Our Network: Issue #9 (Part 2)

Network Updates (cont.)

📌 MakerDAO

Contributor: Primož Kordež, Founder of BlockAnalitica

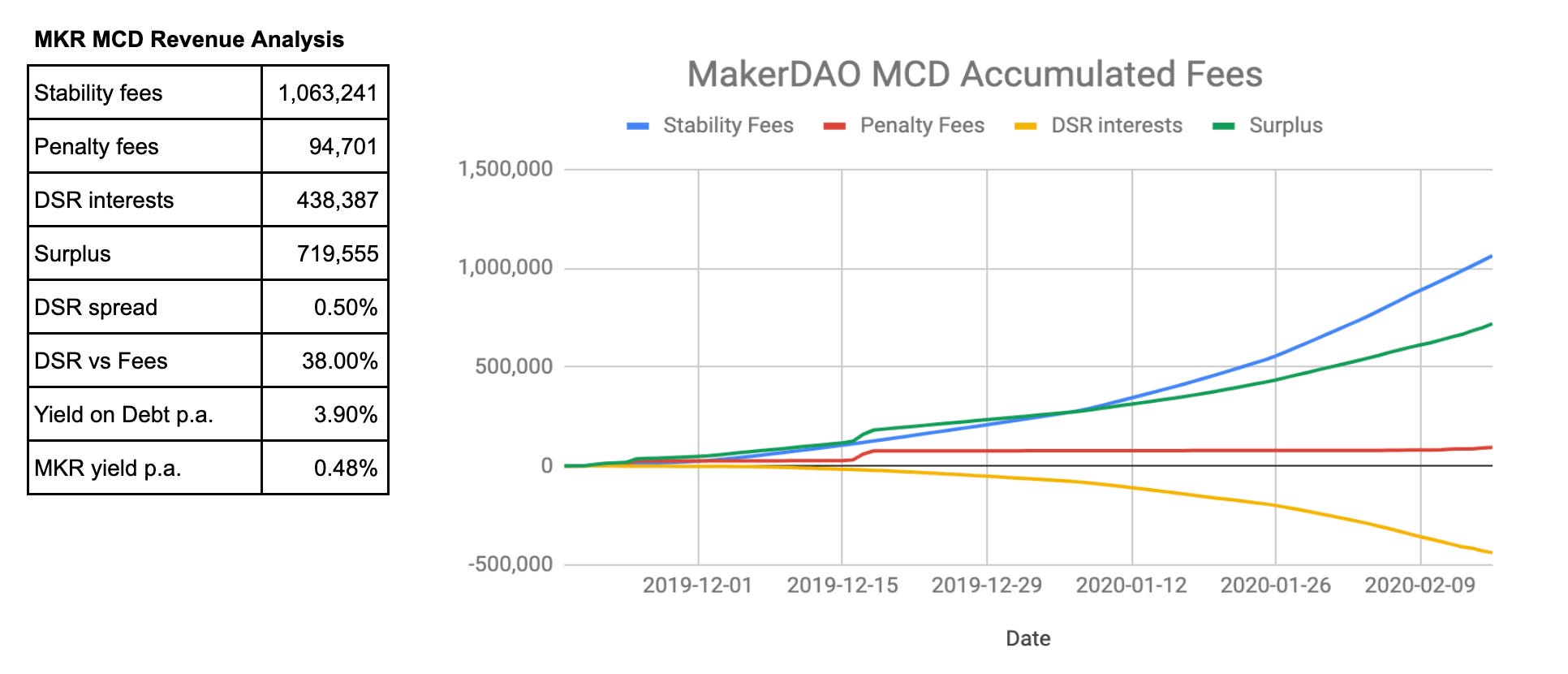

Since MCD launched 3 months ago, MakerDAO has generated 719k DAI in net fees (calculated by the sum of stability fees and penalty fees minus DSR costs). This translates into a 3.9% annual net margin on average debt issued, which is well above the 0.5% average DSR spread that MakerDAO had in that same period. This higher margin is explained by both lower DSR utilization and extra income from 95k in DAI penalty fees. This is also why the DSR costs comprise only ~40% of all fees even though the DSR spread was very low on average. (Note: that the actual net fee margin is always higher than DSR spread if the DSR has sub-100% utilization.)

