Our Network: Issue #5

Updates on MakerDAO, Synthetix, Set Protocol, and Uniswap.

Welcome to Issue #5 of Our Network, a weekly newsletter where top blockchain projects and their communities share data-driven insights about their networks.

Network Updates

This week our contributors cover DeFi:

📌 MakerDAO

Contributor: Primož Kordež, MakerDAO Interim Risk Team and founder of BlockAnalitica

The introduction of the DSR in Multicollateral DAI has produced a more competitive landscape for secondary lending platforms. MakerDAO overtook the #1 spot for DAI lending market from Compound, also because Compound implemented DSR for its unutilized supply. dYdX marketshare also significantly decreased as its value of DAI deposits dropped by about 80%. The total value of DAI deposits across major lending platforms represents about half of the current DAI and SAI total supply, which is interestingly less than the ATH of 66% reached during September of last year. This may be due to the less active remaining SAI lending markets and the higher interest rates seen last year (savers could earn 13% yield during summer last year versus 6% currently).

Marketshare of DAI borrowing has also dropped significantly for secondary lending platforms. The total value of DAI and SAI outstanding loans on secondary platforms is currently 22m, or only 15% of MakerDAO’s borrowing or total supply. This ratio was much higher in the past. For example, last year in September, 36m SAI or 46% of total supply was borrowed on secondary lending platforms. The recently increased marketshare of MakerDAO borrowing is probably related to lower borrowing rates on MakerDAO that were voted on for migration purposes.

MakerDAO governance is currently in the midst of a discussion about the Emergency Shutdown of Single Collateral DAI. We have witnessed a bit of a drop in the pace of CDP migration, which is supported by increased SAI inventory in the migration contract. Analyzing a sample of the top 100 remaining SCD CDPs reveals that almost half of SAI sampled debt is represented by CDPs which were totally inactive during the migration period. Only about 20% of sampled debt is held by CDPs which are showing signs of unwinding their debt position. Further, 4m SAI debt is represented by CDPs which were still active in SAI minting during migration. These users may prefer using SCD instead of MCD for some reason or perhaps they are speculating on other potential benefits of holding SAI as it experiences a liquidity shortage.

Speaking of a SAI liquidity shortage, there has been a huge drop in SAI trading activity across DEX venues. Currently only Uniswap and Kyber offer decent liquidity for SAI, having daily trading volumes averaging $250k in the last week. Uniswap SAI liquidity is at $1.2m, whereas DAI liquidity is at $2.9m. This has become a serious problem for the remaining SCD CDPs who want to deleverage, particularly for those trying to increase their collateralization ratios in order to protect themselves from getting liquidated in the event of the price of ETH collapsing.

DAI locked in the DSR has been steadily increasing since the beginning of the migration period. The most notable increases were in the third week of December when Compound implemented the DSR for its unutilized DAI and during the second week of December when the DSR rate increased from 2% to 4%. The recent rate increase of the DSR from 4% to 6% continued the linear pace of DAI being locked in DSR until last week when DSR utilization fell to previous levels seen before the rate increase. This happened due to one large withdrawal of DAI from the DSR and can be also partially explained by an increase in DAI minting in 2020 that has outpaced the amount of DAI locked in the DSR.

📌 Synthetix

Contributor: Jordan Momtazi, VP Partnerships at Synthetix

81.6% of SNX (the native token of Synthetix) is currently staked, which is one of the highest staking ratios in crypto. Because of this, the network supports over $19m of synthetic assets (called Synths). Synths range from synthetic commodities to currencies to cryptoassets.

The target collateralization (c-ratio) across the network is 750%, which is quite high relative to other systems in DeFi. The ratio has been deliberately set at this level as a way to buffer from any shocks that may occur early in the life of the protocol. The target number itself (750%) may go up or down based on how the network responds to various scenarios and/or community feedback in the future. Longer-term, we envisage this ratio will come down and enable a more capital-efficient system.

The active c-ratio is determined by looking at all of the wallets that are staking and calculating their total SNX value against the value of Synths issued. This number (currently 786%) is dynamic and fluctuates based on the price of SNX and the debt (total Synth) value within the network. Below is a look at the c-ratio since June of 2019. Note that the system increased the required c-ratio from 500% to 750% in June and the network responded as designed due to the incentives for Stakers to be over collateralized.

