Our Network: Issue #17

LINK, Nexus Mutual, Stablecoins, and Lending Rates.

Interested in joining the discussion about on-chain metrics? Click here to join the Our Network telegram chat.

Welcome to Issue #17 of Our Network, a weekly newsletter about on-chain metrics and crypto analytics that reaches almost 2000 investors every week.

This week, our contributor analysts cover decentralized finance:

Stablecoins

Nexus Mutual

Lending Rates

Chainlink

I’m particularly excited for readers to dive into our stablecoin coverage because it’s a category that the crypto investor community has been quickly ramping up on over the past few months.

Stablecoins have come a long way in a relatively short amount of time. Tether minted its first batch of USDT in October 2014 (just $100!), which was just over 5 1/2 years ago. Fast-forward to today and—

What is particularly interesting is that there appears to be new use cases emerging for stablecoins other than crypto trading. Historically new minting has always been a signal that fiat was on-ramping onto an exchange in order to buy crypto (and usually BTC). However, today there are reasons to believe that may not always be the case, a topic that perhaps one of our analysts can cover in more depth soon.

Network Coverage

📌 Stablecoins

Contributor: Jai Prasad, TokenAnalyst CEO

In 2020, stablecoins have established themselves as the go-to way to transfer value on blockchains. This post looks deeper into which stablecoins are dominant and what they are used for.

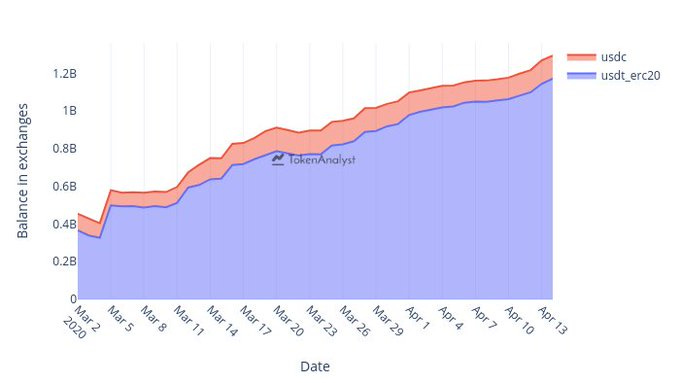

As it did in through most of 2019, Tether (on Ethereum) towers over all other stablecoins in terms of on-chain volume. Tether's daily on-chain volume on average is ~$835M compared to ~$145M for USDC; Dai comes in at third with ~$95M in daily on-chain volume

Tether is mainly used to transfer value between exchanges and to trade in and out of crypto pairs. This is evidenced by ~$1.3B of Tether sitting on exchanges wallets (just $1B alone on Binance). Explanations for this phenomenon include:

"Limit orders at exchanges, waiting for the perfect moment to buy" h/t @ankitchiplunkar

"Stablecoins are being used for more mundane purposes in response to the global shortage in US dollars" h/t @luyongxu

Additionally, the top 10 trading pairs on Binance are all USDT (Tether) pairs.

A good indicator of stabelcoin health is the number of on-chain transactions. More on-chain transactions mean more usage. Removing Tether from our analysis reveals that Dai is the most transferred stablecoin. Dai averages 15K transactions daily. Paxos (PAX) is one to watch out for. Pax started the year with ~4K daily transactions but has averaged over ~10K transactions in the last 30 days!

The main goal of stablecoins is to minimize price volatility. Looking at the price of various stablecoins paints a troubling picture. GUSD has been nowhere close to it's $1 peg in 2020, and Dai has moved away from it's peg since mid-March. Given DAI's pivotal role in decentralized finance, the Dai price is something to keep a close eye on.

📌 Nexus Mutual

Contributor: Richard Chen, Partner at 1confirmation

In the last month, 3672 ETH ($625k) was contributed to the capital pool, bringing the total capital pool size to 16735 ETH ($2.85M).

