Our Network: Issue #6

Updates on Tezos, Ethereum, Decred, Zcash, and Bitcoin.

Welcome to Our Network, a weekly newsletter where top blockchain projects and their communities share data-driven insights about their networks.

This week our contributors cover Layer 1 cryptocurrencies:

Tezos

Ethereum

Decred

Zcash

Bitcoin

Network Updates

📌 Tezos

Contributor: Alexander Eichhorn, Founder at Blockwatch Data

Staking: Custodial staking continued to gain traction in Tezos. Throughout January 2020 staked balances at exchanges increased by +1.3% (26M) to 14% (89M) of all staked coins. Staking participation overall increased by +18M to a new ATH of 77.3% (635M). At the same time staking yield dropped to an all-time-low of 1.48% above inflation. At current prices you needed to stake 1.2M tez to make a base income for a decent living in Berlin.

Validators: Despite diminishing yield the number of consensus participants (bakers) remains relatively stable at around 430. We show unique roll owners here because Tezos assigns validation & voting rights based on rolls with one roll equal to 8000 tez. About 50% (207) of all validators are self-baking entities, meaning they have <= 1 incoming delegation. 160 of them own less than 100k tez in staking balance, 10 self-bakers are whales with balances between 1-5M tez.

Centralization: Although the amount of unique validators is high (430) the distribution of their weight tells a slightly different story. 50+% of Tezos staking is controlled by only 9 different entities while the top 100 bakers control 92% of the network. The largest entity (the Tezos Foundation) validates 27% of all blocks, the next largest are Coinbase (5.84%), Polychain (4.42%) and Cryptium Labs (3.62%), Binance (3.16%), Kraken (1.96%), P2P Validator (1.93%), Airfoil (1.72%) and FlippinTacos (1.71%). This is not troubling for consensus since rights are assigned randomly, but it plays a relevant role in governance. The foundation and some of the large bakers have historically abstained from voting. With the rise of custodial staking exchanges suddenly find themselves under pressure by the community to vote and build tools to let their delegators contribute.

Growth: Funded accounts on Tezos continued to grow by +7% (+24k) throughout January, but the number of economically relevant accounts with more than 100tz balance increased only by 938 to 24.6k, which represents 6.6% of all 376k funded accounts. Overall, the top 1k accounts hold about 67% of total supply which is close to Litecoin (64%) but much higher than Bitcoin (35%).

