Our Network: Issue #23

Coverage on BAT, LINK, Nexus Mutual, Opyn, and PoolTogether.

Click here to join our telegram chat.

Welcome to Issue #23 of Our Network, the newsletter about on-chain analytics that reaches more than 2000 crypto investors every week.

This week our contributors cover the following projects:

PoolTogether

Nexus Mutual

Chainlink

Opyn

Basic Attention Token 🆕

Network Coverage

🟢 PoolTogether

Contributor: Leighton Cusack, CEO of PoolTogether

PoolTogether is a protocol for no loss savings games on Ethereum. The two primary growth metrics are unique wallets with deposits and total deposited funds. Unique users have grown from 423 on January 3rd 2020, to 8,296 on May 28th. Monthly user growth is shown in the image below.

In contrast to the consistent user growth, total funds deposited has fluctuated up and down. Early in the year, the pool was dominated by $100,000+ deposits, this has been replaced by many more deposits from smaller holders.

The prizes the protocol awards are derived from the interest earned on all the deposited dollars, due to major decreases in interest rates (especially after the market crash in mid-March) total prizes awarded per month have also fluctuated. The following chart shows total prizes disbursed so far in 2020.

PoolTogether released the "pods" functionality enabling users to link their tickets together and automatically split any prize. The pods have grown to be the single largest ticket holders making them a unique investment vehicle. Currently, the Dai Pod has 82,060 tickets deposited in it, equating to a 1 in 6.43 chance of winning each week. Since the Dai pool has a total of 893,895 each time the Dai pod wins ticket holders are effectively earning 10x the interest they would have earned over the same period of time.

The Argent Wallet recently launched a direct integration into the PoolTogether protocol. This provides a good data point in how improving ease of use can expand protocol usage. Net new users increased 240% in the 10 days after the launch of the Argent integration compared to the 14 days prior to the integration launch. This shows significant untapped demand once onboarding is improved.

🟢 Nexus Mutual

Contributor: Richard Chen, Partner at 1confirmation

Two large covers of 1000 ETH (~$220k) each were taken out recently for DXdao and ParaSwap. You can keep track of all new covers with this Twitter bot.

Below are active cover amounts (in USD) on each project. Flexa ($550k), dYdX ($455k), Uniswap ($421k), and Compound ($405k) have the most money insured.

Active cover amount increased by 12% from $2.8M to $3.13M over the last month. There is still a lot of cover capacity available as currently the mutual can support up to $18.3M in total covers. The upcoming partial claims launch will expand coverage to not only smart contract bugs but also oracle risk.

Since inception 2032 NXM (worth $7169) in staking rewards has been paid out to NXM stakers. The upcoming pooled staking launch will increase staking rewards by 2.5x, encouraging more people to stake and thus decreasing the cost of covers.

🟢 Chainlink

Contributors: ChainLinkGod and CryptoSponge

This may not be news to you, but Ethereum’s blockspace is not free. Because of this, tracking the total percentage of blockspace (gas) being consumed by a protocol shows just how much stress (demand) an application is putting on Ethereum’s bandwidth. A higher level of gas consumption is bullish, but at the cost of making Ethereum transactions for everybody else.

The chart below shows what percentage of gas available each day is being consumed by Chainlink oracle networks. At mainnet launch, with only a single price feed (ETH/USD) and three nodes, Chainlink was consuming 0.33% of Ethereum’s daily bandwidth available. Over the course of 2019 this rose to a peak of 3.5% when there was two price feeds (ETH/USD and BTC/USD) each with 21 oracle nodes causing a 10x in bandwidth consumption.

There was peak up to 6% consumption during Black Thursday, but since then gas consumption has stayed nearly completely rock solid at 1% despite the fact that there are now 30+ price feeds supported by 30+ oracle nodes. One potential reason for this decrease and stabilization in gas consumption could be attributed to Chainlink networks moving to a deviation based schedule instead of just a heartbeat schedule thus matching the demand rhythms of Ethereum itself (as volatility goes up more liquidations and arbitrage happens), but if you have any other theories please let us know!

