Click here to join the Our Network telegram chat.

Welcome to Issue #22 of Our Network, the newsletter about on-chain analytics that reaches almost 2000 crypto investors every week.

This week our contributors are back covering DeFi:

0x

dYdX

Kyber

Uniswap

WBTC

I am an active DeFi investor and user myself, and something I have been thinking a lot about lately is just how quick this ecosystem is maturing. It’s a lot faster than people realize. A year ago, I would have agreed with many of the skeptics who said this is a space for hobbyists and tinkerers. But fast-forward to today and the signs that we are crossing that chasm to mainstream adoption are becoming evident:

And the list goes on…

As one of my favorite DeFi investors put it to me recently: “The reason there is close to $1 billion in DeFi [and billions in stablecoins] is not because users are playing around. It’s because they are making serious money.”

I couldn’t agree more.

-Spencer

Network Coverage

🟢 WBTC

Contributor: Alex Svanevik, co-founder of Nansen and D5

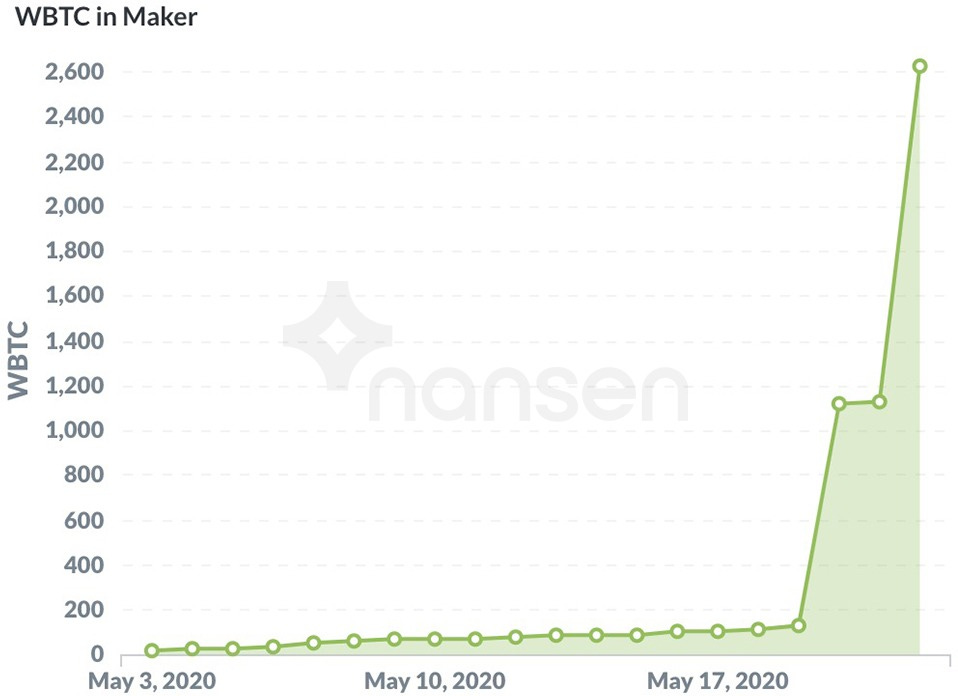

Earlier this week, Nexo took the final step and locked up their remaining 997.4 WBTC (~$9.2m USD) in Maker, as expected. And just yesterday, Nexo minted another 1.5k(!) WBTC - beating their last record. This latest mint ultimately made it into Maker as well. The result is a massive spike on the "WBTC in Maker" chart:

