Our Network: Issue #27

Coverage on L1 Networks.

Are you a loyal reader? Click here to support Our Network on Gitcoin Grants

This is issue #27 of Our Network, the free newsletter about on-chain analytics that reaches nearly 3000 crypto investors every week.

This week our contributors cover Tezos, Ethereum, Bitcoin, Decred, and Cosmos.

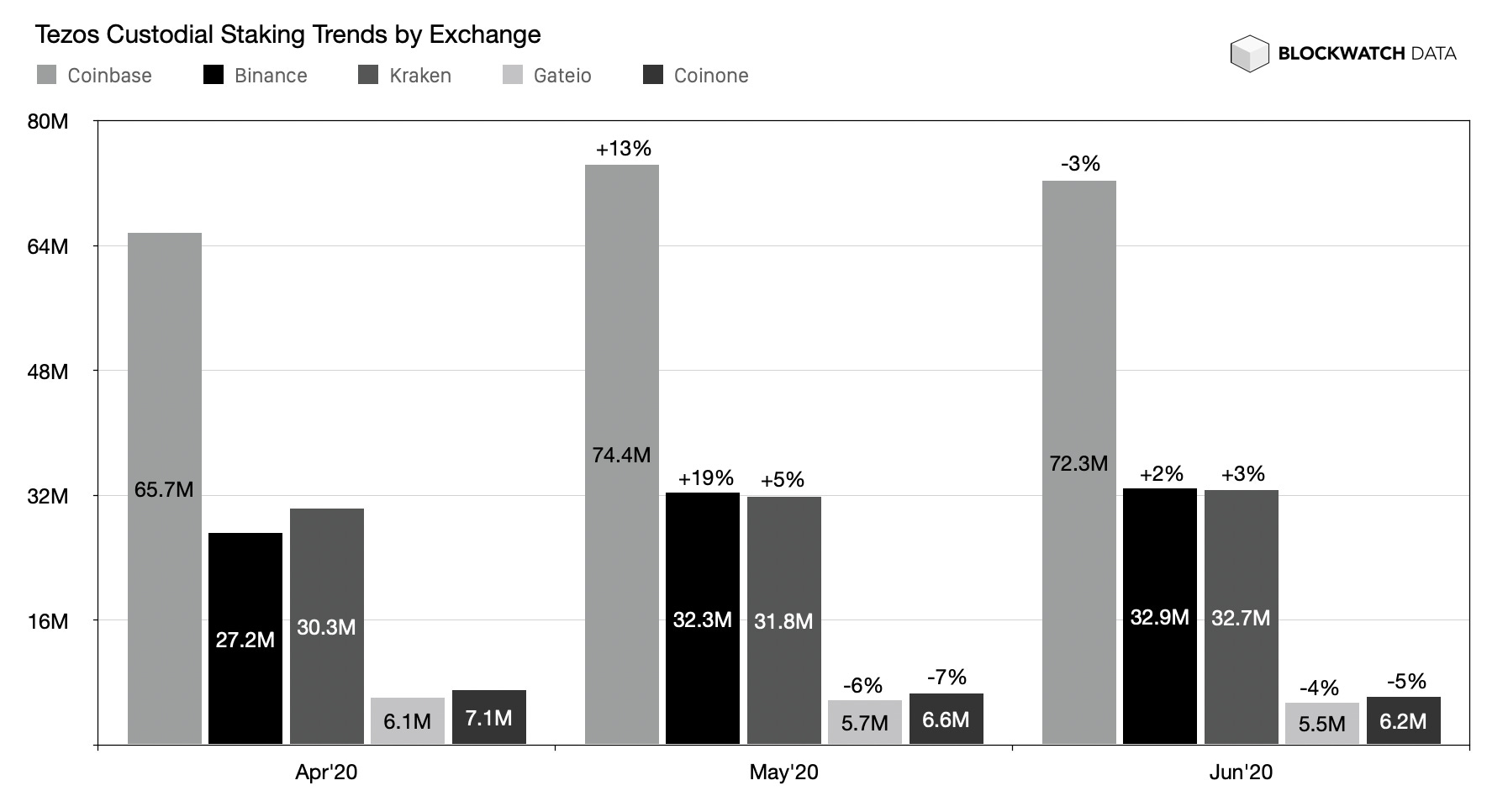

1. Tezos

Contributor: Alexander Eichhorn, Founder at Blockwatch Data

Staking: Tezos' network-wide staking ratio is at 80.27%, close to its ATH of 80.4% from end of May 2020. This also means staking rewards for everybody are at an all-time low of 5.93% with a yield above inflation of only 0.94%. The most interesting development is that the meteoric rise of custodial staking which started last October has stopped. In fact, the amount staked across all top 6 custodians fell by -0.7% to 151.6M tez since I last reported in mid-May. Now all custodians combined control 18% of Tezos' consensus. At the same time, network-wide stake grew slightly by +0.8% (+5.6M tez) which suggests new delegators chose community bakers despite the convenience of exchanges.

