Our Network: Issue #72

Coverage on YFI, MKR, NXM, and LQTY.

Issue #72 of the on-chain analytics newsletter that reaches 11k crypto investors every week 📈

About the editor: Spencer Noon is an investor at Variant, a first-check crypto VC fund.

This week our contributor analysts cover DeFi: Yearn, MakerDAO, Nexus Mutual, and Liquity.

① Yearn

👥 Michael Silberling

📈 WOOFY brings 2.7k new holders to Yearn

👉 Follow the Yearn Community on Twitter

On May 11, Yearn introduced the WOOFY token which tested two ideas:

Unit Price Psychology: Yearn’s YFI token was one of the higher-priced per unit assets (~$75k for 1 YFI on May 11), but YFI holders could exchange YFI for WOOFY at a 1:1M rate (i.e. if 1 YFI is $75k, then 1 WOOFY is $0.75)

Dog Meme Coins: would there be additional sentiment-driven buying due to the simple fact that its a dog meme like Doge.

Metrics can be found below:

WOOFY holders already make up 9% (3.2k) of all addresses with Yearn exposure (YFI or WOOFY) even though WOOFY only stores 0.7% of Yearn’s market cap. 84% (2.7k) of WOOFY holders have never held YFI (in it for memes?).

Can WOOFY influence YFI? — Leading up to YFI’s all-time high, WOOFY ranged between 10-40% of total Yearn trading, peaking at $7.4M hourly volume; However, aside from launch and market volatility, YFI and WOOFY’s derived price (WOOFY price * 1M) has so far held within +/- 5% of YFI’s unit price.

② MakerDAO

👥 Vishesh Choudhry

📈 Liquidations 2.0 tops $5M Revenue at Launch

👉 Join MakerDAO’s community on Rocket Chat

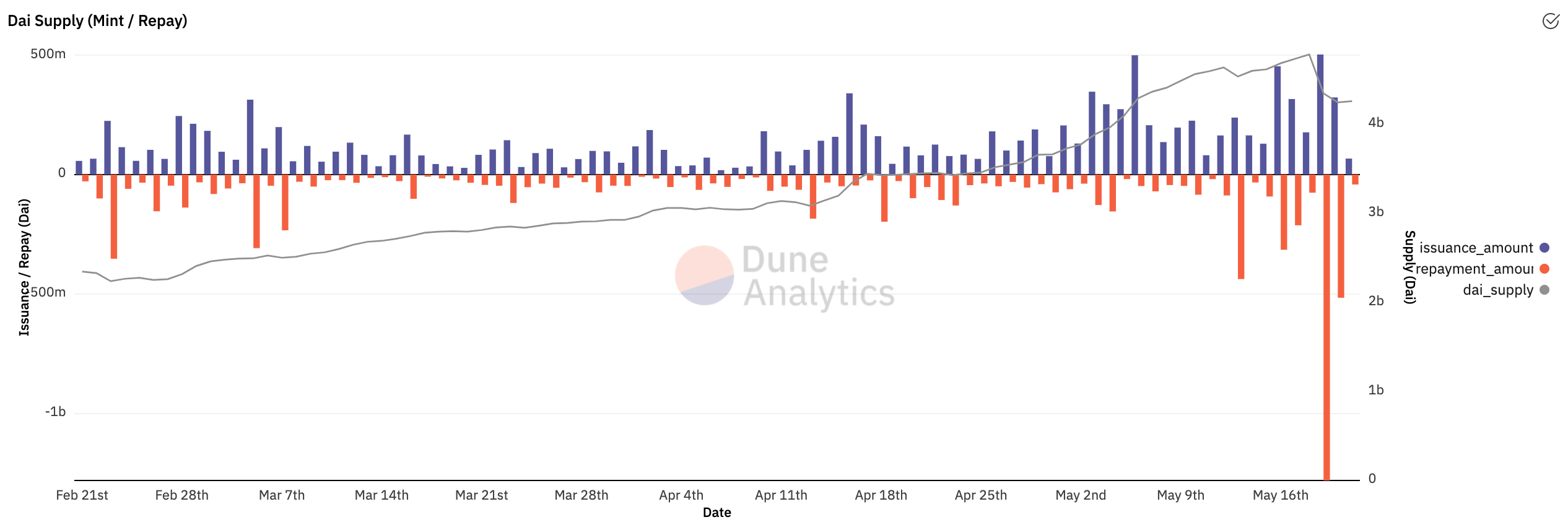

DAI supply has been growing consistently in 2021 (almost 400% YTD). Supply brushed up against $5b this week, just before the ETH price crash that sent numerous DeFi protocols into liquidations. Maker was one of these protocols, with over $46M liquidated on May 19th. However, the DAI supply dipped by a full 400-450M; As such, a large portion of positions were rebalanced or repaid prior to liquidation. This is in contrast to the sudden and severe “zero-bid” liquidations of Black Thursday 2020.