The annual estimated yield on MKR is roughly 0.5%, which is below that same figure from 2019. This can be explained by the low DSR spread and also low rates in general from the launch of MCD in order to incentivize CDP migration. However, this yield does not include any additional SCD related fees in that same period and why the actual yield on MKR could be at least twice as higher, assuming collection of additionally generated fees by SCD.

DAI in DSR reached 72M and pushed DSR utilization to an all-time high of 57%. Even though there is a positive correlation between higher DSR rate and DSR utilization, it remains unclear what the true rate sensitivity is for savers, especially considering how there was recently a decrease in the DSR rate but also a record increase in DAI locked in the DSR. In a frictionless and rational market, all of the DAI should be locked in DSR. Therefore, the ideal metric to measure DAI demand and associated upward price pressure in response to rates is to measure how much external capital flows into DAI that gets locked into DSR afterward. There are more than 50 new addresses locking DAI in DSR daily, where the largest share of DSR deposits is represented by Compound and Chai which together hold 18% of DAI in DSR.

Currently there are over 3.3k vaults in MCD with approximately 50 new vaults created daily. Out of the new ones created, ~20% are being created by SCD CDPs who are migrating to MCD. The recent spike in vault creation and DAI issuance is of course associated with ETH price increase, although most of the DAI was issued by existing larger vaults. The debt distribution is similar to SCD still in that it is highly concentrated: the top 10 vaults together owe about 50m DAI, or 40% of total DAI debt.

The collateralization ratio distribution is a good metric to measure the behaviour of Vaults. Normally when collateral price increases as did recently, the collateralization ratio of Vaults improves and share of higher collateralized Vaults increases. For instance, the share of Vaults who have a collateralization ratio higher than 400% is currently 53% (measured by their debt position size as of 18th February). However, there is a mean-reverting process usually followed that decreases these ratios when highly-collateralized Vaults either withdraw unnecessary collateral or issue additional debt in case they are bullish on collateral. We have seen a similar pattern emerge at last year's bull run when the average collateralization ratio increased for 83% (from 300% to 550%) even though ETH price increased for more than 160% in that same period.

ETH locked in DeFi decreased by 12% this month, from 3.2m ETH to 2.8m ETH. This 400k ETH decrease was mostly led by MakerDAO MCD collateral withdrawals of about 450k ETH in that same period. This week alone in just 24 hours, about 100k ETH was migrated and refinanced from Maker to Compound, another 150k ETH was removed from highly collateralized large Vaults, and 25k ETH was removed from Uniswap after a large withdrawal of MKR liquidity. The borrowers were most probably either (1) removing unnecessary dollar valued collateral after ETH price increase or (2) diversifying their collateral and leveraged debt position across other protocols in light of recent flash loan attacks or (3) removing collateral and liquidity due to potential governance attacks associated with flash loans (also explains drop of Uniswap MKR & ETH liquidity).

The leverage behavior of Vault users typically reveals collateral price sentiment. Similar to measuring net long/short position on centralized exchanges of a particular asset and predicting price patterns, DeFi can also offer a view on leverage behavior activity of users, but with a direct view on a per user basis. This may serve better to estimate crowd behavior than simply looking at nominal amounts of leverage activity. DeFi Saver offers users an easy way to increase or decrease leverage in MCD. There are around 300 unique Vaults subscribed to this kind of automation service. The below graph reveals an interesting observation where boost (increase leverage) activity overpassed repayment activity for the first time in January right when the ETH bull run started. Note however that sample size might be currently too low to make any assumptions about general retail behavior when it comes to ETH price sentiment, especially by knowing most of these users represent only a small subset of ETH investors using DeFi.

