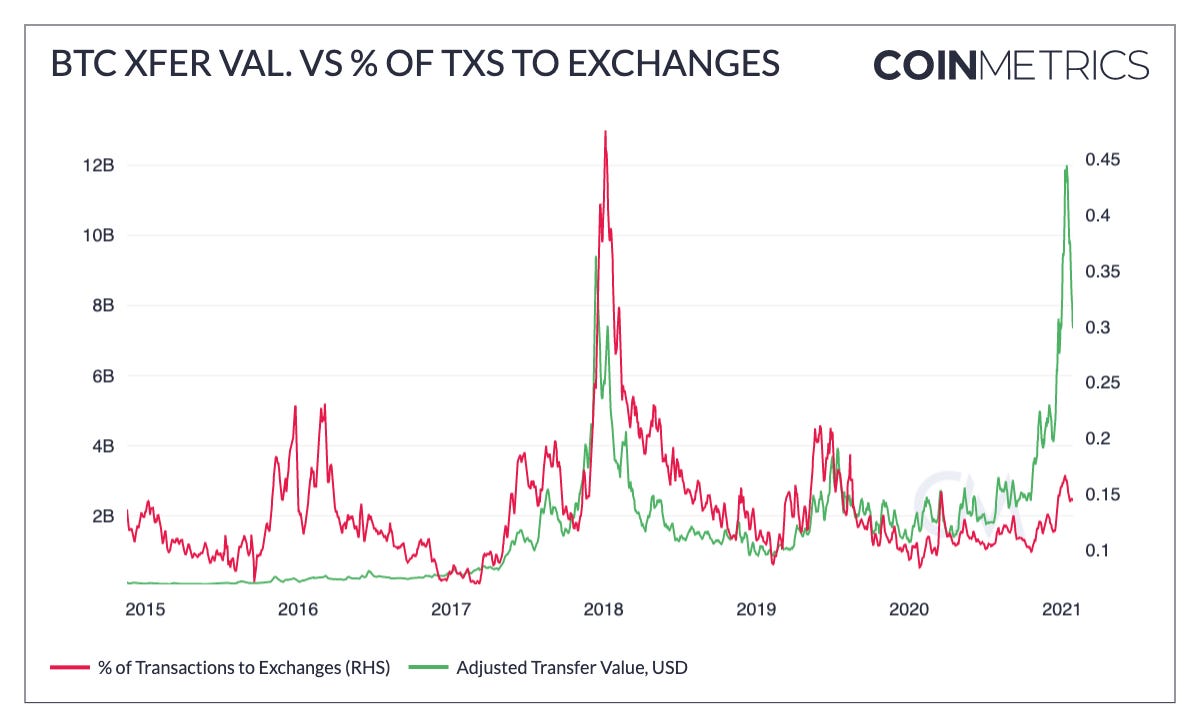

BTC on-chain activity has also surged to new heights. On-chain transfer value (adjusted to remove self-sends and other noise), shown on the left-hand side of the below chart, has reached new all-time highs in early 2021. But the percent of total BTC transactions sent to exchanges (right-hand side) has not grown with it - only about 15% of BTC transactions are being sent to exchanges in early 2021 compared to over 45% during the peak of the 2017 bull run. This is perhaps due to the fact that institutions are increasingly purchasing BTC through OTC desks and other platforms outside of the major exchanges, and signals that retail interest is still just ramping up.

② Ethereum

Contributor: Alex Gedevani, Researcher at Delphi Digital

During the 2017 bull market, fulfilling ICO demand was arguably ETH’s biggest use case. Unsurprisingly, when the music finally stopped, the price of ETH tumbled. Fast forward three years and the % of ETH supply held in smart contracts has increased by 49% to 18.5%. What’s driving this? The massive growth in DeFi, primarily, has led to 7 million ETH in total value locked (TVL). A few factors driving this are demand to use ETH in dApps for yields and Eth Phase 0 staking, which accounts for 2.9 million deposited ETH. Similarly, the chart highlights the shift in ETH’s evolution towards becoming a productive capital asset with yield. Put simply, there is a more sustainable foundation this cycle with clear demand for usage of ETH as DeFi grows.

A network’s ability to generate fees is key for long term sustainability and network security. In January, Ethereum generated more network fees ($285m) than 2017-2019 combined ($242m); annualized fees are now ~$3.7bn. This is a great sign considering EIP-1559 with the fee burn is coming. Miners, however, are against the EIP since the base fee being burnt on transactions will reduce their expected revenue. Nevertheless, we find the pick up in dapp fees to be another healthy indicator; popular AMMs like Uniswap and Sushiswap are holding their own with 7-day average fees $2.3m and $1m, respectively, relative to Bitcoin’s $2.8m.