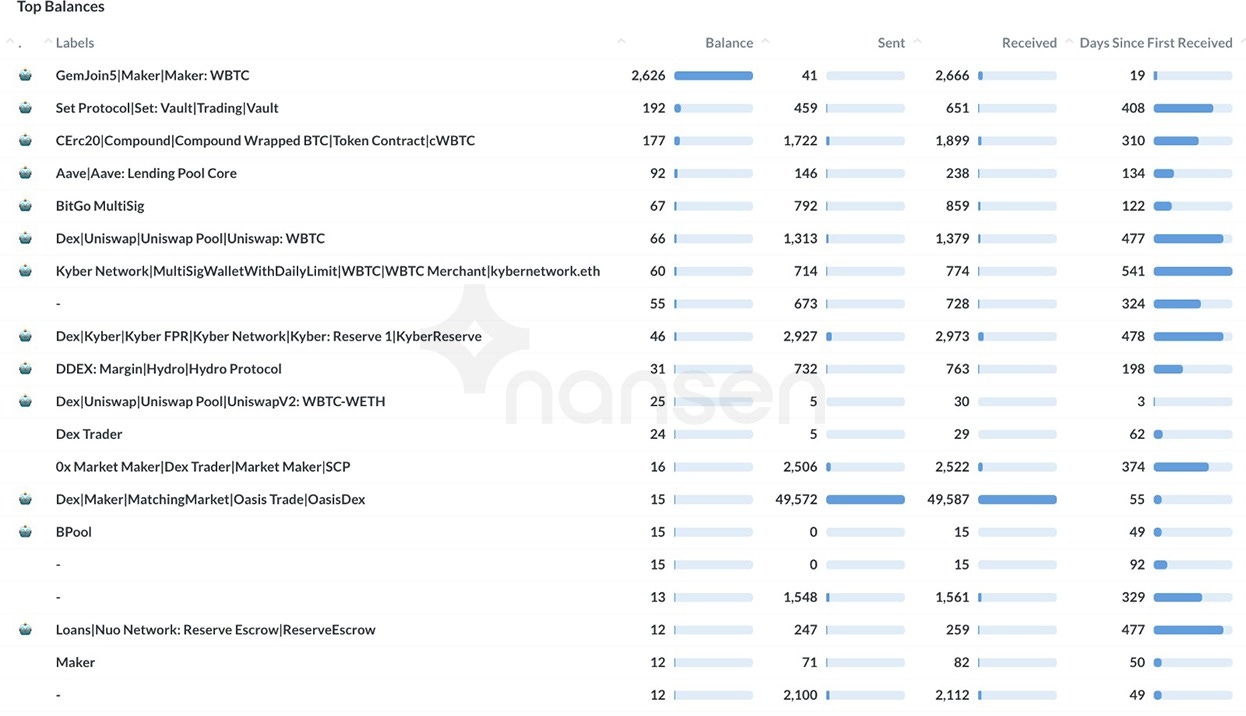

These transactions place Maker firmly at the top of the list of WBTC-holding addresses. The Maker WBTC contract now has a balance of 2,626 Wrapped Bitcoins, almost 14x higher than #2 on the list (Set Protocol). As you can see in the table below, WBTC is predominantly held by DeFi-related contracts.

