📝 Editor’s Note:

Coming to you from beautiful Buenos Aires, where the OurNetwork team has enjoyed Devconnect, DuneCon and more, welcome to this week’s issue of OurNetwork.

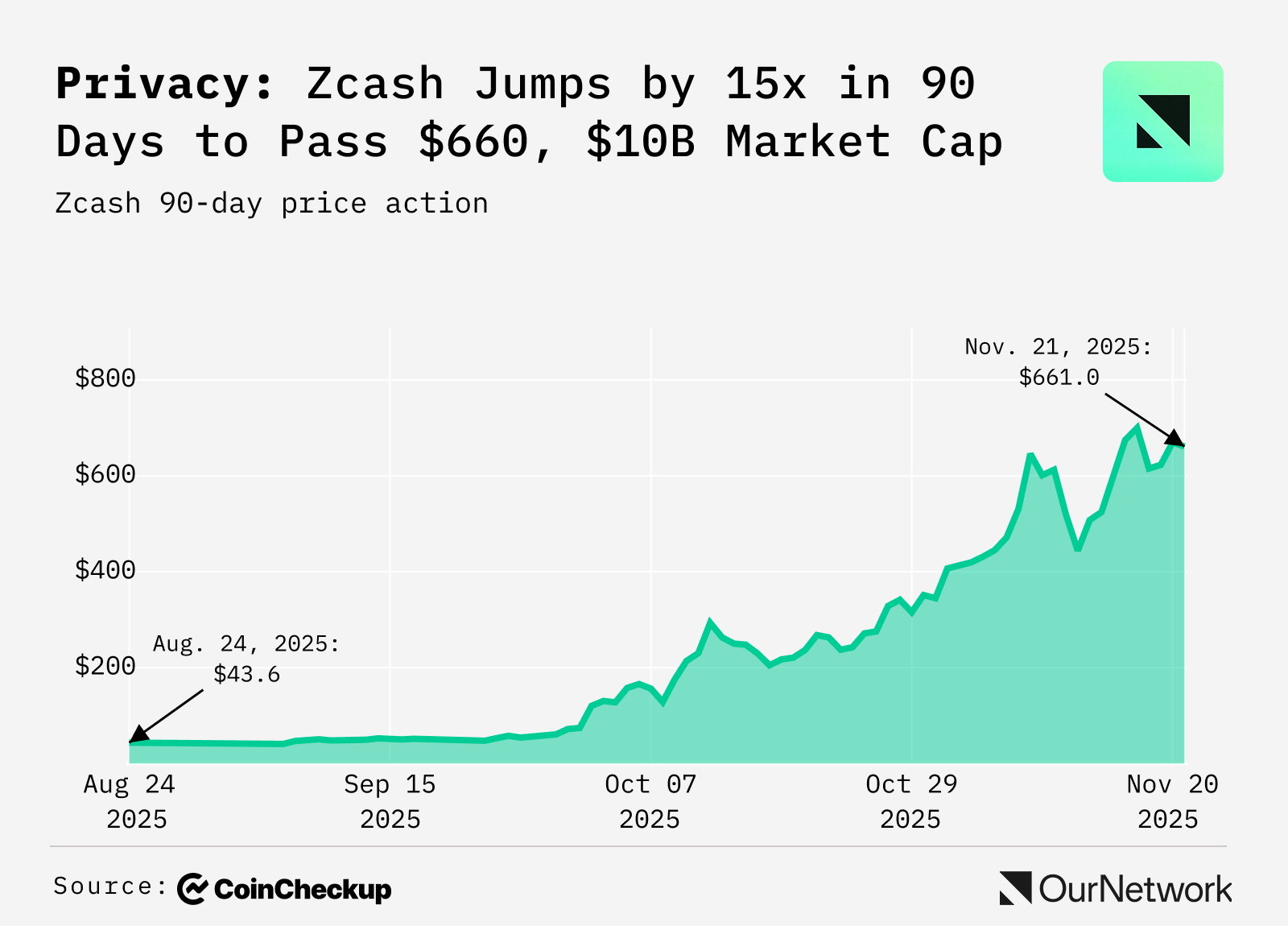

This one takes a look at privacy, a sector which pushed into the spotlight in part because of the rise of Zcash, a token launched in 2016, which has jumped by 15x in the past 90 days to become a top 20 crypto asset by market cap.

