This is issue #66 of the on-chain analytics newsletter that reaches nearly 10k crypto investors every week 📈

About the editor: Spencer Noon is an investor at Variant, a first-check crypto VC fund.

✨ Together with our partners:

1inch, whose v2 offers the best rates by discovering the most efficient swapping routes across all DEXes—swap on the customizable new 1inch UI. And also Aave, where you can experience DeFi: Deposit, Earn, & Borrow on Aave.

This week our contributor analysts cover DeFi: PoolTogether, Nexus Mutual, UMA, and Sushiswap.

① PoolTogether

👥 Leighton Cusack

📈 $1.1 million of prizes in 5 weeks

👉 Jump into the next pool

PoolTogether is a protocol for no loss prize savings. Users deposit money to have a chance to win prizes and can withdraw their money at any time. Prizes are comprised of the interest accrued on all deposits, of which all depositors automatically receive the POOL governance token. A key metric for the protocol is total prizes awarded — with $1.2 million in prizes that have already been distributed. Recently the pace of growth has accelerated with $273,000 awarded in the last week alone.

Since prizes are derived from interest earned on deposited funds, total assets deposited represents an important metric. The protocol currently has $155 million in total deposits. The largest prize pool is USDC with $63 million deposited followed by Dai with $52 million deposited.

A portion of every prize is redeposited back into the prize pool generating a higher effective APR and larger future prizes. This was first activated by governance 3 weeks ago and amounts to an effective ~2.5% of the prize value — resulting in $30,000 of reserves being collected so far.

② Nexus Mutual

👥 Richard Chen

📈 Active cover amount is $635M, up 9.27x YTD

👉 Join the newly created Nexus Community Fund

Protocol cover launches on April 26, which means Nexus will expand its coverage beyond smart contract bugs to oracle failures as well as economic and governance attacks. Nexus also covers centralized exchanges and custodian hacks, with millions of dollars of coverage on Binance, BlockFi, Celsius, and others. In addition, when DeFi projects launch on layer 2 and other chains, the new Nexus cover policy will apply automatically.

Annualized premiums are $18.2M, with additional revenue coming from Nexus’s sell spread and investment earnings. Even with the Yearn claim payouts in Feb, Nexus has been massively profitable unlike many traditional insurance companies that lose money on their core business (premiums - claims & expenses).

NXM currently trades at around 1.6x book value (and even lower for wNXM). Book value is the ratio between the market cap and capital pool size. By comparison, mature traditional insurance companies trade at 3-4x book value yet have much lower growth potential.

③ UMA

👥 Vishesh Choudhry

📈 UMA has reached $174M TVL (+335% YTD)

👉 Join the UMA community

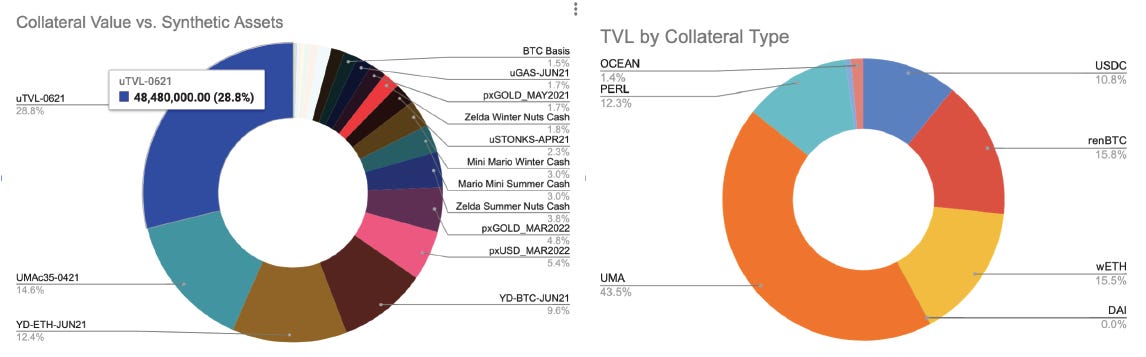

In Feb, UMA announced its KPI options, which is a product offering that grows in value with TVL in the protocol. Since rewards for this KPI option are locked in the protocol it also counts towards TVL. In Dec 2020, TVL was ~$40M, which has since grown to ~$174M. This is primarily held in $UMA, $WETH, $renBTC, $PERL, and $USDC collateral. The main synthetics built on this value are UMA options (uTVL-0621 and UMAc35-0421), YD-ETH and YD-BTC, and a few smaller offerings. This is a ~335% increase YTD.

UMA provides tools for devs to create their own synthetics contracts. In Nov 2020, they launched a program to incentivize devs to build on top of UMA. To date, 85 products have been created using UMA, many of which are still active or hold value. This growth started to uptick in March 2021.

UMA also offers a price oracle system upon which these synthetics contracts are built, generally used at redemption/expiry of options. Voters vote on prices to update these oracles. The protocol has seen 103 such oracle requests to date. Over time 92 different voters have contributed to these price oracles.