📌 Synthetix

Contributor: Jordan Momtazi, VP Partnerships at Synthetix

sETH has the largest Mcap of any Synth (synthetic asset) inside the Synthetix network and has demonstrated how effective a well designed incentive can be to drive desired behaviour. The incentive directs 5% of the weekly inflationary supply to those who add liquidity to the Uniswap sETH/ETH pool. A further arbitrage mechanism to help hold a strong peg was used and has now been superseded with a SNX auction mechanism

This Uniswap chart shows the steady increase of sETH supply over the past 5 months. The pool is now 26% of Uniswaps total liquidity and at one stage was closer to 50%.

The Uniswap pool was incentivized to enable a way for traders to enter and exit synthetix.exchange without the fear of slippage and provide confidence in terms of liquidity. The below chart shows the increasing volume for the sETH/ETH pool, along side the increasing size of the pool since September 2019.

The weight of sETH (currently 65%) as a distribution across all Synths is artificially high as a result of the incentive and is now seen as likely too heavy relative to the overall open interest across the network. The project will introduce a similar sUSD incentive to balance out the open interest and create a more natural distribution of Synths. This is important for the network to scale sustainably and support assets the market wants exposure too. For more info on the Synthetix protocol and the various mechanism designs please visit the blog

📌 Aave

Contributor: Pablo Candela, User Success at Aave

As Aave-watch shows, the borrowing actions differ for each asset. Right now, the borrower preference is for stable coins DAI, USDC, USDT, sUSD, and TUSD. Apart from these assets, SNX is the only exception with a high borrowing percentage. This can be explained by the SNX staking reward incentivizing borrowers to borrow SNX from the platform. Most other assets have lower borrow demand, suggesting that they are deposited in order to earn interest or for use as collateral.

Flash Loans Activity. It is interesting to note that the last 15 Flash Loans on Aave were for DAI. Also, while the sample size is still quite small, the primary use-case of Flash Loans is arbitrage. There are two reasons for this: (1) Dexes arbitrage usually occurs more frequently than liquidations (2) Collateral swap is relatively new and is still experimental

Below are the earnings on Flash Loans for depositors (x-axis), the protocol (blue), and the Flash Loan executor (orange). It is interesting that in most of these cases, the depositors and the protocol earned more than the actual Flash Loan executor. It is also worth noting that after a recent governance vote, the Flash Loan fee on Aave has been reduced from 0.35% to 0.09%.

The current market size of Aave (total value locked + total borrowed) is $20M and has been growing steadily since its release on January 8th with an average growth rate of $0.5M per day. On the Aave futuristic realtime dashboard, users can view a variety of metrics including this one.

Finally, below is an image that shows the fees collected on each asset available in Aave Protocol. Approximately 80% of all collected fees are used for burning the LEND token.

Oped Related Readings & Sources

https://bostonreview.net/philosophy-religion/agnes-callard-angry-forever

https://www.erikhollnagel.com/A%20Tale%20of%20Two%20Safeties.pdf

https://www.esrad.org.uk/resources/vsmg_3/screen.php?page=1qguide

https://www.eugenewei.com/blog/2018/5/21/invisible-asymptotes

https://fs.blog/2013/02/the-psychology-of-human-misjudgement/

https://gauntlet.network/reports/CompoundMarketRiskAssessment.pdf

https://github.com/snakescott/awesome-tech-postmortems/blob/master/README.md

https://www.kitchensoap.com/2011/04/07/resilience-engineering-part-i/

https://www.kitchensoap.com/2013/10/29/counterfactuals-knight-capital/

https://link.springer.com/chapter/10.1007/978-3-319-70278-0_35

https://www.newyorkfed.org/newsevents/speeches/2018/ros180517

https://vessenes.com/ethereum-contracts-are-going-to-be-candy-for-hackers/

http://web.mit.edu/2.75/resources/random/How%20Complex%20Systems%20Fail.pdf

Our Network is a weekly newsletter where top blockchain projects and their communities share data-driven insights. Subscribe now to receive a crash course in on-chain metrics and crypto fundamentals, and never miss an issue.

About the editor: Spencer Noon leads investments for DTC Capital, a fundamentals-focused crypto fund. He actively tweets about on-chain metrics.