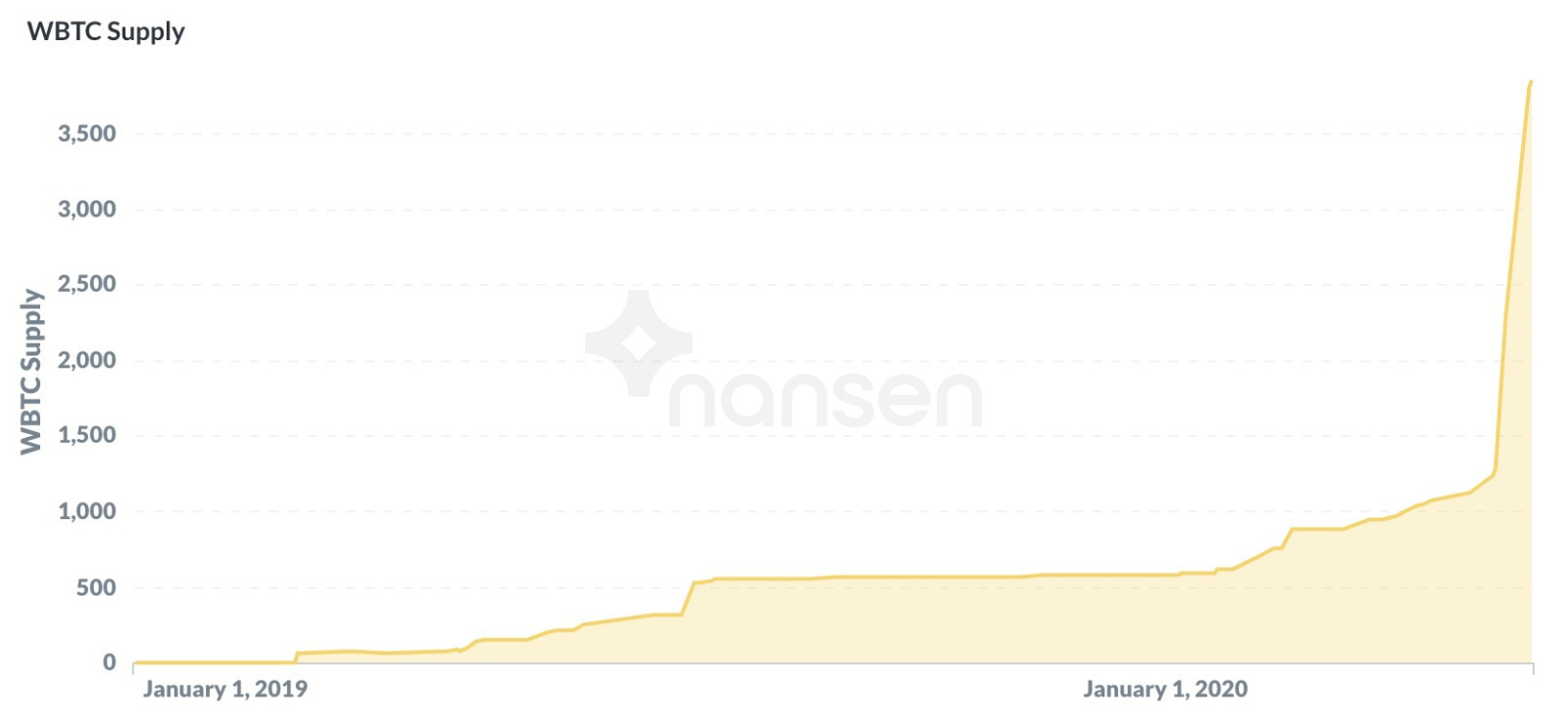

In fact, 68% of the total WBTC supply is now locked in Maker! The chart below shows the total WBTC supply over time - currently at 3,851 WBTC:

Finally, the DAI minted against this WBTC has maxed out the debt ceiling for WBTC. At the time of writing, it's sitting at ~95%.