Churn: In Tezos, delegators can freely move their coins or switch bakers at any point in time. Lockup time only exists for baker security deposits. This means people could re-delegate, sell or arbitrage all the time. A great metric to visualize the situation and detect long-term shifts in loyalty is to look at churn rate, in particular, how many delegators empty their accounts, maybe migrate to centralized custodians or sell their stake over time. Overall, delegator churn on Tezos is surprisingly low (between 3 and 11%) and we see a positive correlation with price shifts. When the price goes up, churn goes up as well because some people sell. When the price goes down, churn goes down too, suggesting there are only very few traders in the Tezos community. Clearly, most people are in it for the long term.

Growth: The total number of new Tezos delegators continued to grow and reached its highest growth ever (+7.5k) in May and is set to keep this pace in June. Over its short 2 years of existence, Tezos went through two growth epochs already and is in the middle of its third. I call them the Early Backers (Jun'18 - Mar'19), the 2019 Boomers (Apr'19 - Oct'19), and the Brrrr Generation (Nov'19 - now). Each epoch started with an up-tick in delegator growth, then continued with a dramatic price surge and an increase in delegator churn (see graph above), followed by price and churn decline. Eventually, an epochs ended with a new low in delegator churn rate. At the end of each epoch, Tezos had gained 2-3x more delegators. The most recent epoch seems to be not over yet, although churn is declining, delegator growth keeps increasing while at the same time the custodial uptrend is broken.

Adoption: Development activity in Tezos is steady and strong. Many teams are working on infrastructure projects like price oracles, value oracles, document management, asset tokens, asset standards development, and exchange platforms. Most of these projects haven't made it to mainnet yet, which is a good thing, since the Tezos contract developer community puts as much emphasis on security and correctness as the core teams. Meanwhile, core is ramping up efforts for the next amendment process towards protocol version 007 which will be an exciting and feature-rich release. We will probably first see an early testnet before upgrade voting starts on mainnet in late summer.

2. Ethereum

Contributor: Santiment

It appears that Ethereum miners are once again back to accumulating ETH, adding more than 21,000 ETH in the past 20 days alone. The latest uptrend comes after a string of short-term miner selloffs in late May and early June following ETH’s rise above $220, which coincided with the start of Ethereum’s consolidation phase. The prolonged periods of miner accumulation can indicate fairly high confidence levels among ETH mining pools in relation to the asset’s short-term performance. As such, it’s particularly notable that the Ethereum miners have decided to sit on their block rewards for almost the entire (unconventionally lethargic) month of June and some growing concerns about Ethereum’s market performance.

The amount of addresses interacting with (sending or receiving) ETH each day has been on a decided three-month uptrend, and is now quickly approaching the activity levels recorded around Ethereum’s 2019 top. In the past 24 hours alone, over 441,000 addresses have sent or received ETH - the network’s highest single-day engagement since June 12th, 2019. What’s particularly notable about Ethereum’s recent network activity is that previous surges in Ethereum’s daily active addresses often coincided with a strong price rally for the second biggest coin by market cap. The current uptrend, however, comes in the face of a weeks-long consolidation period for ETH, and marks a rare but strong decoupling trend between Ethereum’s price action and the network’s utilization.

Ethereum’s Token Age Consumed, which tracks the activity of previously dormant coins, recently spiked to its highest level since February 2019, indicating that a substantial amount of previously idle ETH is once again moving between addresses. The current TAC spike has even eclipsed the one recorded on Black Thursday, when a number of long-term Ethereum holders migrated their holdings to exchanges in reaction to the market-wide drop. Spikes in Token Age Consumed can sometimes signal changes in the behavior of certain long-term holders, and tend to precede increased volatility in the coin's price action. The latest spike is most likely due to the sudden movement of 789,534 ETH (~$184,000,000) from the known PlusToken address, a notorious ponzi scheme which now seems to be attempting to ‘launder’ their coins by splitting it up into thousands of smaller transactions on the Ethereum network.