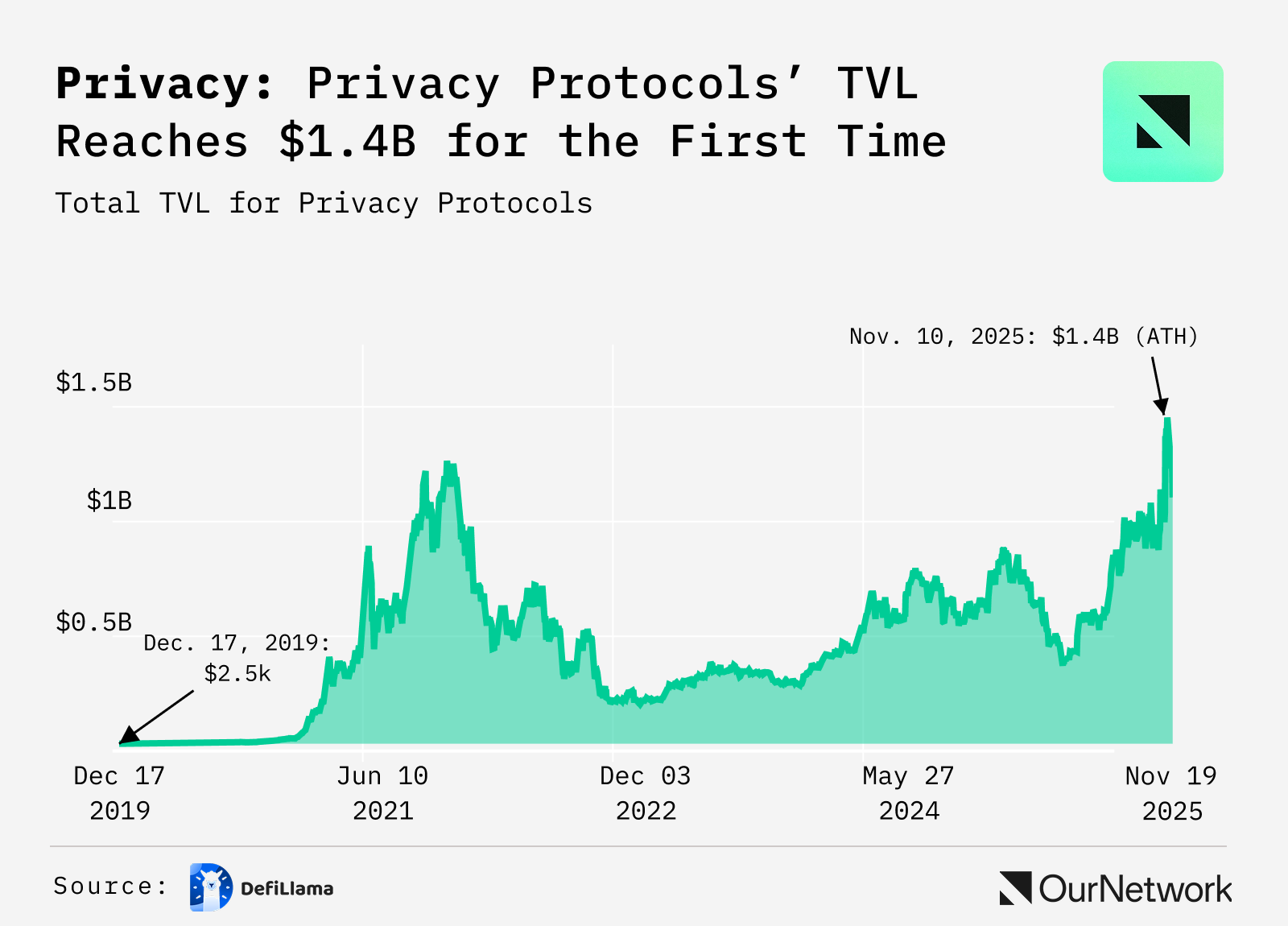

It’s not just Zcash however. Privacy protocols’ total value locked reached an all-time high of $1.33B on Nov. 11, according to DefiLlama. Leading that growth is Tornado Cash, a mixing protocol, Railgun, a privacy protocol, and Aztec, the Layer 2. Together those comprise over 99% of privacy protocols’ TVL, again according to DefiLlama.

That the top protocols encompass such different use cases hints at a major theme in privacy: it’s not as simple as hidden transactions. Privacy is about controlling identity and minimizing revealed data, features which enable regulated actors and institutions to operate with the precision their onchain operations can require.

In this issue, we’re lucky to have Surf Query and Seoul Data Labs dig into the onchain latest of Zcash and Railgun, two leaders in the resurgent privacy space.

Let’s dive in.