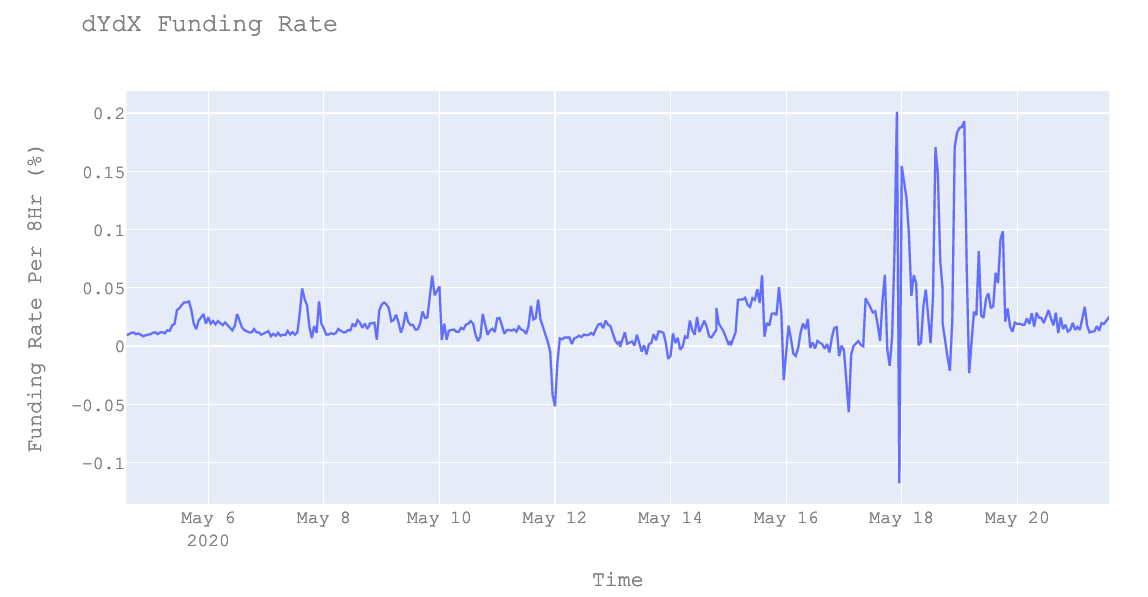

🟢 dYdX

Contributor: Brock Elmore, Co-Founder of Topo Finance

dYdX recently launched their BTC perpetual contracts. These contracts operate on the Ethereum blockchain and this system is the first non-custodial way to get exposure to BTC price movements in the Ethereum DeFi ecosystem. It was in private beta prior to launching publicly on May 13th. The protocol offers up to 10x leverage. Since launch, the protocol has seen good volumes, with daily volume exceeding $12M in a single day of trading. That pushed dYdX to the top of DEX volume.

Average trade size is always a good metric for an exchange. dYdX shines here with liquidity from their off-chain orderbook/on-chain settlement system. Post-launch, they saw average trade sizes of up to $7k.

Trades per day naturally follows volatility, but dYdX has seen on average around 400 trades per day since launch.

Perpetual contracts use a funding rate to help balance longs/shorts to minimize risks in case of a large market move. This works similarly to BitMex, except interest is paid every second (but does not compound), unlike BitMex where they sweep funds earned every 8 hours. This rate is quoted at an 8-hour return percentage. During high volatility, the book was unbalanced (predominantly long) so you could earn 0.2% in 8 hours if you were willing to go against the market. One twitter user suggested short 10x on dYdX, long 10x on BitMex to capture the funding rate arbitrage (ignoring liquidation risk here).

🟢 Kyber Network

Contributor: Deniz Omer, Head of Ecosystem Growth at Kyber

While Automated Market Makers are a great hands-off approach to supplying liquidity, they are not capital efficient when it comes to volatile assets (ie all non-stablecoins). Professional market makers have an advantage in this space as they can deploy their own unique algorithms with customized trading strategies to provide far more dynamic pricing and this reflects in the data as professional market makers with their more competitive pricing facilitate 63.5% of volume passing through Kyber.

The march of the stablecoins continues and they now make up a whopping 63.7% of all token volumes on Kyber. We see this increase in volume in non-speculative assets as a clear sign of Ethereum’s increasing adoption as a platform for decentralized finance and part of a narrative of maturing lending, borrowing, and margin trading products. A year ago stablecoin dominance on Kyber stood at roughly 40% with SAI making up most of that volume.

Kyber Network continues to attract a diverse range of dapps for their liquidity needs and in April, 71 different dapps and services pulled liquidity from Kyber. After KyberSwap’s web/iOS/Android offerings, DeFi dapps like 1inch.exchange and DeFi Saver and popular wallets including MyEtherWallet and Trust Wallet made up the largest consumers of Kyber’s liquidity last month.

1inch.exchange increased its dominance of Kyber's DeFi volumes over the last month although it must be noted that this chart excludes volumes from half a dozen other DeFi integrations (including Set Protocol) because they do not have a registered wallet address to receive protocol fees which is the primary way we calculate DeFi volumes. For the first time in over a year Fulcrum was absent from the DeFi data as the team works on an updated protocol for their relaunch.