A key metric to visualizing the sustainability and profitability of running an active Chainlink node is overlapping the daily LINK rewards in USD to how much ETH in USD the data requesters and node operators spend daily on transaction fees (gas costs). To create a sustainable oracle network, rewards paid to nodes for external data needs to be higher than the costs spent by those nodes in delivering that data on-chain. The requesters total costs are LINK paid to nodes + ETH paid for data request transactions.

There was a very clear and obvious spike that occurred on the 12th and 13th of March, due to Black Thursday where Ethereum’s transaction fees skyrocketed. Since Chainlink oracle networks now update on a deviation basis, the more volatility there is, the more updates that need to be triggered, leading to such a large spike. On these particular days the USD spent on transaction gas costs are far higher than the rewards, but luckily these situations are an anomaly and do not affect the overall sustainability for running a node.

Lately average Ethereum gas fees have been far higher than normal digging into the profitability of running a Chainlink node. Most of these costs are borne by the requesters (currently the CL team) but a non-insignificant portion is also being paid by the nodes for their response transactions. If this continues into the future, LINK rewards to nodes may be bumped up, but with technical improvements to decreases gas consumption this will largely become a non-issue.

Each Price Feed built using the Chainlink framework pays a different amount of LINK rewards to oracle nodes depending on the security needs of each particular network (more security needed = more LINK needs to be paid to nodes). This is best represented by the below chart which compares the amount of total job runs (data requests to each node) per price feed to the amount of LINK rewards (provides economic security) per price feed.

What this shows is that while most networks have a similar amount of job runs per day, the ETH/USD (light blue) and BTC/USD (light green) networks are by far the highest paying price feeds in the Chainlink ecosystem. This intuitively makes sense as these particular feeds are not only high in demand by DeFi applications, but they contain a higher level of decentralization than most networks (21 nodes as opposed to 7-9) thus requiring more payments per update.

It’s also not too much of a surprise that the ETH/USD price feed is currently the most secure and in-demand Chainlink network on the Ethereum blockchain.

