Our Network: Issue #28

Coverage on DEX.

This is issue #28 of Our Network, the free newsletter about on-chain analytics that reaches nearly 3000 crypto investors every week.

This week our contributors cover projects in the DEX ecosystem: Curve, Kyber, 0x, dYdX, and Uniswap.

1. Curve

Contributor: Michael Egorov, Founder of Curve Finance

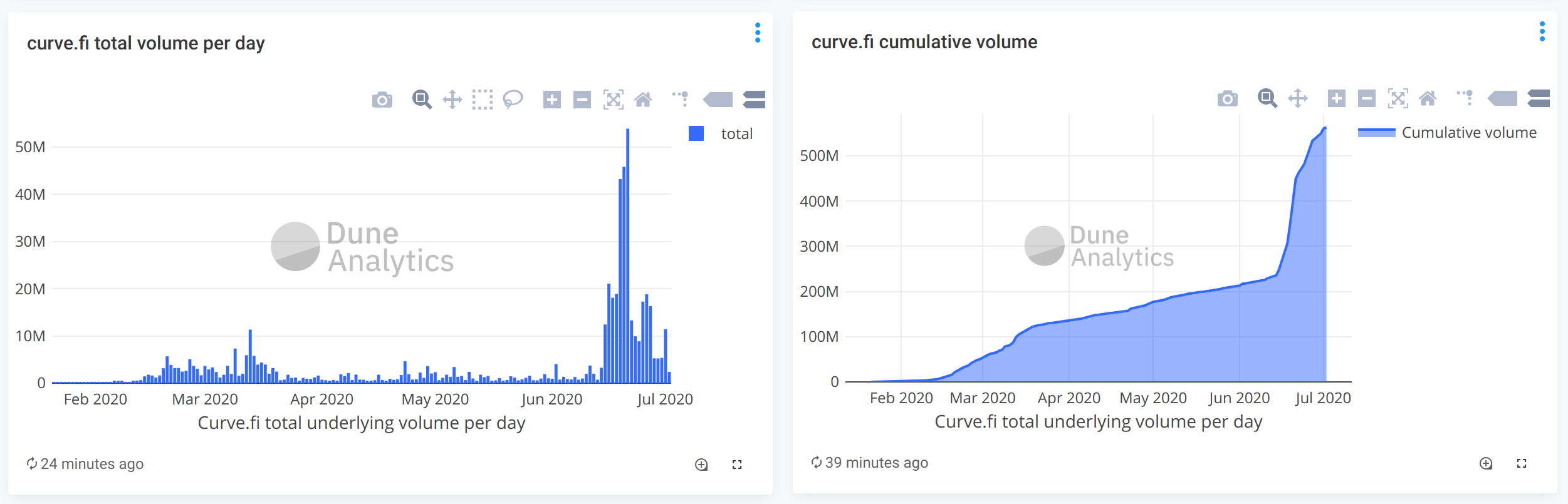

Curve is an automated market-maker for stablecoins and similarly priced assets, launched in January 2020, currently holding $52.5M in liquidity (source). Due to a specific bonding curve optimized for such assets, it is 100-1000 times (depending on the configuration) more effective in terms of slippage than Uniswap for Balancer for the same task. Currently, Curve supports most popular stablecoins, and also 3 types of Bitcoin on Ethereum. Users can exchange between similar types of assets, or deposit them to earn yield from trading fees, reward programs and/or lending.

Following its inception and the initial growth, Curve was absorbing 1-2M in daily trading volume on average until recently. When Compound introduced COMP distribution, it created unprecedented demand for exchange of stablecoins. Trading volumes touched $60M daily, with total trading volume over all time of existence of the platform exceeding $500M (source).

Growth of trading volumes, in turn, elevated the returns. Annualized daily returns were exceeding 100% APY at the peak of the demand. Currently, the returns sit at 6% APY for the pool on the graph (Y pool, consisting of DAI+USDC+USDT+TUSD - a pool profiting from both market-making and lending). For an SUSD (DAI+USDC+USDT+SUSD) pool subsidized by SNX current annualized daily return rate is 23% APY. (Source)

Increased trading volumes caused profitability spike which tripled the deposits. That increased market depth tenfold (image) and, hence, usefulness of the pools - thanks to the demand driven by token incentives of other protocols. Currently selling $5M USDC for USDT can be done with 0.4% slippage. We give 3M dollar swap as an example [link] - this transaction was done through 1inch.exchange but went through Curve pools. (Source)

Almost half of the weekly trading volume consists of USDC<>USDT swaps - the most popular to facilitate COMP farming. It is notable that swaps between RenBTC and WBTC (usually facilitated as a way to convert real Bitcoin to WBTC trustlessly), and between SUSD and USDC amount for 6% of weekly trading volume each. (Source)