④ Sushiswap

🥇 Pierre-Yves Gendron, Adam Cader

📈 SushiSwap is Ethereum’s second-largest DEX

👉 Join the Sushiswap community

Sushiswap is currently ranked as the second-largest DEX, processing weekly volumes of ~$2B from ~10k traders, second only to Uniswap which processes ~$7.5B in volume from 175k traders — This implies that traders on Sushiswap execute, on average, larger trades ($200k weekly) than those on Uniswap ($43k weekly).

Sushiswap's weekly protocol fees (0.05% or 1/6th of LP fees) are currently ~$1M, implying an annualized yield of 2.2% (1.3% on a fully diluted basis) for token holders. Since January yields have diminished following a decrease in trade volume, while the price of SUSHI increased in part due to the Coinbase listing in March.

Sushiswap's liquidity (TVL) is $4.34B, which is slightly lower than Curve's ($4.54B) and Uniswap's ($5.68B) TVL. SushiSwap's liquidity is spread across hundreds of pairs, with 49% being in the WETH/WBTC pair, 22% in WETH/Stablecoins pairs (USDC, DAI, USDT) and 10% in the WETH/SUSHI pair.

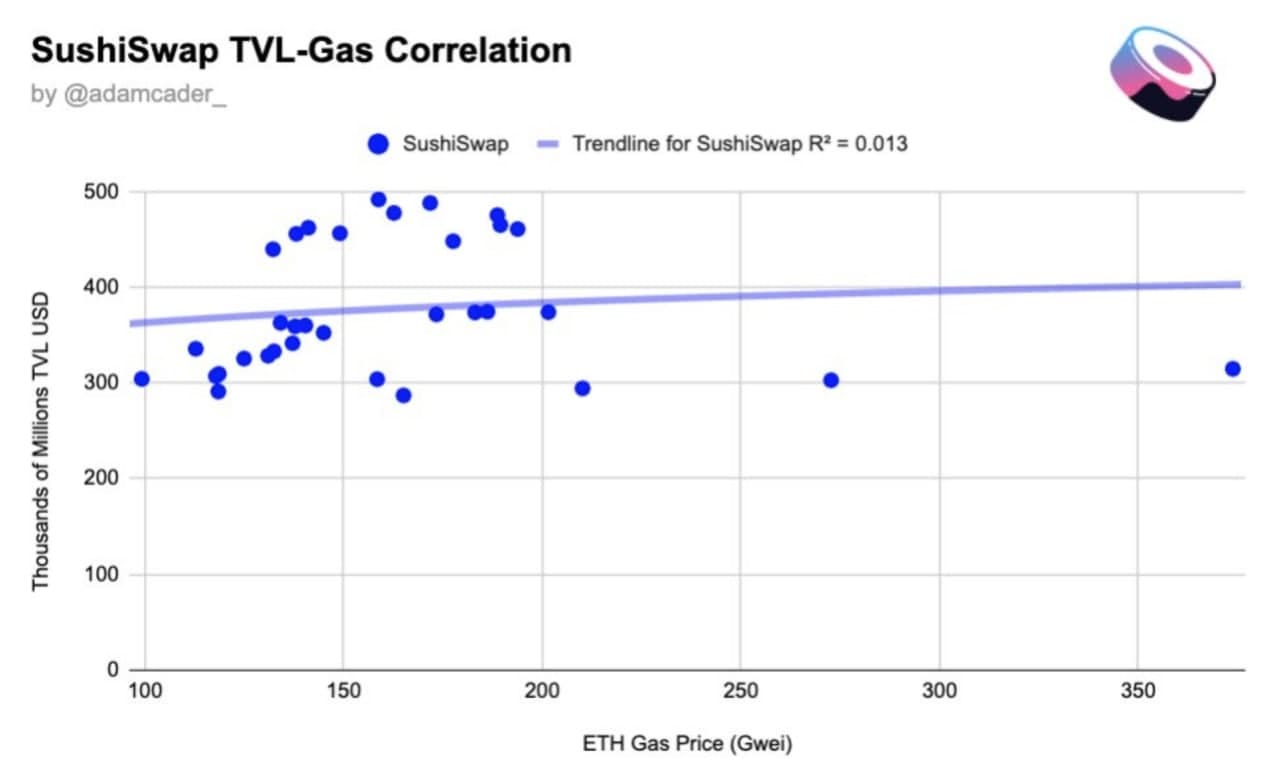

The correlation between Sushiswap’s TVL and the ETH gas network fees remains low at an R^2 value of only 0.013 — indicating there is essentially no correlation and that Sushiswap’s liquidity incentives are a strong protocol moat even when fees to enter pools are high.

Sushiswap added more than 1128 distinct new liquidity providers in just the first eight days of April. The amount of returning LP’s increased from 642 to 1951 from February to March: a 230% net change. Moreover, a stable level of returning LP’s can decrease future assumptions of pool volatility.