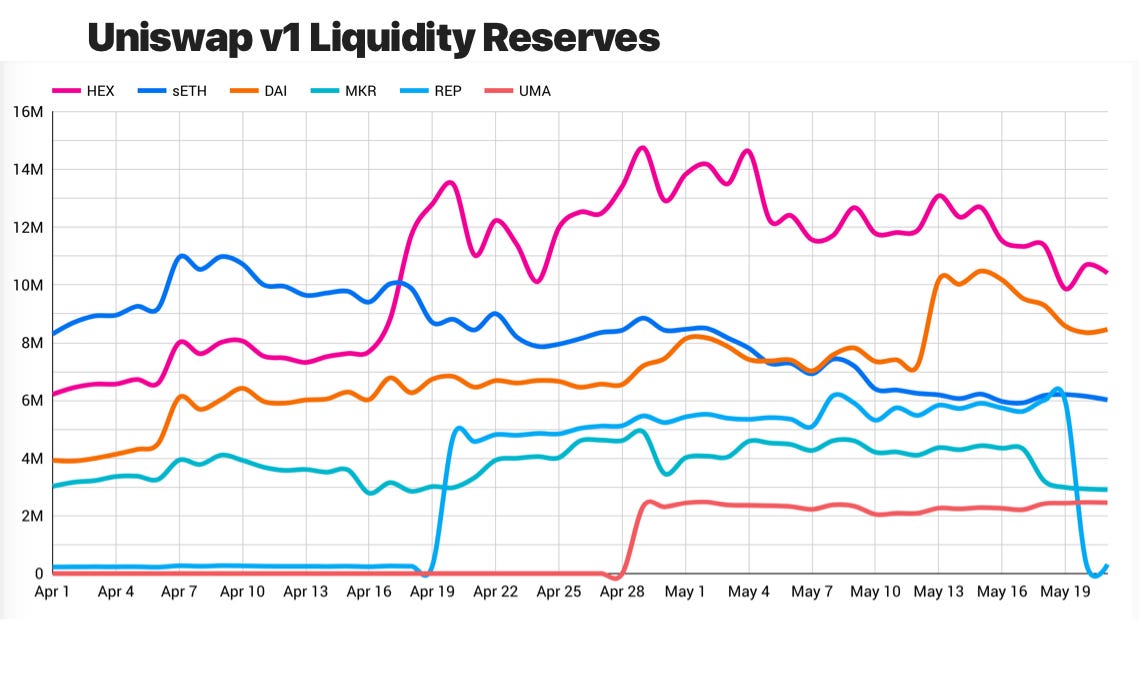

🟢 Uniswap

Contributor: Caleb Sheridan, co-founder of Blocklytics

Yesterday, Uniswap v2 launched! Congratulations to the Uniswap team! One more reason to celebrate the launch is the opportunity to see Uniswap (the platform) go through an upgrade process which Uniswap (the team) cannot force on users. There is no off switch or upgrade lever -- Uniswap v1 will run as long as there are traders and liquidity providers. So far, Uniswap v2 has attracted $11m in liquidity and $1m of daily trading volume (source).

The team's launch and migration efforts have migrated over 20% of liquidity so far. For reference, Black Thursday saw the platform's liquidity drop 13% (in ETH terms) as LPs liquidated their positions.

So far, the biggest Uniswap v2 markets are simple migrations from v1:

WETH-REP ($5M)

WETH-DAI ($1.1M)

WETH-USDC ($660K)

Uniswap v2 also allows for more exotic token to token pairs. Notably the much anticipated stablecoin markets have started to build liquidity but are far from generating meaningful volumes:

USDC-DAI ($110K)

USDC-USDT ($40K)

cUSDC-cDAI ($23K)

Since our last update in early April, Uniswap v1 has seen the following developments:

HEX became the deepest market

DAI liquidity ~doubled

sETH liquidity ~halved (likely due to new incentivization mechanisms launching)

REP received a $5M liquidity injection (which was subsequently migrated to v2)

UMA grew a $2.5M market after a very controversial IUO (Initial Uniswap Offering)

Finally, you cannot get this track on Spotify. Grammy-award-winning artist RAC released $TAPE as a limited edition good on Uniswap. As you can expect from similar limited-edition physical goods, the token's price performed extremely well increasing from $20 to a high of ~$930. RAC revealed that he has "actually been a liquidity provider for a while" (source).

🟢 0x

Contributor: Alex Kroeger, Data Scientist at 0x

In an effort to make metrics about 0x more broadly accessible, editable, and auditable by the DeFi community, the 0x core team has begun developing visualizations in Dune analytics. Dune analytics is a tool for querying a rich set of Ethereum blockchain data. The data in this post will highlight items from the 0x Staking dashboard on Dune. Check it out, fork the queries, and stay tuned for more!