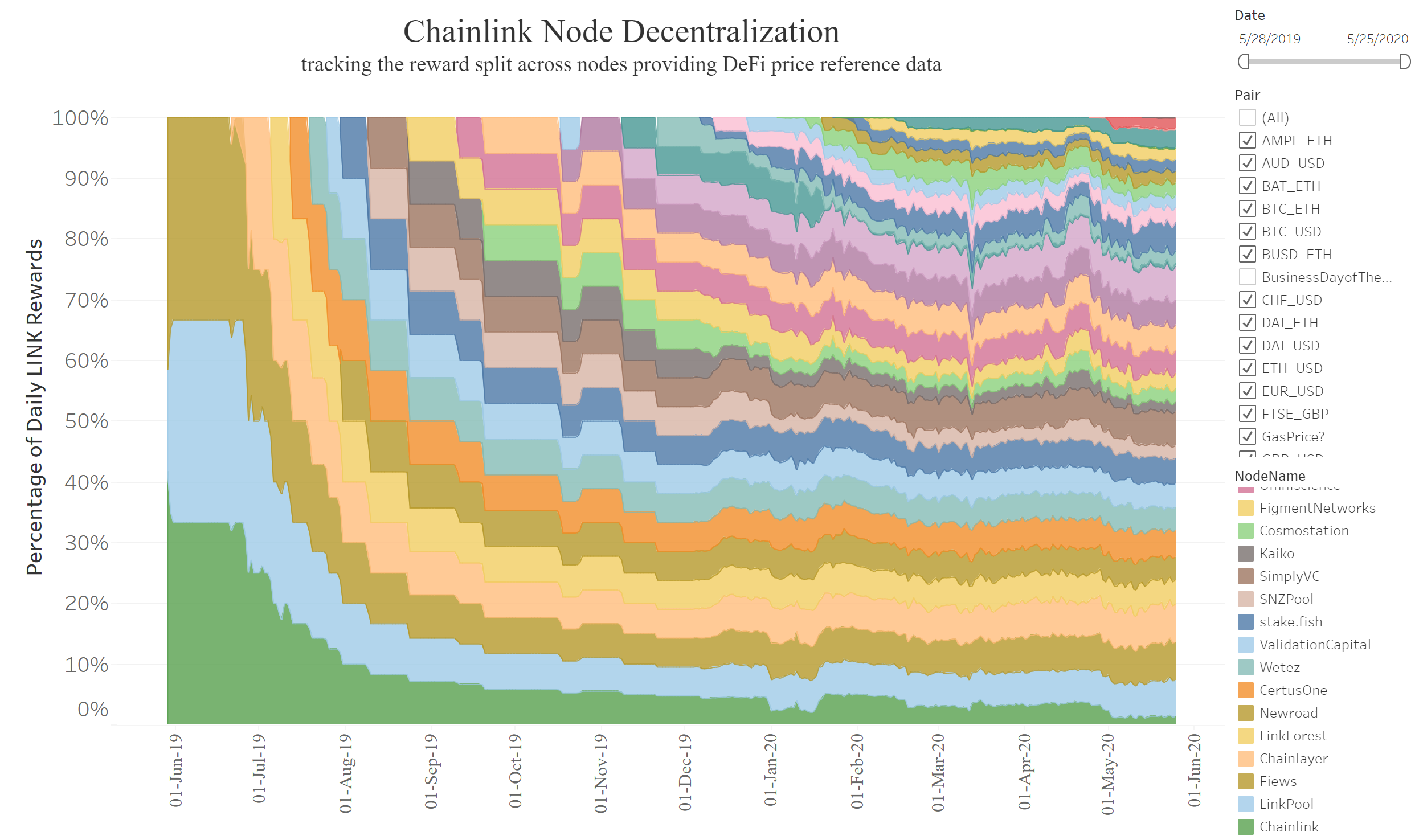

Zooming out and looking at the distribution of LINK payments paid to each active Chainlink node since mainnet launch in May 2019 gives some interesting information on the evolution of the Chainlink network. The first observation is that the network has been continually decentralizing over time. First only beginning with three nodes (Chainlink team, LinkPool, and Fiews), the network has since grown to over 30 active nodes, a 10x increase in decentralization.

The overall percentage of LINK payments paid to the Chainlink core team’s node has also drastically lowered over time. Initially beginning at 33.33% of the total daily payments, it has since lowered to only 1.34%. Additionally payments have become more variable in the last third of the chart due to the transition to a deviation based schedule. Additionally notice how each node is paid differently, this is due to the fact that not every Chainlink node is not equal in quality and thus do not serve the same amount of oracle networks.

Dig into the charts from today’s post here: Source 1, Source 2

🟢 Opyn

Contributor: Zubin Koticha, CEO of Opyn

Opyn provides DeFi risk management built using protective put option tokens called oTokens. Opyn provides protection on Compound deposits and ETH protection with ETH protective put options (oETH). At time of writing, there is currently an all time high of $2.17mm of collateral protecting ETH and Compound deposits (source).

