Never miss an update — click here to follow Our Network on Twitter.

This is issue #44 of Our Network, the on-chain analytics newsletter that reaches nearly 6000 crypto investors, analysts, researchers, and builders every week 📈

This week our contributor analysts cover DeFi: 0x, Curve, Keep Network & tBTC, and Stablecoins.

① 0x

Contributor: Danning Sui, Data Scientist at 0x Labs

It’s been a year with lots of developments in DeFi, as well as for 0x. The chart below shows the combined 0x trading volume per month, from both protocol and API levels. It breaks down the trading volume by a few types:

settled on v2 protocol (v2.1) or v3 protocol, with 0x native liquidity;

settled on v3 protocol, with liquidity sourced via bridges from other protocols;

or sent by 0x Exchange Proxy and settled directly on Uniswap v2/Sushiswap.

The daily volume climbed from ~4m at the beginning of this year to ~40m now, a 10X growth. This steady volume growth is attributed to the user growth both in the taker side as well as the maker side. Since the end of June, Matcha has started to aggregate liquidity by tapping into 0x API and has grown its user base since. It has now cumulatively onboarded ~3.4k individual traders. While on the protocol side, 0x has been building liquidity bridges to source across 17 protocols for better price and more liquidity. A few professional Market Makers also entered the game and started providing 0x exclusive liquidity directly into the protocol, which can be seen by the recent growth in the Tokenlon app.

10 days in, with only ~10% of Metamask users being exposed to the swap features, Metamask has filled ~$2M volume through 0x API making it the 2nd largest integrator besides Matcha. At its peak, Metamask made up to 5% of 0x API volume share, with a daily total over $700k.

In the week of September 7th, Matcha’s weekly volume rocketed from 27.9m to 118.6m showing a 4.25X growth and stayed steady around ~80m per week after the spike. It is consistent with the user growth trend — with a 2-week lag — that in the last week in August, weekly user count grew by ~257%, from 157 to 404.

As the volume spiked around the Ethereum gas peak time (Sep 1st ~ Sep 17th), one of the reasons behind this growth can be Matcha’s lower gas consumption advantage. The team has been focusing on optimizing the routing mechanisms behind 0x API (Matcha) to achieve a lower total gas cost for users. We believe the “adjusted price” (with gas fee considered on top of quoted price) is the gold metric for aggregators, especially when gas price fluctuates heavily. Simulation report shows that trades on Uniswap via Matcha are cheaper than direct trades on Uniswap. (full report link)

As one of the improvements in our liquidity matching logic, Bunny Hop is a way to bridge an illiquid pair (or when there is an intermediary token of greater liquidity that can connect the requested pair) to help the trader get liquidity sourced for a better price. When a new token (e.g. renBTC) is created, it is usually only available on certain protocol pools and for certain trading pairs (e.g. WBTC-renBTC). In this case, for example, if someone wants to trade DAI-renBTC, Bunny Hop will find the bridge and route of the best price (e.g. DAI-WBTC/WBTC-renBTC). Note that this differs from splitting orders, as Bunny Hop considers the whole size of order for each hop.

Since its deployment in late August, there have been 40,083 hops until today and below we visualized all of them in a network. Each node represents a token and its size shows how many times it’s been sourced in the hops. Each edge represents a trade and the size of the edge measures the total volume between that pair historically. We can see that WETH and stablecoins (DAI, USDT, TUSD) have been the main bridges of liquidity, followed by a cluster of DeFi tokens on the left. Leaf nodes in the graph below show the newly traded tokens that needed the hops (on the right side).

② Curve

Contributor: Michael Egorov, Founder of Curve

Admin Fees. The community-lead proposal to align incentives between veCRV holders (governance participants) and liquidity providers got off to a very strong start with total fees accrued reaching $1m in its first month. Governance subsequently chose to distribute those fees as 3Pool LP tokens which will start in the coming weeks.

Lock Rate. After the admin fee proposal was approved by governance, lock rates started to rise. They were around 10% of the total supply and currently stand at 17% and growing rapidly.

Volume. September brought new records to the Curve protocol with volumes reaching above $5B as well as a new daily record of over $550M.

veCRV Decentralization. With the number of vote locked users fast approaching 3,000, the DAO has become increasingly decentralized with voters holding under 0.5% of voting power accounting for 46% of the total voting power, in stark contrast of early days of decentralized governance.

