Continued from Part 1.

The majority of largest vaults are directly or indirectly involved in yield farming activities, mostly at Compound. The USDC-A vault owners have the most leveraged positions, which is evident in low account liquidity. Maker recently changed the liquidation ratio for USDC-A from 120% to 110% in order to potentially reduce DAI premium (either by helping market makers to be more aggressive at shorting DAI or by flooding markets with DAI to reduce farming yields).

In practice, the change primarily increased farming yields for these individuals, as the vast majority of DAI issued by USDC vaults recently ended up in Compound. It is yet to be seen how much more DAI is needed to reduce the DAI premium or farming yields, but the number could be very high, particularly due to DAI weight dynamics in liquidity pools such as Curve explained earlier.

Liquidation risks at Maker clearly increased with rising DAI debt exposure. If another Black Thursday even occurs in which ETH drops 50% ($160) and BTC 40% ($6,600), 165m debt would be liquidated or about 50% of DAI supply. This compares to 20% of DAI supply liquidated on Black Thursday and shows that recently increased debt exposure carries lower collateralization of vaults and implies much higher liquidation risks. It is questionable if the system could handle such high degree of liquidations and potentially Circuit Breaker would need to be triggered.

On the other hand, a lot of larger Vaults have their DAI parked in Compound and YFII farms which means that they should be able to unwind their positions quickly before liquidations happen due to 1 hour OSM delay.

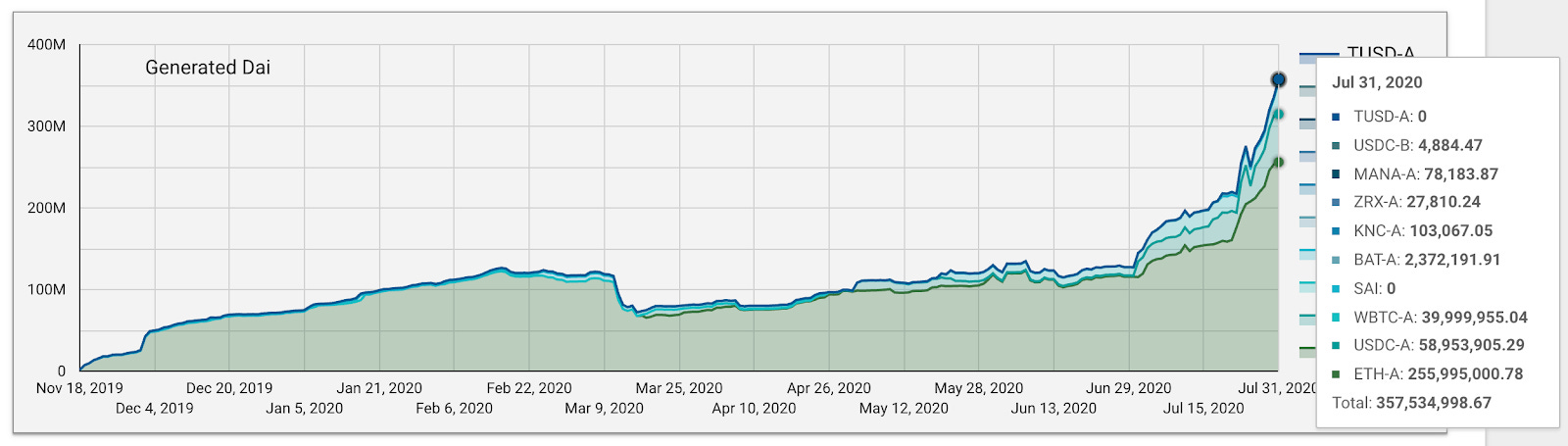

Finally, DAI supply increased by 244m from 115m to 359m in just 45 days, which coincides with Compound starting the yield farming craze. During this period, the ETH debt ceiling was increased 5 times, from 140m to 340m.

Total increases in DAI debt in last 45 days:

ETH Vaults: +154m DAI

USDC Vaults: +57m DAI

WBTC Vaults: +30m DAI

BAT Vaults: +2m DAI