Finally, below are metrics from the top 35 SNX wallets. To maximize rewards, a staker would need to have 100% of their SNX value locked and be as large of a percentage of the debt pool as possible. This percentage is simply what portion of total Synths you have issued relative to the entire pool.

📌 Set Protocol

Contributor: Anthony Sassano, Product Marketing Manager at Set Protocol

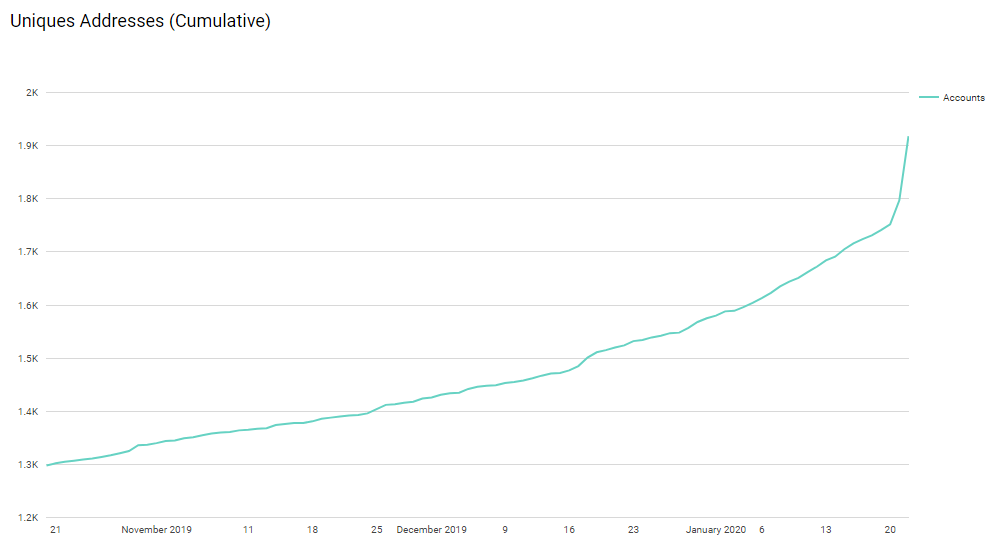

The total value locked (TVL) in Set Protocol has been growing steadily and is almost back at an all-time high. TVL fell in December because a couple of the larger Sets made some bad trades which resulted in under-performance. However, since then these same Sets have been outperforming the market against both ETH and USD. We've also seen a nice uptick in activity since we introduced Set Social Trading onto the platform.

Over the last 90 days, the number of unique addresses holding a Set has grown by ~48% from 1,300 to 1,920. You'll also notice on the chart below that the launch of Set Social Trading on January 21st contributed significantly to this growth.

Since the launch of Trend Trading on TokenSets roughly 6 months ago, we've managed to cultivate a healthy and competitive rebalancing marketplace that 35 unique addresses have participated in. This is due to Set rebalances being open for anyone to participate in through using our Rebalancing Dashboard located here. The top 10 addresses that participate in rebalances are shown below (sorted by dollar volume).

Finally, cumulative Set purchase volume increased from $6.5 million to $8 million over the last ~30 days. This is likely due to the recent outperformance of most Sets and the launch of Set Social Trading.

