About the editor: Spencer Noon is an independent crypto investor.

EXCLUSIVE ONCHAIN COVERAGE:

DeFi 🫧

① Curve Finance 🌈

👥 nagaking | Website | Dashboard

📈 crvUSD approaches $122M supply, minimizes liquidations during market volatility

Despite significant market volatility, crvUSD has continued to grow through August, with total supply reaching a new all-time high of 122 million. The wstETH market continues to dominate with a total size of $60M (debt cap: $150M), followed by wBTC ($28.7M; $200M cap), sfrxETH ($9.9M; $10M cap), and wETH ($7.2M; $200M cap). Across crvUSD markets, the total debt cap is 560M, allowing for future expansion of crvUSD's total supply.

crvUSD continues to be a reliable source of income for the Curve DAO, with weekly revenue rivalling the combined trading fees from all non-ETH chains. Over the last few weeks, weekly revenues for crvUSD have been in the $15k-$93k range.

In August, volatility produced widespread liquidations in crypto markets. Long term stats show crvUSD borrowers were largely insulated from liquidation. (a) Across crvUSD markets, ~85% of users had 0 loss, (b) Median losses were ~2% for losing positions, (c) Soft liquidations were limited to <18%.

💦🔬 Tx-Level Alpha: Here, a user deposits 24.99 wBTC and borrows 350k crvUSD, increasing their total collateral to 1.9k WBTC ($48.17M) and total borrow to 28.06M crvUSD. This tx demonstrates crvUSD's ability to serve even very large crypto holders.

② MakerDAO 🏗️

👥 Sébastien Derivaux | Website | Dashboard

📈 MakerDAO’s RWA investments provide 56.7% of revenue

MakerDAO issues the DAI stablecoin, which users can stake to earn a saving rate (DSR, currently 5%). Both DAI and DSR represent capital that Maker can invest. Initially, MakerDAO mainly used this capital to fund crypto-backed loans (CDPs). It then migrated to invest mainly in stablecoins to maintain the peg, and is now moving towards Real-World Assets, which now represent 39.8% of all investments with a $2.04B balance. RWAs have been of interest to MakerDAO since 2020, but investments in them have ramped up slowly due to legal challenges and low TradFi interest rates.

MakerDAO experienced a big trend in the shift of stablecoin holdings to Real-World Assets (mainly T-bills) through projects called Clydesdale and Andromeda. As of August 24, 2023, Maker’s expected annualized revenues is $158.5M, of which $90M is from real-world assets.

The influx of revenues made it possible to enable the Smart Burn Engine in mid-July, which uses Maker’s surplus buffer to purchase MKR from a Uniswap pool, thereby removing MKR from circulation. This update made MKR deflationary. MKR’s outstanding supply decreased from 912k MKR in mid-July to 906k today.

💦🔬 Tx-Level Alpha: This transaction shows a return of T-Bills profits from project Clydesdale to the MakerDAO Surplus Buffer (it happens every two weeks). The same address receives profits from the T-Bills ETF every quarter (and soon a $6 million transfer). This structure, in which profits are sent to a smart contract, is called RwaJar. It replaces the Stability Fees for RWA vaults. This explains why MakerDAO revenues are sometimes understated.

③ PancakeSwap 🥞

👥 Chef Seaweed | Website | Dashboard

📈 PancakeSwap V3 crosses $15B+ in volume since launch

PancakeSwap is a leading decentralized exchange on BNB Chain and has been in its expansion to multiple chains over the last few months. PancakeSwap’s overall cumulative volume is ~$600B (second behind Uniswap across all DEXes). To date, PancakeSwap has deployed its v3 version to 6 different chains, and has generated a total of $15.4B in trading volume, with the majority of the volume being attributed to the BNB Chain, accounting for 91.7%, followed by Ethereum at 7.3%.

Zooming in on differences between v2 and v3: As of the end of March, v2 had 88% and 91% share in PancakeSwap's total volume on Ethereum and BNB Chain, respectively. The dominance of v2 has shifted with the introduction of v3, as v3 now takes up to 99% of the volume on Ethereum and 46% on BNB Chain.

Looking at different products, we see that before the end of May, Swap had accounted for 88% of the total Daily Active Users (DAUs) on the platform with 150k+ daily users. Since Pancake Protectors launched, the game has become the second largest DAU contributor with around 25K+ daily users, accounting for about 15% of the total DAUs of PancakeSwap in recent weeks with Swap's DAU share falling to 70%.

💦🔬 Tx-Level Alpha: PancakeSwap recently introduced the Revenue Sharing Pool, allowing fixed-term CAKE (PancakeSwap’s token) stakers to share part of the protocol’s trading revenues weekly. On August 21, 2023, around 19.5K CAKE tokens were allocated to the Revenue Sharing Pool as the third batch of revenue sharing distribution.

④ Aave 👻

👥 Jack | Website | Dashboard

📈 Aave GHO stablecoin crosses $30M in supply

Since July 16th, the GHO stablecoin's—which is pegged to the US dollar—supply has exhibited considerable growth. Starting from under 2 million, it has climbed to over 23 million. In tandem, there has been a Minting of 44 million GHO tokens and a burning of 20 million tokens, activities that any user can undertake. Yet, to contextualize these figures: this 23 million supply is just a small fraction compared to Aave's Total Value Locked (TVL) of $4.62B. This juxtaposition underscores the potential room for growth and the broader landscape in which GHO operates.

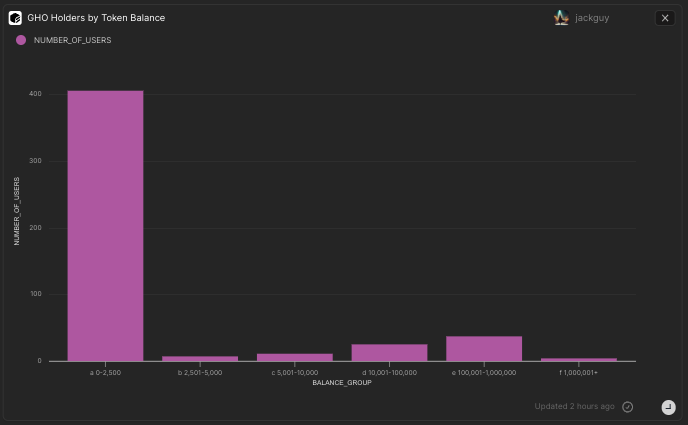

Among 493 GHO token holders, 414 possess less than 2.5k tokens, while 41 command over 100k. The average holder's stake is 48.6k GHO, but the median sits at 45.1 GHO. This breakdown reveals a diverse distribution pattern in the GHO small community of holders.

Since mid-July, GHO token's swap activity has seen a notable rise, escalating from mere hundreds of thousands daily to a current 1-3 million. Interestingly, daily swappers range between 20 and 60, indicating that a limited group handles this substantial volume, highlighting concentrated trading activity.

💦🔬 Tx-Level Alpha: In this transaction, the stablecoin GHO is minted within Aave when borrowed against collateral. With the minting, the borrower receives a debt token. To settle this, the GHO is returned to Aave, allowing collateral retrieval. However, if the collateral's value significantly drops compared to the borrowed amount, it risks liquidation. This system upholds GHO’s peg, as collateral in Aave consistently backs the GHO supply.

Quick Links: Disclosures