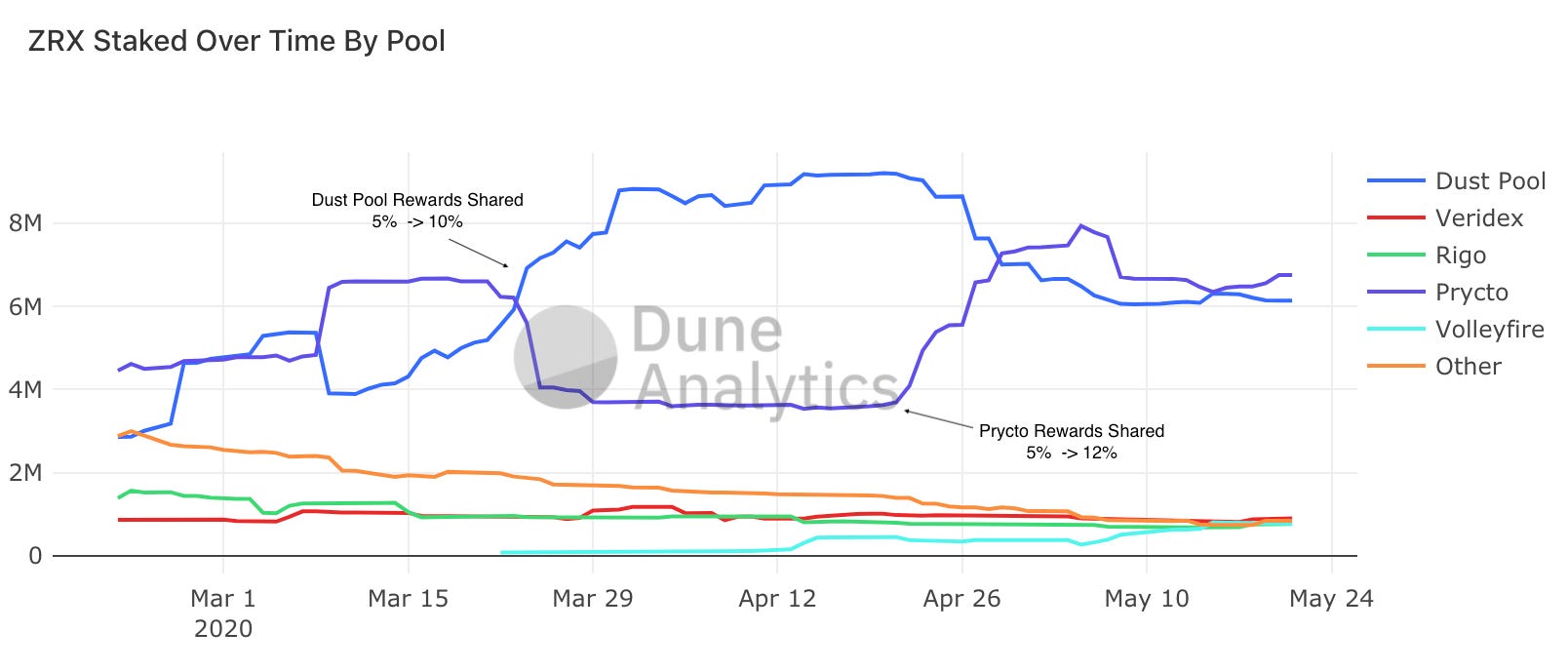

To recap previous posts, market makers using 0x receive rewards in proportion to the fees generated from fills of their orders and the amount of ZRX staked against their addresses. If the market maker does not own sufficient ZRX to maximize their payouts, they can form pools to accrue stake from other ZRX holders in return for sharing a portion of their rewards. The proportion of rewards that are shared with pool members is set by the market maker and can be adjusted upwards.

In setting the percent of rewards to share, the market maker faces a maximization problem. A larger percentage of rewards shared decreases the market maker’s share of the eventual reward pot, but it also can make their pool more attractive to potential stakers, and more ZRX staked means the reward pot will be bigger. The latter effect depends on how attractive the pool is relative to other pools, so we should expect to see pools compete on rewards shared. Indeed, we’ve seen many pools increase the proportion of rewards shared to pool members, as shown in the chart below. Of the top 5 pools, Volleyfire has set this value most aggressively at 33%.

These changes have affected the way stake is allocated across pools. Dust Pool’s increase of rewards shared from 5 to 10% on March 24 helped solidify their position as the top staked pool at the time. Likewise, Prycto’s increase in rewards shared from 5 to 12% on April 22 preceded with their re-taking of the top spot.