2. Kyber

Contributor: Deniz Omer, Head of Ecosystem Growth at Kyber

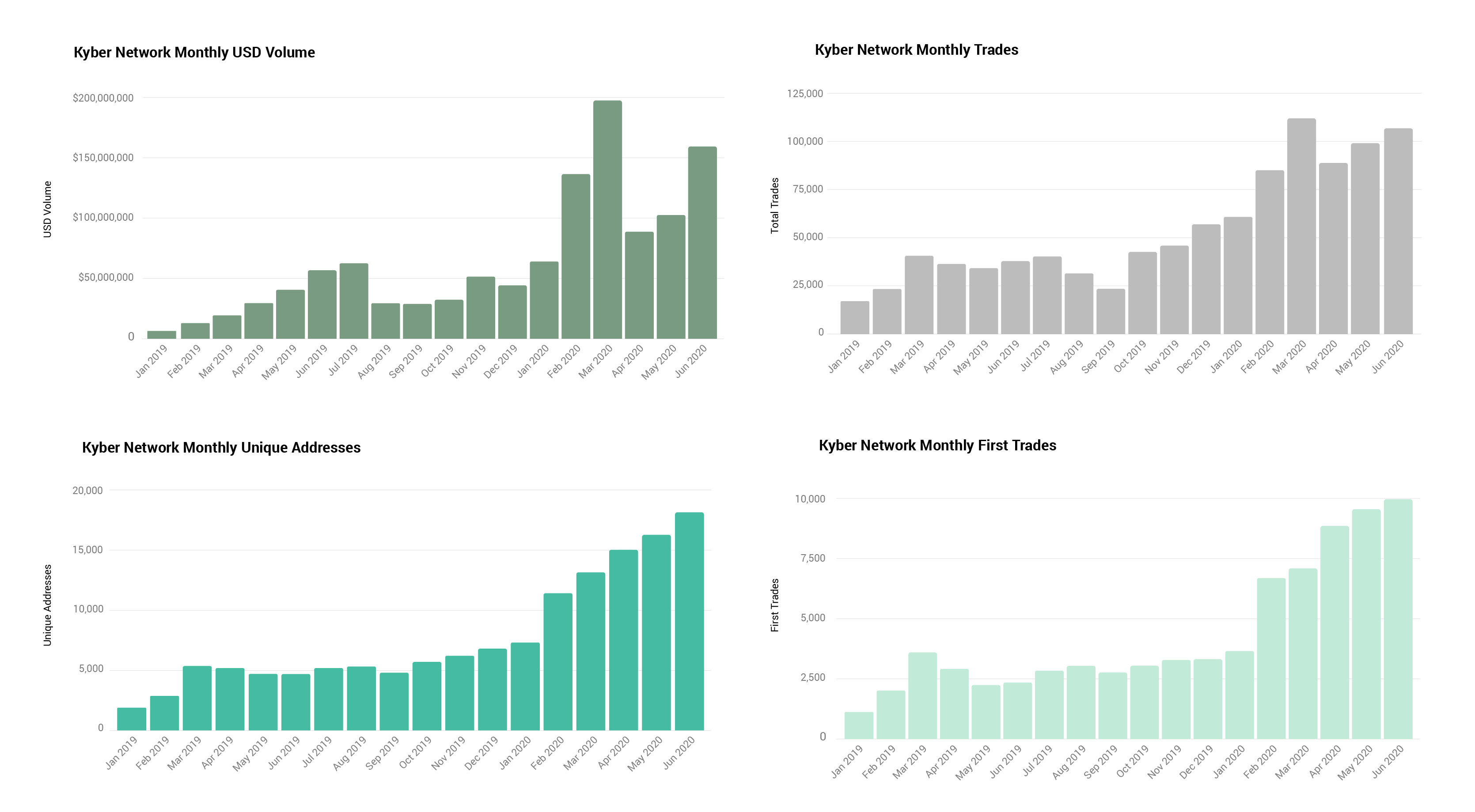

Ever since DeFi first came into our consciousness in late 2018 and early 2019 it’s seen its repertoire grow in terms of both product innovation and the ability to scale up liquidity. Of course the fast pace of innovation has led to increased risks as services are combined to build unique new products but at its core, the basic infrastructure pieces like liquidity protocols have kept seeing increasing volumes, increasing new users, and increasing number of trades at liquidity rates (calculated as slippage + spread, not TVL) unimaginable just a year ago.

Top consumers of Kyber Network’s liquidity continues to be KyberSwap, 1inch and other wallets and DeFi dapps. 1inch has seen especially strong growth with an increase in volume through Kyber from ~$8M in both April and May to $24M in June. Traders and dapps without registered wallet addresses make up another quarter of Kyber’s volume while more than 20 Kyber integrations have more than $1M monthly volumes.