– ON Editorial Team

Zcash | Railgun

Zcash 🕵🏻♂️

👥 Surf Query | Website | Dashboard

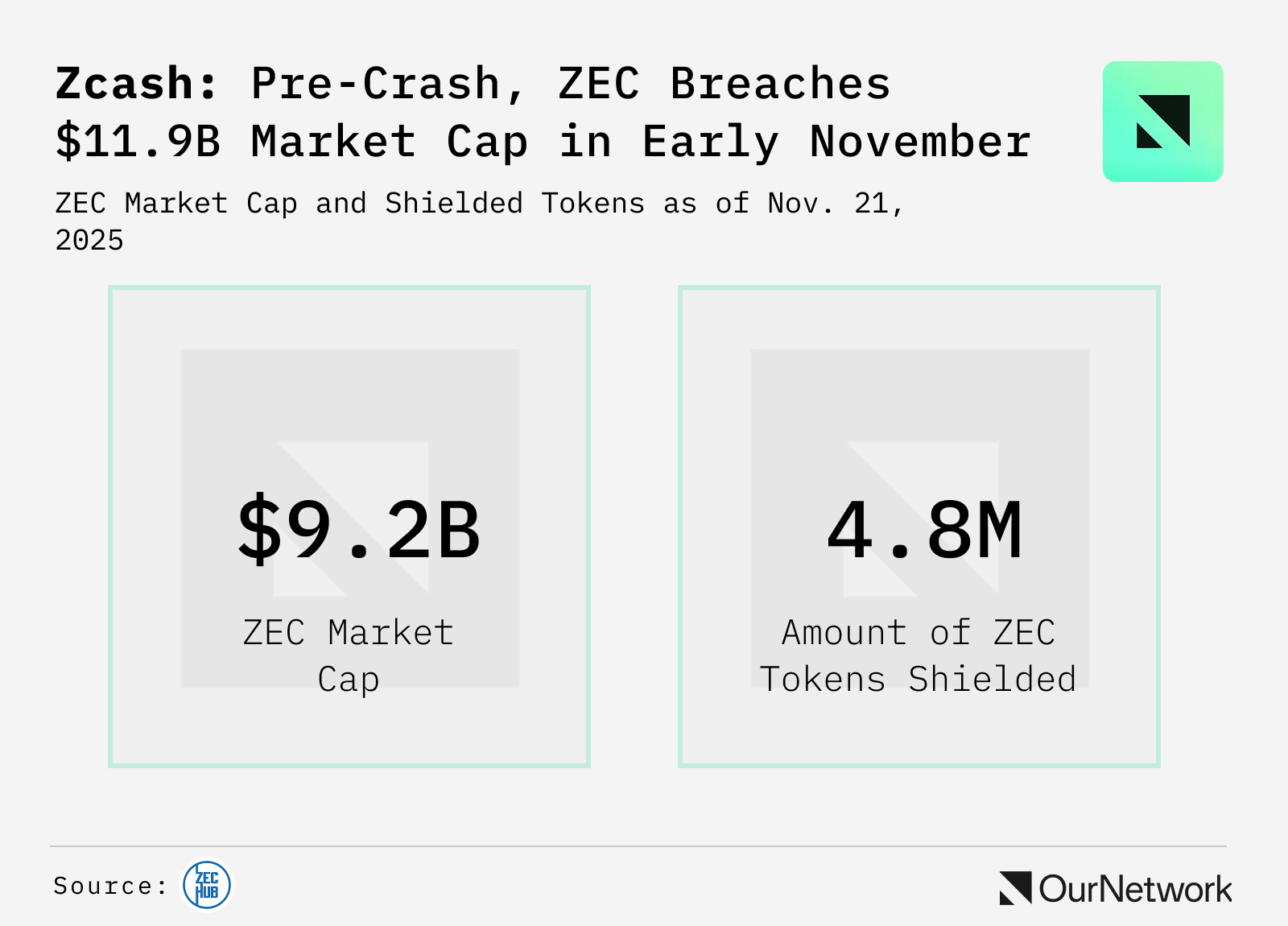

📈 Growing Zcash Activities Reveal Growing Demand for Privacy Through ZK-Snarks Technology

Zcash is a privacy-first cryptocurrency, like Bitcoin but with anonymous transactions. That’s possible with zk-SNARK tech, proving validity without revealing details. Now people can shield funds (using private z-addresses that hide sender, receiver, and amount, via encryption) and transfer with privacy, or choose transparency for audits. As of today, Zcash has processed over 2.4M transactions, with over 4.8M ZEC in shielded supply.