📌 Uniswap

Contributor: Caleb Sheridan, co-founder of Blocklytics

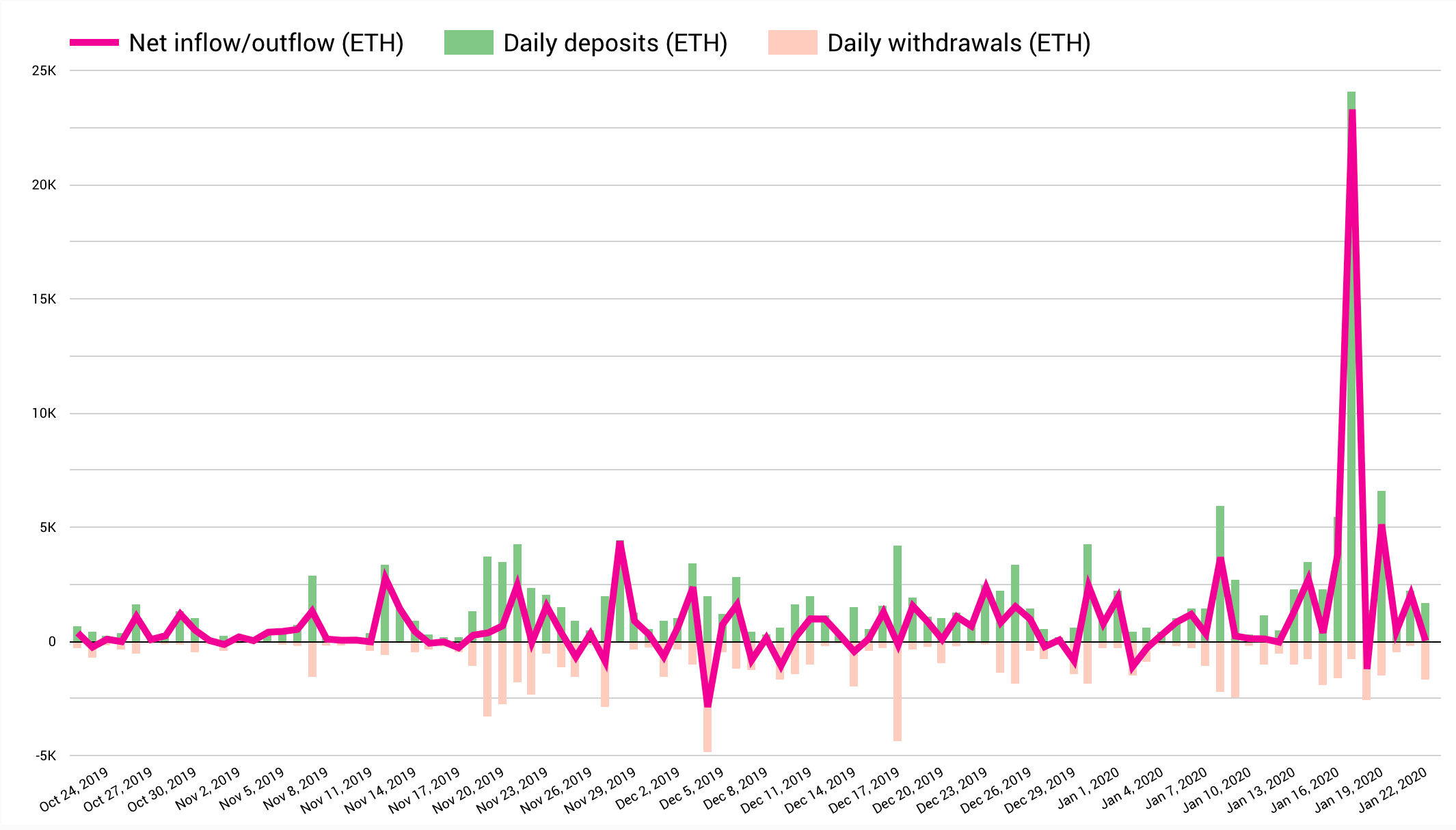

Uniswap net deposits are growing and healthy. January 17, 2020 was a major outlier: about $10m worth of liquidity was added. MKR, REP, and USDC pools have benefitted the most.

More liquidity is a requirement for facilitating big trades. Uniswap's design is often criticized since big trades generate slippage. However, that's generally been improving as pools are getting deeper. Looking at the top MKR trades this year, we can see how much slippage the biggest trades experienced. Note the 200+ ETH trade fulfilled with <1% slippage after the January 17th liquidity boost.