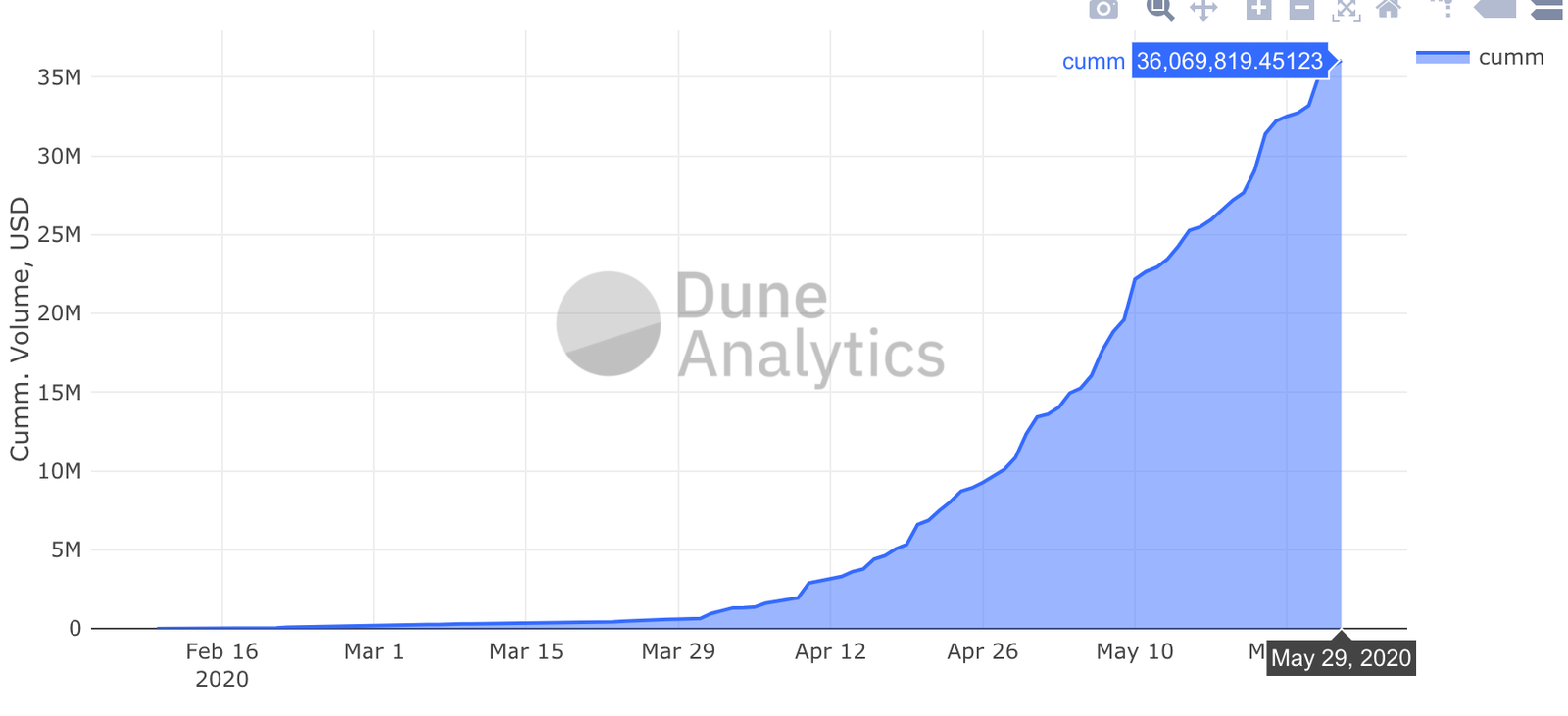

Opyn has 5x’d total notional volume in the past month with $36mm in notional volume since launch, $25.45mm in notional volume this past month and over $6.5mm in notional volume this past week (source). Notional = oETH * ETH price at time of trade. This is how notional is usually calculated for options in traditional finance (option * price of asset at time of trade).

Daily notional volume has doubled over the past month with $1.08mm seven day moving average for daily notional volume and $848k thirty day moving average for daily notional volume. Additionally, in the past month, Opyn hit a new daily volume record with $2.55mm in notional volume on May 10th (source).

In the last month the number of unique Ethereum addresses interacting with oTokens has doubled with, 752 unique Ethereum addresses having interacting with oTokens, protecting themselves against DeFi risks (source).