The advantage of the mutual model for insurance is that Nexus can be undercollateralized (by up to 5-6x right now) and thus capital efficient. In other words, for every dollar contributed to the capital pool, Nexus can underwrite $5-6 in cover that's diversified across different smart contracts. So a $625k growth in capital pool size in the past month translates to up to $3.75M in additional smart contract cover capacity.

The increase in capital pool size also increases the price of NXM. The graph below shows the NXM price denominated in ETH. For context, NXM outperformed ETH by 10% in the past month.

In the next month, Nexus will launch pooled staking, making it easier to earn staking rewards that are paid from the premiums of smart contract covers. More stake on a smart contract also decreases the premiums for covers on that smart contract. So far the most profitable contracts to stake on are dYdX, Compound, MakerDAO, Flexa, and Uniswap.

For more data see: nexustracker.io

📌 Lending Rates

Contributor: Lucas Campbell, Growth at DeFi Rate

In mid-March, Black Thursday caused a significant amount of volatility in DeFi lending markets and crypto at large. Dai lending rates on dYdX and Compound went wild as there was a massive demand for Dai amid the liquidity crisis. The volatility in crypto markets also resulted in the Maker Protocol dropping the Dai Savings Rate (DSR) down to zero percent. Since then, Dai lending rates have experienced a steep downturn as lending rates across DeFi protocols struggle to offer anything substantial relative to historical yields.

As it stands today, crypto bank CoinList offers the highest rate on Dai at 2.4% APY. Major protocols like Compound are offering 0.44% APY on Dai while dYdX and Aave offer 1.79 and 1.21%, respectively. One of the more interesting things to note with Dai lending rates is Nuo’s “step-ladder” decrease in rates over the past 30 days. The India-based DeFi lending platform offered significantly higher rates relative to other lending markets as its 30 Day average on Dai was a lofty 16.94% APY (compared to 0.34% today).

The one silver lining with the DSR at 0% is our ability to better understand the risk premiums across different lending platforms. For those unfamiliar, the risk premium is a simple formula in traditional finance for calculating risks across different investment opportunities. Specifically, the risk premium is calculated by subtracting the expected return from the risk-free rate (i.e. the DSR).

Although the DSR is not technically “risk-free” today, it does serve as a useful proxy against which to measure the risk/return for other lending rates offered on the market. Looking at the 30 Day average lending rates relative to the DSR, it’s obvious that Nuo’s high-yielding average of 16.97% may present some concerns given the rates offered on the rest of the market. In comparison, lending protocols like Aave, Compound, and dYdX all boast moderate risk premiums of 1.99%, 2.28%, and 3.55%, respectively.