On May 17th, the Maker community upgraded to “Liquidations 2.0”. This is currently live for nearly all vault types. Of the $46M liquidated (including penalties) on May 19th, almost 50% came from ETH vaults and 30% from WBTC. This generated over $5M in revenues for the protocol and executed fairly efficiently.

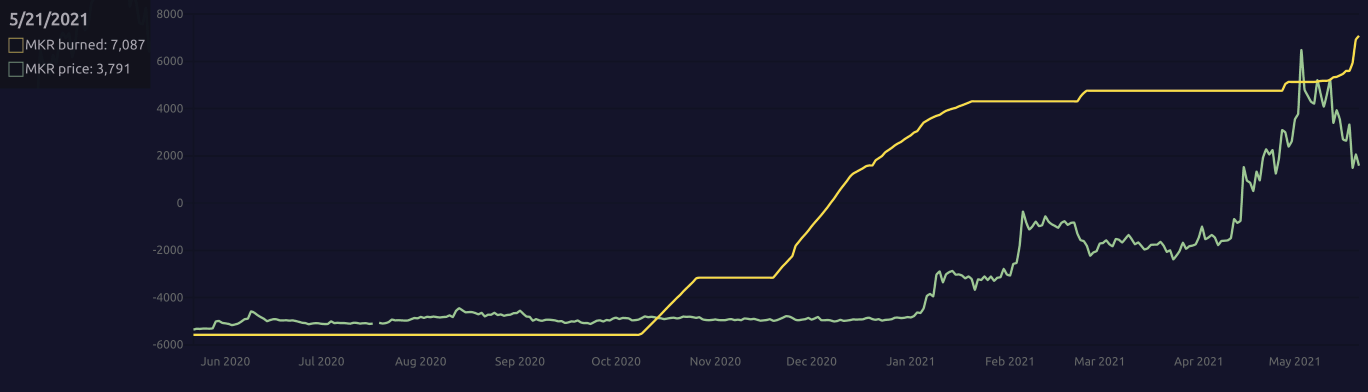

The May 19th liquidations led to an uptick in DAI surplus, which then led to MKR-burning auctions. Protocol changes in 2021 have led to increased revenues along with MKR being burned — to date, ~7100 MKR has been burned. MKR price has grown alongside the increase in revenues (liquidations are a major source).

③ Nexus Mutual

👥 Richard Chen

📈 Nexus reaches ATH of $1.2B in active covers

👉 Submit grant proposals for the Nexus community fund

Several record cover purchases were made in the last few weeks, including a $65M cover on Compound which is the largest cover to date that wasn't purchased for farming. Curve also became the first project to reach over $100M in active covers, just over two years after Bitgo secured $100M of insurance from Lloyd's.

Nexus recently launched protocol cover, which means you can now get coverage on other L1 and L2s like BSC and Terra. Coverage was also expanded to include attacks like oracle manipulation, governance attacks, and economic incentive failures.

May 2021 is on pace to generate the most monthly revenue ever for Nexus from cover premiums alone. Sep 2020 and Jan 2021 had spikes due to Cover Protocol and Armor.Fi farming, so May's revenue will be all organic. Annualized revenue run rate also reached an all-time high $32M.

④ Liquity

👥 Kolten

📈 Liquity sees large growth and navigates ETH crash

👉 Join the Liquity community

Liquity is an immutable, governance-free borrowing protocol that allows you to draw 0% interest loans against ETH. Loans are paid out in LUSD, a USD pegged stablecoin, and need to maintain a minimum collateral ratio of only 110% (under normal conditions). Since launching April 5 Liquity grew to hold ~1.17M ETH at its peak and now stands at ~850k ETH even after the ETH crash on 5/19. LUSD also swelled to a supply of ~1.3B at its peak before the crash’s leverage wash out brought it back to ~580M.

As mentioned, Liquity does not charge interest on loans, but instead charges a one-time borrow fee up front ranging from 0.5% to 5% (most often ~0.5%). The borrow fees combined with redemption fees are distributed directly to LQTY stakers and have generated >$10.3M in protocol revenue since launch.

Liquity handled the 5/19 crash flawlessly — 310 positions were liquidated, along with 93.5M LUSD debt being offset against the Stability Pool (SP) and ~48.6k of liquidated ETH being distributed to SP depositors. With the ETH price recovering, this means SP depositors are in the green and were able to “buy the dip”.