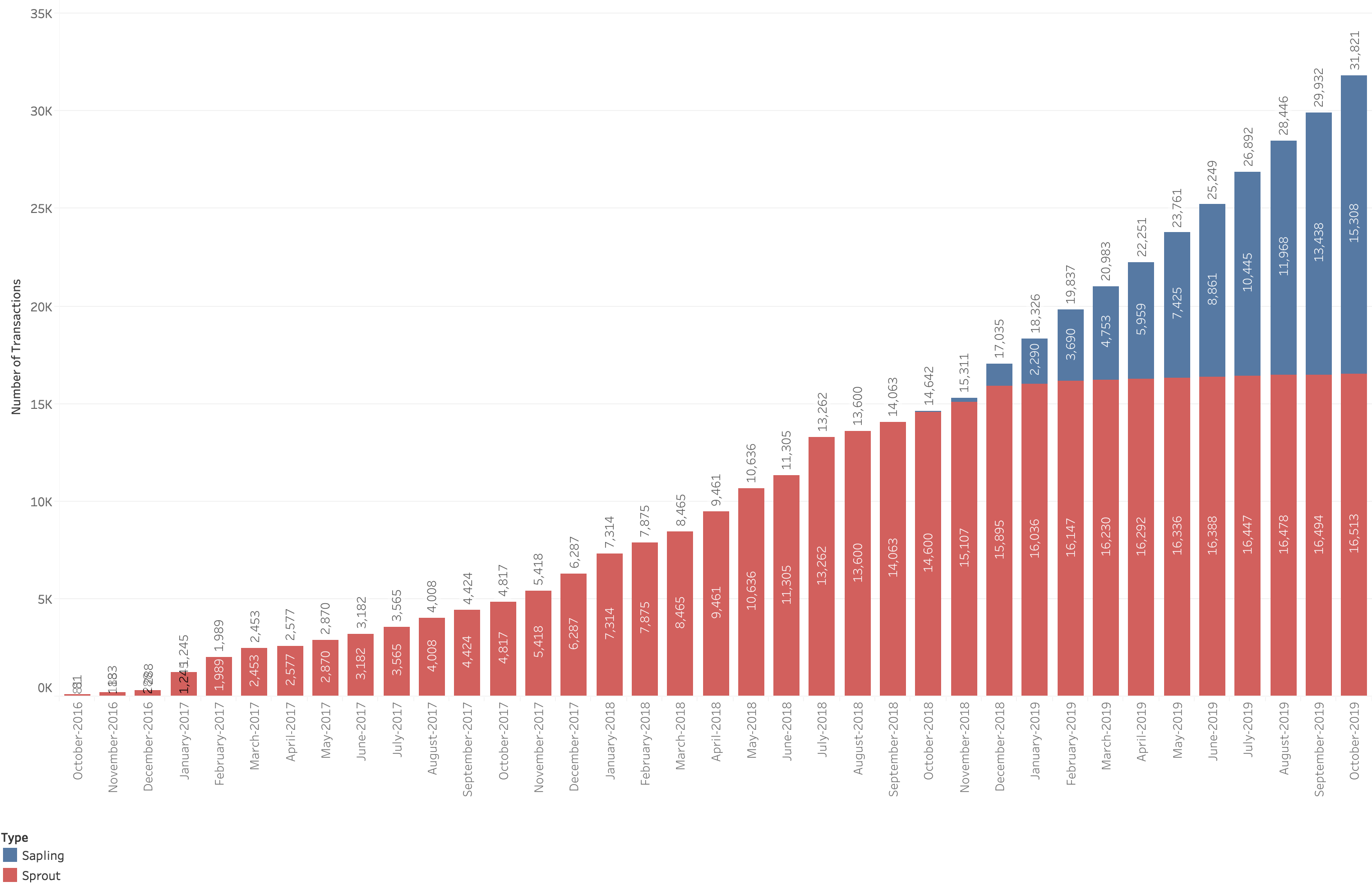

Adoption: Smart contract usage on Tezos mainnet has not picked up speed yet. Throughout January mainnet has seen a meager 55 new contracts and 3.5k contract calls, the most prominent deployed contract has been StakerDAO. The real action in Tezos still happens on various testnets hinting at a quickly growing developer base. The most active one is Babylonnet which has seen an all-time high in deployed contracts 4,647 (+1,456 from Jan 1st) and an unprecedented growth in smart contract calls (+62k since Jan 1st which is a 2.6x growth in one single month).

📌 Ethereum

Contributor: Maksim Balashevich, founder of Santiment

Miners' ETH holdings poised to breach all-time-high. Across the entire Ethereum miner ecosystem, the last three months were marked by stable and undisrupted accumulation. As a result, the cumulative balance of all ETH mining pools is currently hovering at an all-time-high of 1.69M ETH (which has a current value of ~$300M). These periods of accumulation tend to suggest high confidence levels in the project among the majority block creators, at the very least relative to the current market conditions. On the other hand, major miner sell-offs have often been followed by quick and significant price corrections historically. The last time the network’s miners held on to this much ETH was back in late October of 2019, when a drop below $170 prompted some to offload their holdings. Barring major market volatility this time around, we’re likely to breach this milestone within the next few days.

Ethereum’s coins continue to age “gracefully”. Mean coin age is a relatively new method of measurement to observe a network’s behavior in aggregate. For each coin, we calculate how long it has stayed in its current address and we compute the average of all those ages. Major drops in mean coin age indicate that previously dormant coins are starting to change addresses, and often correlate with increased market volatility. An undisrupted incline on the chart signals a growing average age of all coins on the network.

The current view of Ethereum’s Mean Age highlights a year-long period of relative token inactivity (barring a few minor bumps at short-term price increases). On aggregate, previously dormant coins aren’t moving or being interacted with, and the average age of ETH (network-wide) continues to grow. This is further reinforced by the declining share of Ethereum tokens that have moved within the last 365 days; On January 1st, 2019, 54.6% of all ETH in existence was active within the past year. At the end of January 2020, this number has dropped to 39.6% of the total ETH supply. Both data points highlight the same trend - ‘old’ coins remain relatively unutilized, and the share of active coins continues to decrease. With the explosive growth of ‘ETH locking’ mechanisms and DeFi solutions, this is likely to become the norm in years to come.

It will be interesting to see how this trend affects various valuation models that draw from network activity and health indicators. NVT, for example, posits that the more value transferred on the network (using on-chain trx volume as a proxy), the more valuable the network is itself. Given that several of Ethereum’s emerging use cases warrant relative coin inactivity, it could likely prompt the creation of new and/or modified approaches to ‘traditional’ blockchain network valuation.