August 22nd (200 locks) vs September 22nd (1991 locks) vs today (2817 locks)

Source 1 / Source 2 / Source 3

Holder Growth. Meanwhile, total volume reached $10B on October 14th continuing a trend of astounding growth for pegged assets swaps and on-chain trading. To put the rise of Curve and DeFi in perspective, Curve took nearly seven months to reach $1B in volume and managed to reach $1B volume in under four days in late September.

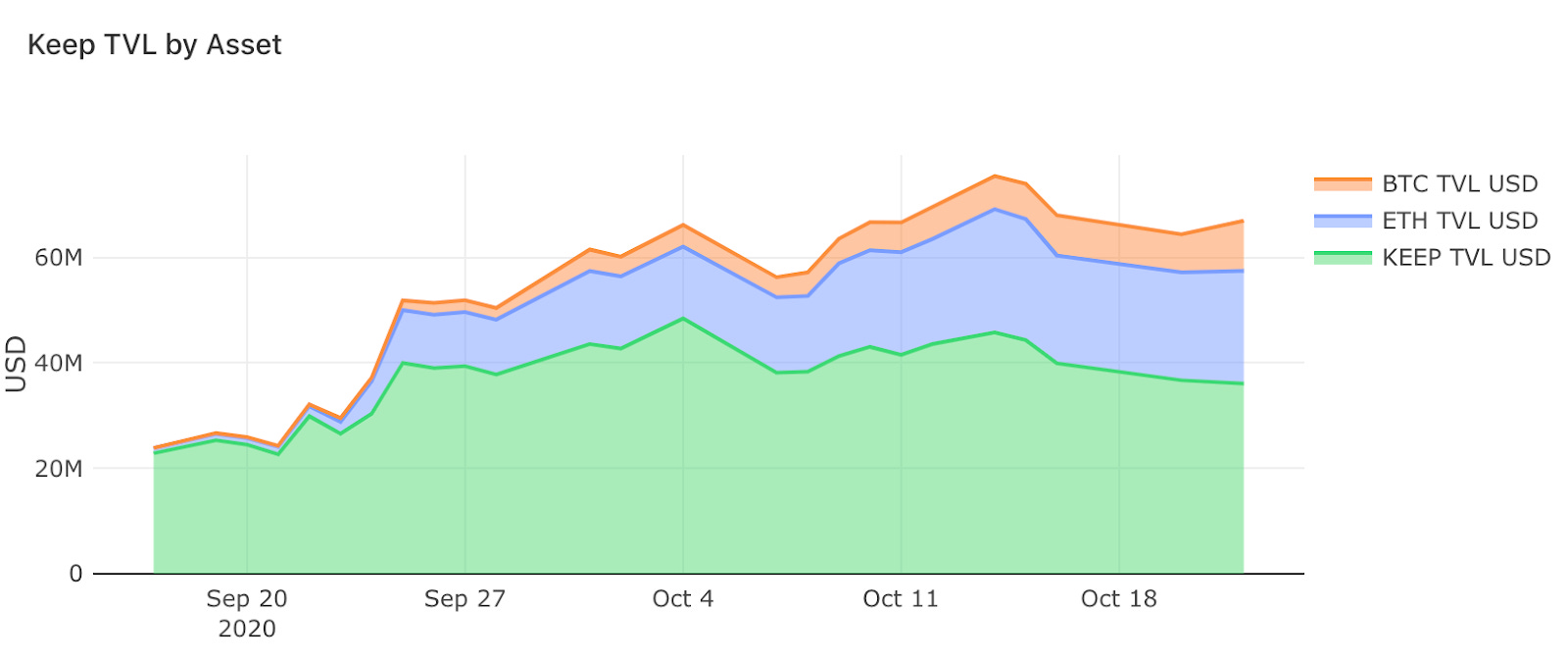

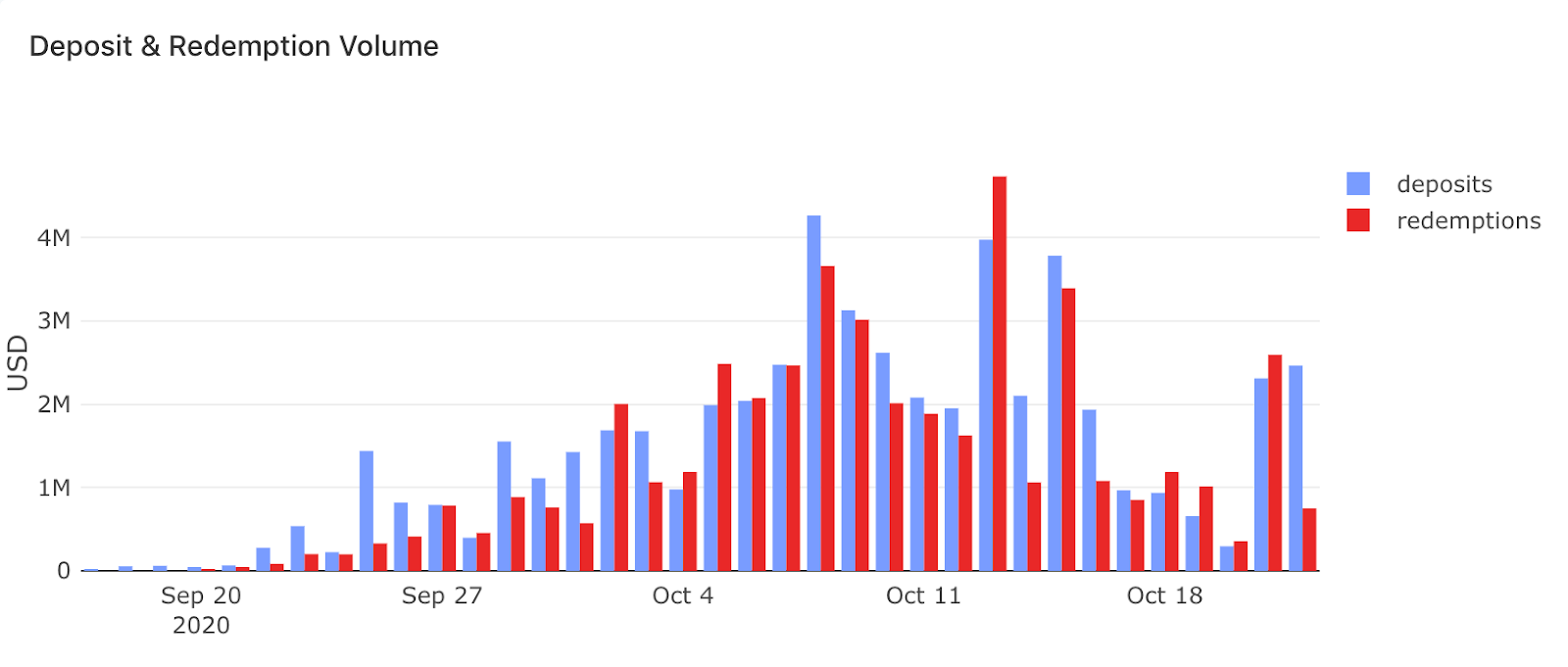

③ Keep Network & tBTC

Contributor: Jon Itzler, Research at Accomplice

Since relaunching on September 17, Keep’s first cross-chain bridge has facilitated 4,761 BTC (~$53M USD) in cumulative deposit volume by 205 unique addresses, with daily deposit volumes reaching up to ~$4M USD. 10-BTC lot sizes for deposits were enabled shortly after launch, quickly becoming the most popular deposit sizing with 399 10-BTC deposits and counting. 4,068 tBTC, or ~85% of all deposits, have been redeemed back for the underlying Bitcoin.

On the signer side, over 53,700 ETH is currently staked, with ~36,200 ETH bonded as collateral backing tBTC by 67 unique operator addresses. The systemwide collateralization ratio over the first month has averaged 177%, with a total of 2,563 ETH (~$1M USD) in cumulative signer liquidations.

Of the 745 tBTC outstanding, ~57% of the supply has been supplied as liquidity to various automated market makers. Sushiswap represents the majority with 395 tBTC in the incentivized tBTC/WBTC pool (also being incentivized by harvest.finance).

More than 75M KEEP have been staked across ECDSA & Random Beacon nodes, giving the project a TVL of ~$67M after its first month ($36M in KEEP, $21M in ETH, $9.5M in BTC).