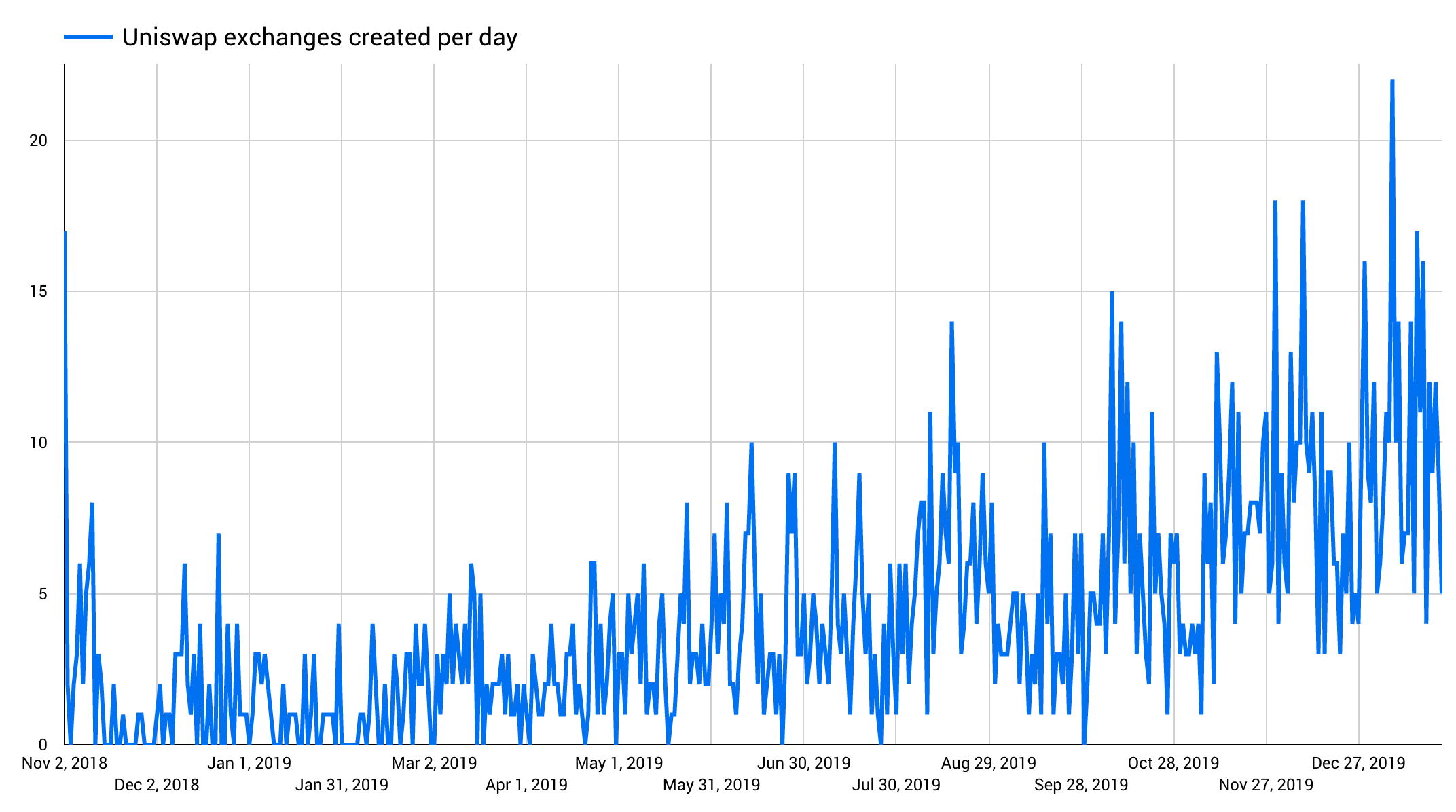

Uniswap has nearly 2000 exchanges. Anyone may create an exchange for any token. Anecdotally, we see the community taking to this concept (examples follow). And, reviewing the number of new markets per day, we also see an upward trend with a record 22 new markets created on January 7, 2020.

Uniswap has become the go-to exchange for starting innovative markets for tokenized goods, services and more. Examples of recent launches include $PEW (tokenized retweets), $MAGIC (hours for consulting), $CAFE (roasted coffee), and $FAME (apparel).

Our Network is a weekly newsletter where top blockchain projects and their communities share data-driven insights. Subscribe now to receive a crash course in on-chain metrics and never miss an issue.

About the editor: Spencer Noon leads investments for DTC Capital, a fundamentals-focused crypto fund. He actively tweets about on-chain metrics.