From a network activity perspective, Ethereum has had a fairly slow start to the year to this point - at least compared to Januaries prior. Over the last 30 days, the network added 1,184,476 new addresses - a 9.5% decrease compared to Jan 2019 and an 82.4% decrease compared to Jan 2018. Of course, the latter is to be expected considering the market-wide conditions of early 2018. However, the same can’t really be said for Ethereum’s current decline in network growth relative to 2019. The two Januaries are much more comparable from a market standpoint: Ethereum was priced at $135 on January 1st, 2019; it was $131 on January 1st, 2020.

We’re also seeing the same downtrend in Ethereum’s active addresses this January. Over the last 30 days, 5,801,553 ETH addresses interacted with the network - a 14.1% reduction compared to Jan 2019. This is unlikely to be a cause for concern, however, as much as further validation of Ethereum’s cyclical growth. The network has followed the same growth pattern several times in the past already - a sluggish start to the year followed by major adoption cycles in Q2 and late Q4. For example, below is the plot of new addresses added to the Ethereum network in the last 12 months. Of course, much of the network rhythm continues to be dictated by the coin’s price action and general market conditions, but the growing sample size continues to make the case for Ethereum’s seasonal appeal to new and existing users.

Divergence in Ethereum’s Holder Demographics. Over the past three months, we’ve been seeing a notable discrepancy in the behavior of micro and retail ETH holders on the one side, and the proverbial whales on the other. Cumulatively, the first category has continued to accumulate ETH at a high clip and across demographics, coinciding with the rising popularity of retail DeFi solutions. Here’s a short breakdown:

Addresses holding <0.001 ETH: +24.7% (+1,055 ETH)

Addresses holding 0.001-0.01 ETH: +10.3% (+4,426 ETH)

Addresses holding 0.01 - 0.1 ETH: +6.1% (+10,000 ETH)

Addresses holding 0.1-1 ETH: +1.4% (+7,600 ETH)

The same can’t be said for large ETH addresses, however, which have been reducing their holdings (sometimes significantly) throughout the same time frame.

Addresses holding 1000-10000 ETH: -0.02% (-4000 ETH)

Addresses holding 10k-100k ETH: -1.24% (-33000 ETH)

Addresses holding 100k-1m ETH: -5.06% (-1.8M ETH)

The only major ETH demographic that has remained ‘in the green’ is also the largest one: addresses holding 1m-10m ETH, which are mostly made up of exchange wallets. In the past 90 days, these wallets have added 40.9% to their cumulative holdings, or a total of 3.1M ETH.

📌 Decred

Contributor: Checkmate, Decred contractor

Decred is approaching its fourth birthday on 8-Feb-2020 and to celebrate, this week will be covering an array of achievements by the Decred chain to date. Decred has finalized over $11.44 billion in USD denominated value over its lifetime, accounting for the movement of over 409 million DCR units. A dominant component of these on-chain flows comes from DCR tickets (~50%), which represent long-term holders participating in PoS security and governance.

ASIC hardware was first released for Decred in January 2018, approximately two years after launch and at the peak of the 2017-18 bull run. Decred hashrate has grown by 1,000x following ASICs coming online. Given the prolonged bear market, the Difficulty ribbon is currently squeezed although showing early signs of recovery. Interestingly, the acceleration in hash-rate growth and subsequent squeeze/plateau of the difficulty ribbon are reminiscent of Bitcoin throughout the the 2015 bear market.

Decred is unique in that it supports both Miners and Stakeholders with coins continually circulating via DCR Tickets. Observing the aggregate behavior of both parties shows each creates fundamental support/resistance levels during price discovery.

A cumulative $5.6 Billion has been locked in DCR tickets and this commitment line (green) has been a magnet for price in a Bull Market.

The cumulative reward paid to PoW miners (incl. fees) now totals $147 Million and supports the notion that miners support bottoms for Bear Markets.

The Realised Price acts as a dynamic support and resistance line in response to changing ticket flows in Bull/Bear conditions.

The Realised Price and PoW Income line are currently squeezed, much like in early 2017.

The Decred Treasury is a central component of Decred's value proposition, enabling sustainable and self-sovereign development into the future. The treasury receives 10% of the DCR block subsidy for deployment by DCR stakeholders. To date, the Decred Treasury has accumulated over 639,600 DCR, equivalent to $11.5 Million at $18/DCR. The project has a spend ratio of 32% of inflows to-date and 14% of the final inflow of 2.1 Million DCR, at the end of the block subsidy. Pricing all Treasury expenditure outflows on the day of the transaction, the Decred treasury has spent $6.96 Million USD to bring the protocol from genesis to its current state.

Decred is currently undergoing its fifth on-chain vote to upgrade the consensus rules. The DCP0005 change restructures block headers and filters to improve SPV security and optimize the interaction between PoS votes and PoW miners. The DCP0005 codebase lies dormant in the new node software and now that 95% of Miners and 75% of Stakers have upgraded, the vote to activate it is live. A minimum quorum of 20% of Stakeholders must vote with 75% consensus to activate the new code. The current approval rate has 99.94% of tickets voting Yes, out of a 59.68% participation rate (note that abstain is default and only yes/no votes count as participation).