🟢 Basic Attention Token

Contributor: Blaise Cavalli, CEO and co-founder at Nyctale

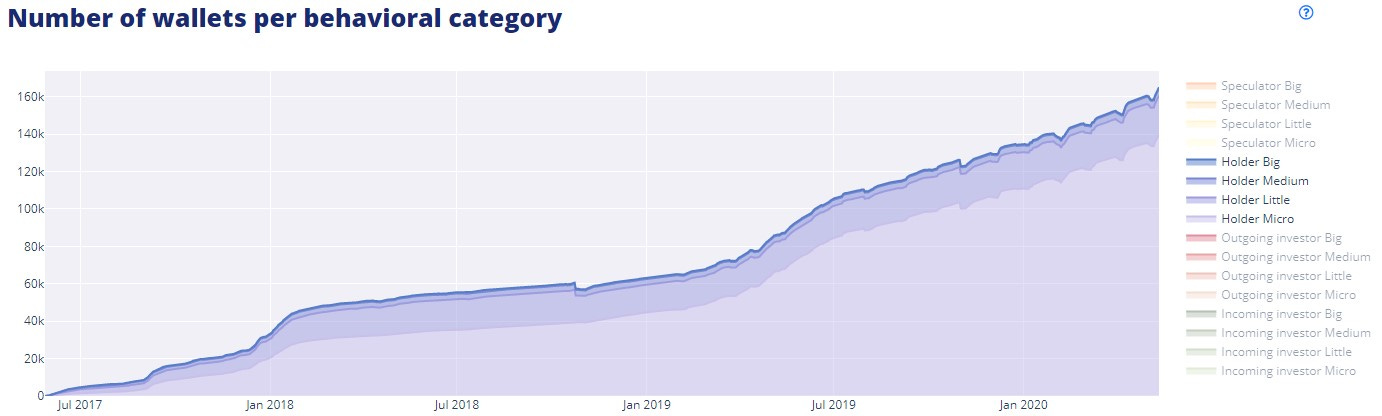

BAT network has an impressive long-term investor community, with more than 160k wallets exhibiting holder behavior (balance superior to 10 tokens, weekly ‘balance evolution’ < 25%, weekly ratio ‘exchange volume / initial balance’ < 25%). This indicator is:

Up from 90k wallets 12 months ago (75% annual growth rate from May 2019 to May 2020)

Up from 54k wallets 24 months ago (66% growth rate from May 2018 to May 2019)

BAT tokens are also owned by different sized crypto-investors. On the graphic below, the legend splits holders in the following categories: 10 tokens < Micro < 100 tokens < Little < 1.000 tokens < Medium < 10.000 tokens < Big. As you can see, most investors own less than 1k tokens.