Professional market makers dominate Kyber Network’s liquidity provision accounting for 2/3rds of all volume. They are followed by DEX bridge reserves connected to Uniswap and Oasis which make up almost 20%, followed by a long tail of 40+ automated market maker reserves deployed by token teams providing liquidity to their respective tokens.

Crypto’s growing adoption across the world is reflected in KyberSwap’s geographic data as we see users from over 100 countries swap tokens with more than 50 countries carrying out monthly traders in the six and seven digits. The US continues to be the largest market accounting for almost 30% of all volumes while European countries make up half of the top 10.

3. 0x

Contributor: Alex Kroeger, Data Scientist at 0x

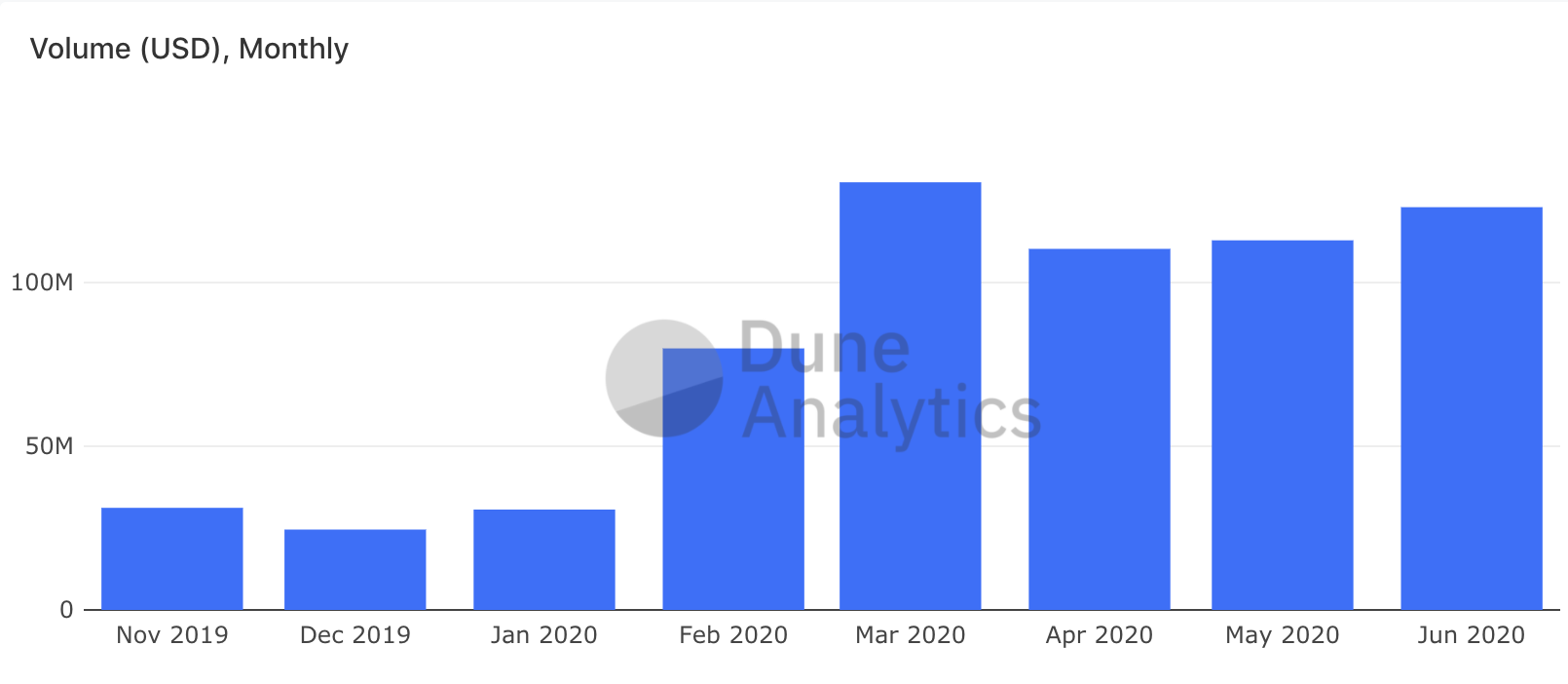

It’s been booming time for DEXs. 0x volume grew 9% month-over-month to $123M in June.

June was also the biggest month ever for the USD value protocol fees paid on version 3 of the protocol, totaling $25K. (Source)

On June 30, 0x Labs officially launched Matcha, a simple trading interface powered by liquidity sourced from 0x API. Since the launch, over 100 traders have tried it out and cumulative volume since the start of the beta passed $2M. High level stats for Matcha can be found on Dune Analytics.

Higher fees have translated to higher returns to staked ZRX holders. Stakers with Volleyfire have earned the highest returns for the most recent epoch at 3% annualized. (Source)

On the back of higher rewards, the amount of ZRX staked has reached highs both in terms of ZRX and USD value to 21.9M ZRX (~$7.5M). (Source)