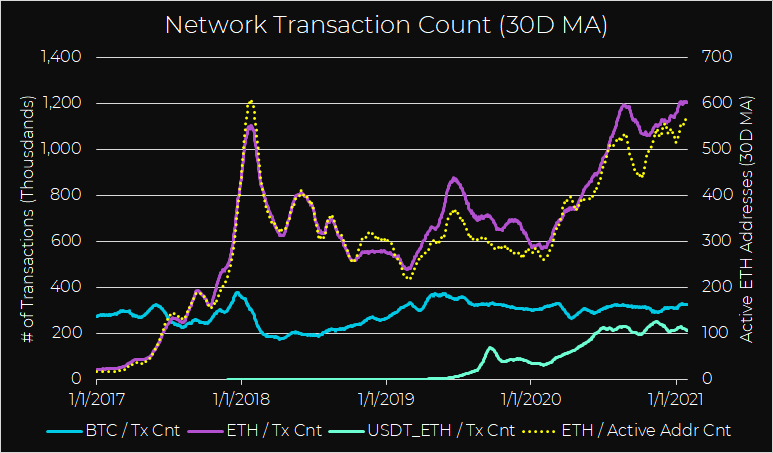

Looking at the transaction counts of large assets like ETH, BTC, and USDT can give an indication of network adoption, but it’s not always apples to apples. ETH tx counts have hit all-time highs at 1.2m over 30 days (notice the strong correlation between transactions and active addresses). This suggests a healthy balance of network utilization. BTC’s lower tx count is expected as it’s more centered around the SoV argument while stablecoins like USDT have seen a sharp rise in transactions, up 204% since early 2020. ETH has separated itself from the pack in this regard with total transactions on Ethereum outnumbering BTC + USDT combined by 123%.

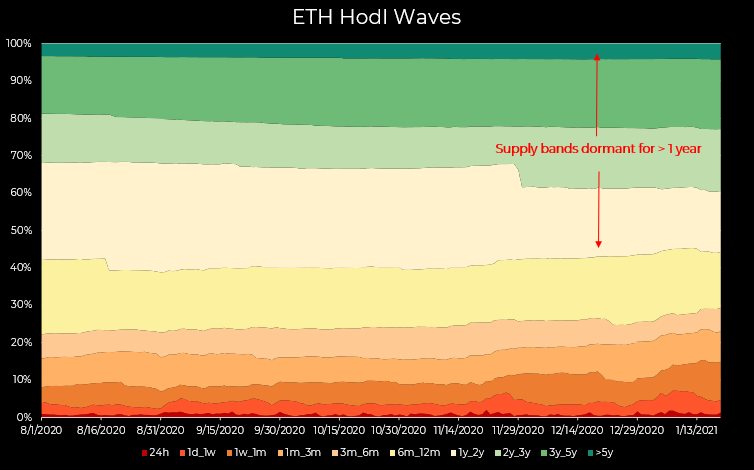

With the markets heating up, it’s important to keep track of the supply sinks for ETH and monitor any longer dated changes in bands.The most noticeable change in hodl waves has been a decline from 29% to 16% for the 1y-2y age band. 56% of the ETH supply hasn’t moved in over a year. Other variables contributing to the supply sink are ETH staking and ETH TVL in DeFi.

③ Cosmos

Contributor: Griffin Anderson, Partnerships at Tendermint

In January 2021, the bonded rate for ATOMs dropped from above 71% to below 67%, leaving many in the industry to speculate about the cause. Some attribute the unbonding of ATOMs to traders realizing gains from recent moves in ATOM’s price. While others attribute the drop in bonding rate to a recent trend around selecting validations that are more in alignment with personal voting preferences. No matter the real reason, the ecosystem is closely monitoring the bonding ratio.

Going strong into 2021, the Cosmos ecosystem is continuing to see an influx of new wallets created that contain at least some ATOMs. Highlighted in late 2020, the vast majority of these addresses are still coming from centralized exchanges. Coinbase and Binance continue to lead in new address creation. This is largely seen as a sign of more speculators entering the space than developers. As the Cosmos ecosystem matures, we will continue to monitor the origination place of these new accounts as a sign of ecosystem maturity.

Voting Power continues to consolidate around the top 10 largest validators. As of January 2021, Binance continues to be the #1 validator on the Cosmos Hub by stake-weight, followed by DokiaCapital and Stake.Fish. It is very important for a mature network to have a strong distribution of voting power among its validators. Therefore, the Cosmos Hub will continue to closely monitor the voting power of all ecosystem participants and encourage new stakeholders to play a more active role in the ecosystem.

④ Decred

Contributor: Checkmatey and PermabullNino, Contractors for Decred

Decred is a hybrid Proof-of-Work + Proof-of-Stake network, and with this comes fascinating on-chain supply and demand dynamics. The On-Chain Balance is a tool developed to measure the portion of issuance (PoW+PoS block rewards) that flows into tickets over a 30-day period.

In 2017, there were three large positive spikes in On-chain Balance (greater flow into tickets than PoW+PoS issuance), which all supported an appreciation in price. 2020/2021 has seen five such spikes with a net overflow of 460k DCR into tickets. Most recently, On-chain Balance has seen the largest ever relative inflow to tickets supporting a doubling in DCR/BTC price.