The total gas used on the Ethereum blockchain has reached a new all time high in the past week, coinciding with the vote by Ethereum miners to increase the block gas limit by 25% (from 10,000,000 to 12,500,000). In theory, this would allow the Ethereum network now the capacity to handle around 44 transactions per second, instead of the previous limit of around 35. However, Ethereum’s on-chain transaction volume has remained fairly stable over the past week, indicating that the surge in the total gas usage likely originates from the increased use of more complex smart contracts which, in turn, require more gas. This is further in line with the documented growth in the utility of DeFi-related solutions like Uniswap and Kyber Network, both of which rank in the top 10 by gas usage in the past 30 days.

Ethereum’s token velocity hits 2-year high. The average amount of times that active Ethereum tokens change addresses recently spiked to 5.2/day - its highest value since the shutdown of the notorious ETH mixer that operated until early 2018. Higher velocity means that each token is used more often in daily transactions (rather than a one-off exchange) and is often associated with healthy network activity. The latest spike in Ethereum’s velocity is unlikely to be price-related, and might well be prompted by the increased opportunities for ‘yield hunting’ on various DeFi protocols.

3. Bitcoin

Contributor: Nate Maddrey, Research Analyst at Coin Metrics

Some interesting trends have emerged as Bitcoin continues to rebound three months after the March 12th crash. Bitcoin daily active addresses (defined as the unique number of addresses either sending or receiving a transaction) are approaching levels not seen since 2018. Active addresses tend to follow price, as seen in the below chart. But in May and June there were several days where Bitcoin had over 1M active addresses, despite price mostly remaining under $10K. The last time Bitcoin had over 1M daily active addresses was July 2019, when price peaked around $11,500. The following chart shows daily active addresses smoothed using a 7 day rolling average (green line, left hand axis) vs. price, USD (red line, right hand axis).