📌 Zcash

Contributor: Elena Giralt, Product Marketing at Electric Coin Company

The dev fund polling has completed and community sentiment is clear. In addition to Electric Coin Co and Zcash Foundation funding, there is now a new grant pool (40% of the dev fund) for other 3rd parties to receive funding for Zcash work.

While the number of shielded transactions is a small fraction of the total number of transactions on the Zcash blockchain, every single shielded transaction increases the anonymity set as a whole. Because of this, the anonymity set for Zcash is significantly larger than protocols that achieve privacy through obfuscating or mixing. This past month, 13.2% of Zcash transactions were shielded.

According to OnChainFX, Zcash is 25th by market cap but in Real Volume it ranks 12th, Adjusted Transaction Volume (9th) and Active Addresses (12th).

Developer activity and collaboration are increasing. ECC recently developed an internal dogfood wallet and mobile wallet SDKs. Zcash Foundation issued grants to support community developers working on core protocol as well as wallet applications. According to Flipside Crypto, Zcash developer behavior has increased by 2.75% in the last 10 days.

Since 2016, Zcash has maintained a regular and predictable release and network upgrade schedule. Going forward, Zcashd will have new releases approximately every six weeks and there will be roughly two network upgrades per year.

📌 Bitcoin

Contributor: Nate Maddrey, Research Analyst at Coin Metrics

Bitcoin estimated hash rate has surged to all-time highs over the start of 2020. The following chart shows the estimated hash rate smoothed using a seven-day rolling average. Estimated hash rate topped 120M TH/s on January 25th, up from about 113M on January 1st.

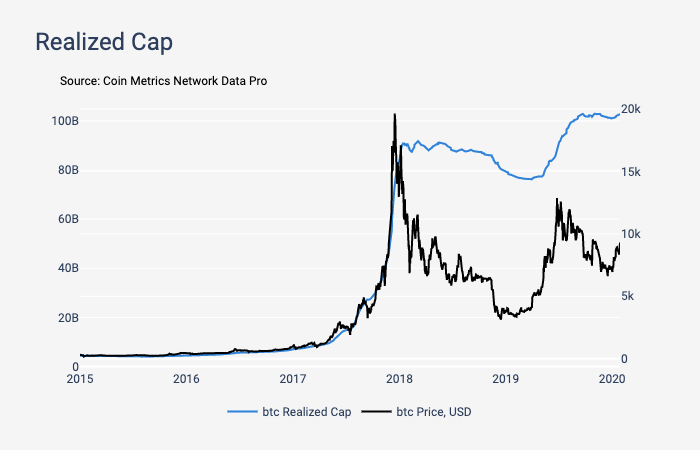

Bitcoin realized cap is also approaching all-time highs. Realized cap values each coin at the time it last moved (i.e., transferred between two distinct addresses) on-chain. So if a coin last moved in 2017 when the price of the asset was $2,500, that particular coin would be priced at $2,500 instead of the current market price. The sum of the prices of all coins priced this way gives the realized cap. Realized cap can be thought of as an estimate of the average cost basis of all holders of an asset. Bitcoin realized cap peaked at a little over $103B on November 4th, 2019. As of January 9th, Bitcoin realized cap is $102,945,486,900.

Bitcoin supply appears to be getting increasingly distributed. The below chart shows the total supply held in addresses with balances greater than 1 in X of the total Bitcoin supply (where X ranges from 1K to 10B). For example, the blue line shows the aggregate supply held by addresses that each individually hold at least 1/1000th of the total Bitcoin supply (1/1000th Bitcoin supply is about 18,188 BTC at time of writing). The total supply held by addresses with balances of at least 1 in 1K has decreased since mid-2019, while the total supply held by addresses with smaller balances has been steadily increasing. This signals that supply is moving from addresses with larger balances to addresses with smaller balances.

The amount of daily active addresses receiving Bitcoin (i.e. addresses that are sent a transaction) is almost even with the number of daily active addresses sending Bitcoin (i.e. addresses that send transactions). This is a relatively healthy signal, since a higher proportion of receiving to sending active addresses can be a sign of chain spam.

Our Network is a weekly newsletter where top blockchain projects and their communities share data-driven insights. Subscribe now to receive a crash course in on-chain metrics and crypto fundamentals, and never miss an issue.

About the editor: Spencer Noon leads investments for DTC Capital, a fundamentals-focused crypto fund. He actively tweets about on-chain metrics.