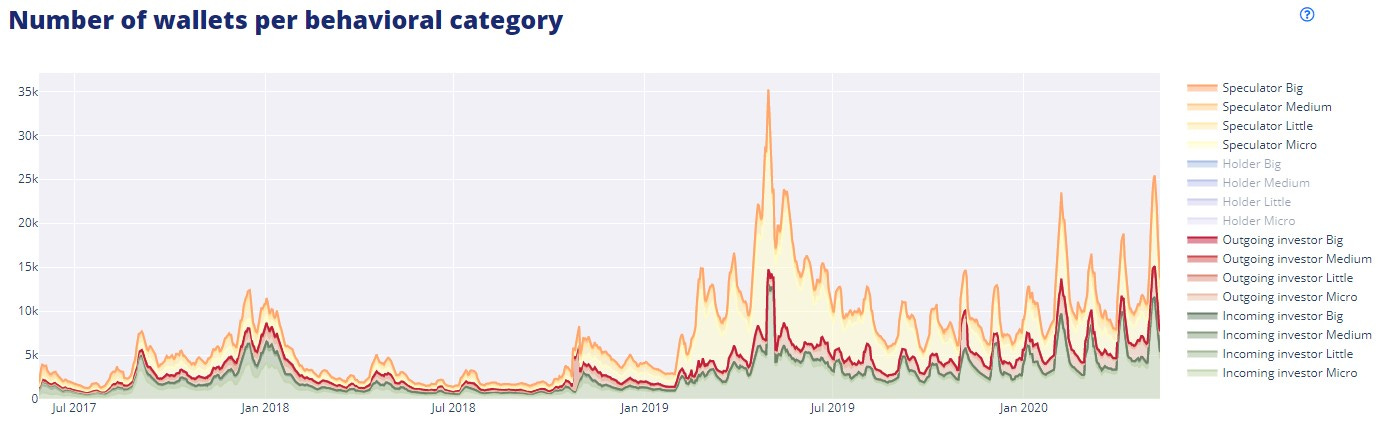

Dynamic wallets’ behaviors (labeled as ‘investors’ for a weekly balance evolution > 25%, and as ‘speculators’ for a weekly ratio ‘exchange volume / initial balance’ > 25%) are following a periodic pattern representing monthly advertisement payments.

Currently around 15k dynamic wallets on a weekly basis, up from 2k in June 2018 (650% growth rate in 24 months)

Clear sign of adoption and network usage beyond trading around exchange platforms (of which wallets have been excluded here)

The wealth distribution within Brave network has evolved with the different market cycles. The graphic below shows the percentage of wallets within the community owning 90% of all tokens in circulation (out of exchange platform’s wallets).

During the 2017 bull market, the wealth concentration has significantly decreased, reaching almost 25% for wallets owning 90% of tokens in circulation.

The 2018-19 bear market brought a break in this trend with a consolidation of wealth on a smaller part of the community, reaching the 10% level in late 2019.

Wealth concentration is now back to a decentralized trend with around 15% wallets holding 90% of tokens in circulation out of exchange platforms’ wallets.

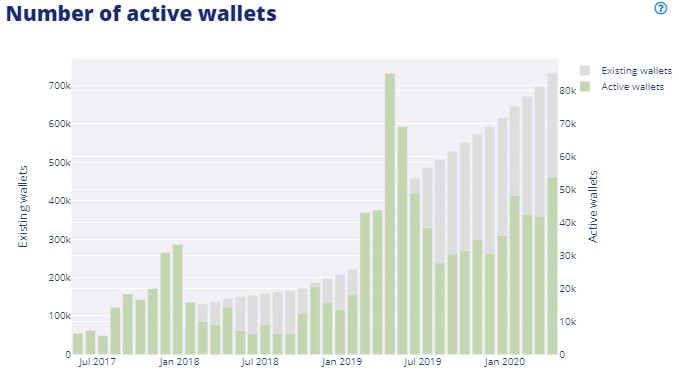

Out of any behavioral labels, more than 700k wallets have interacted with BAT tokens since its inception. Even though it appears as one of the bigger communities around a utility token, it represents only a portion of Brave’s browser active users, estimated at 13.8M at the end of April.

Around 550k of these are holding less than 10 tokens, within which Brave users who hold tokens’ compensations after having viewed advertisements.

Lately, more than 50k wallets have been active monthly, up from 7k in May 2018 (+600% growth in 24 months).

This contrasts with the 1.7M Brave’s users that are said to have an active wallet.

Information note on Brave: Brave is a privacy browser. They do not want users to be identified by on-chain transactions. In browser, wallets and transactions happen off chain. We are not able to see these transactions in our network analysis. Brave integrates with Uphold as their exchange partner. If a user withdraws or transfers their BAT from Uphold, an on-chain transaction will be recorded.

Monthly on-chain volumes are back around the 1B tokens level lately, with a transaction’s mean value around 10k tokens. With more than 100k transactions performed each month recently, Brave network is on its way to achieve a new activity ATH by the next few months.

Data and insights provided by Nyctale (nyctale.io).