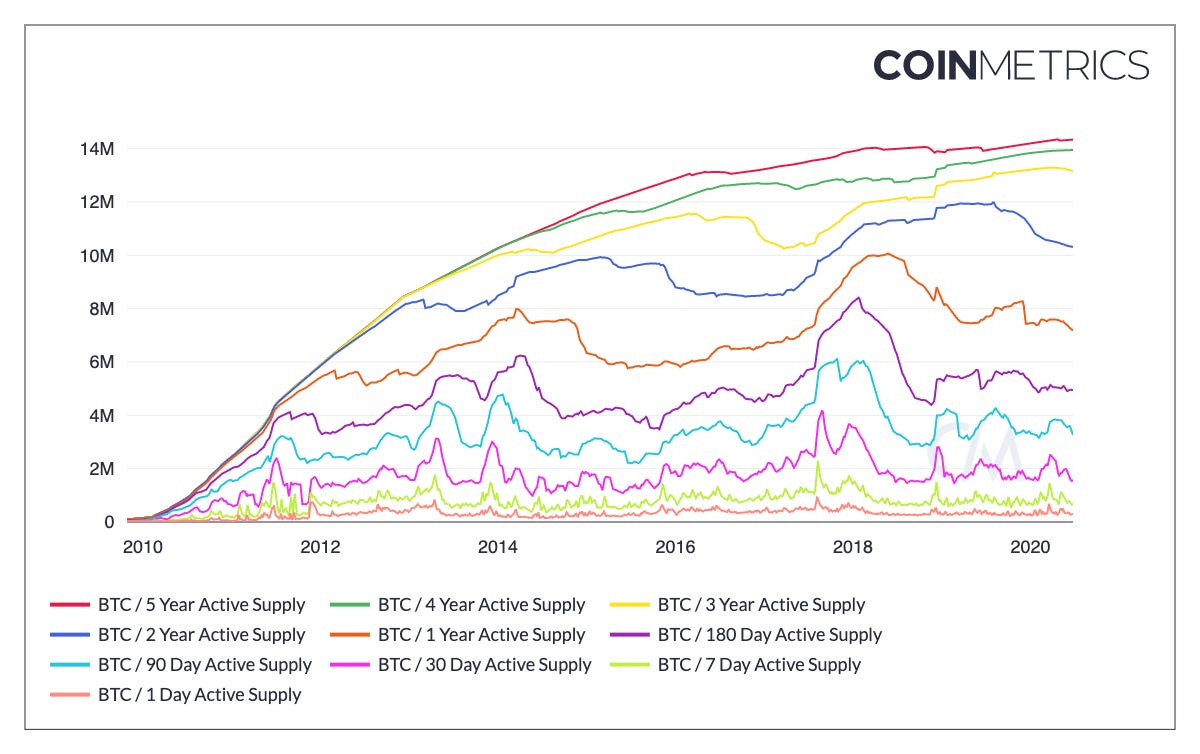

While active addresses have been rising, active supply has been falling. Active supply is a measurement of the amount of supply that has moved on-chain within the last X days or years. The following chart shows BTC active supply ranging from 1 day to 5 years. Although short-term active supply (90 day and below) surged in early 2020, longer-term active supply has dropped. Specifically, 1 year and 2 year active supply have both dropped to two year lows. This implies that supply is increasingly being held for periods longer than one year, which supports the narrative that BTC is used as a store of value. About 10.35M BTC have moved on-chain within the last two years, while about 7.4M have moved within the last year.

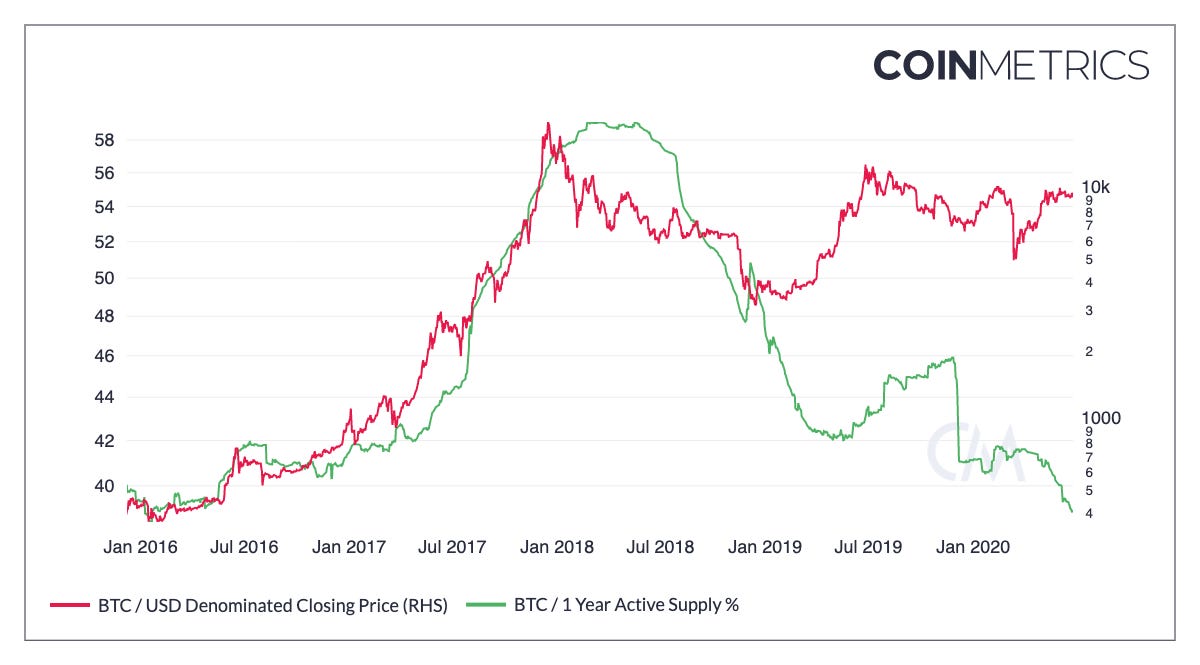

One year active supply percentage paints a similar picture. Looking at active supply as a percentage of total (as opposed to raw active supply numbers) helps account for increases in supply. As of June 23rd, BTC one year active supply percentage (i.e. the percent of supply active within the last year) was about 38.93%. The last time it was under 40% was May 2016.

Additionally, Bitcoin realized capitalization has recovered the losses following March 12th and reached a new all-time high of $106.97B. Realized cap is calculated by valuing each unit of supply at the price it last moved on-chain (i.e. the last time it was transacted). This is in contrast to traditional market capitalization which values each unit of supply uniformly at the current market price. Realized cap therefore better accounts for units of supply that have not moved in a long time, and gives a more accurate view of market capitalization.