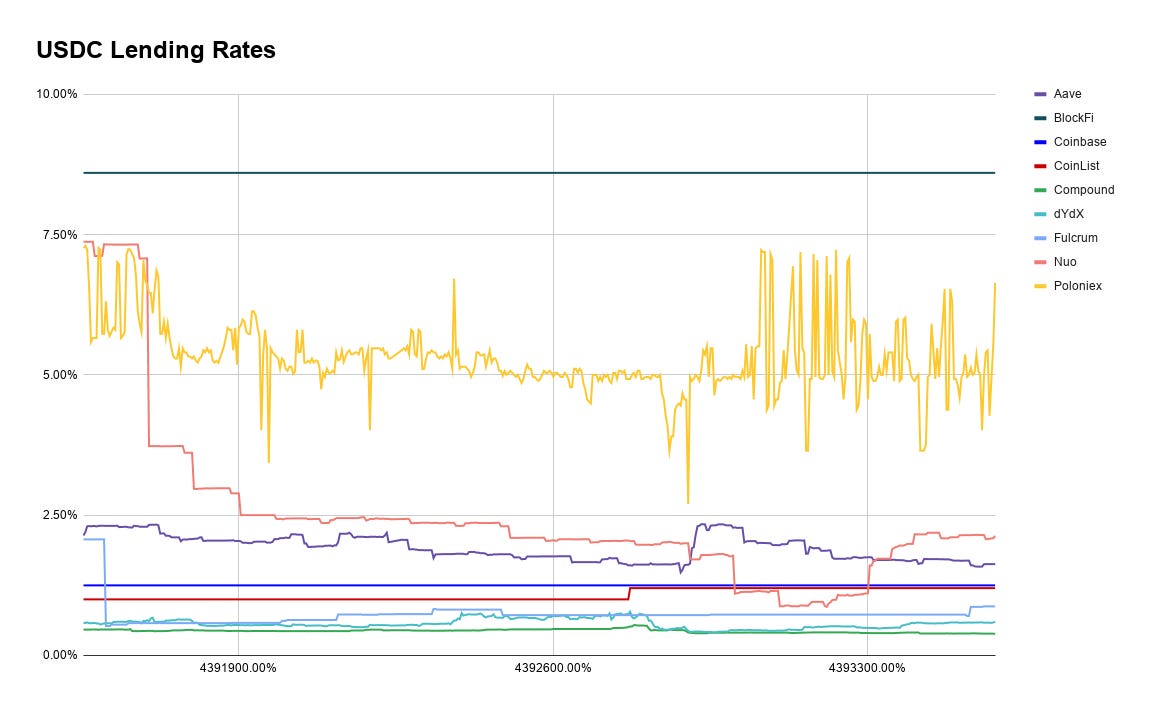

While it was apparent that the DSR was one of the main drivers behind Dai lending rates, it seems that the DSR also has an effect on USDC lending rates. Since Maker lowered the savings rate to 0%, USDC lending rates have also taken a hard hit. Centralized crypto banks like BlockFi and Poloniex are still offering high-yielding rates like 8.6% (BlockFi) and 5.63% (Poloniex), however, DeFi lending protocols are struggling to offer anything attractive. The 30-Day average lending rate on USDC for Compound is 0.43% while dYdX offers 0.56% APY. Other lending platforms like Aave and Nuo offer more attractive yields at 1.89% and 3.97%, respectively.

In terms of USDC risk premiums, we’ll still assume that the rate offered by the issuing entity, Coinbase (1.25% APY), acts as the risk-free rate for USDC lending rates. Again, although it’s not really “risk-free” it does serve as a good proxy for the rest of the market. That said, the two centralized crypto banks - BlockFi and Poloniex - have the highest risk premiums of 7.35% and 4.38% respectively. Some DeFi lending protocols are boasting negative risk premiums like Compound (-0.82%) and dYdX (-0.69%) indicating increasing usage and trust in permissionless lending protocols. However, given the recent correlation between USDC lending rates and the DSR, there’s an argument that the DSR could act as the “risk-free rate” for DeFi stablecoins at large. In the coming months, we’ll continue to explore this correlation in an effort to further expand our understanding of DeFi lending markets.

📌 Chainlink

Contributors: ChainLinkGod and CryptoSponge

An important metric of health for any protocol that uses a token is how many new on-chain contracts are utilizing the token. Below, this graph shows the number of new Chainlink related smart contracts on Ethereum mainnet each week by tracking how many new contracts have received LINK (Chainlink’s native token) for the first time. This activity can range from DEX listings and dApp support for LINK to new oracle contracts (new nodes), new aggregator contracts (new oracle networks), and more.

Initially just after the token sale in late 2017, there was a small but healthy amount of new contract activity of 10-50 new contracts a week, but then later dropped to nearly zero for all of 2018 and the beginning of 2019 as the crypto markets turned bearish with only 1-11 new contracts a week. Growth only began increasing around Chainlink’s mainnet launch in May 2019 where it reached a peak of 199 new contracts a week in 2019. In 2020, new peaks have been made with the highest reaching 357 new contracts a week (a growth of ~32x a week compared to the 2018 dryspell).

It’s important to note this graph only tracks new Chainlink-related contracts and doesn’t take into account current existing contracts using LINK.

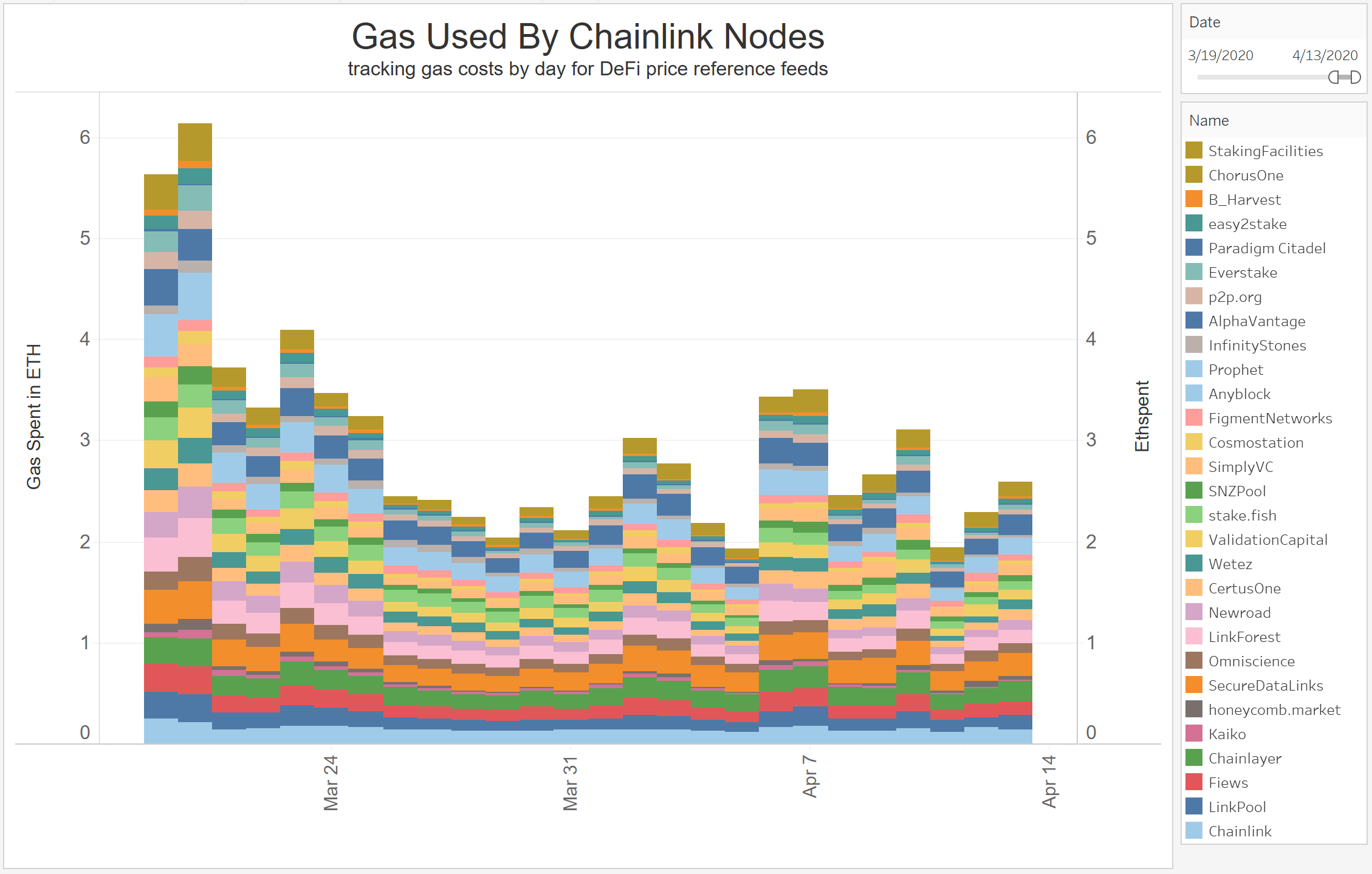

Total gas consumption is an interesting metric to track as it shows how much each active Chainlink node spends in ETH each day in order to pay for Ethereum blockspace to ensure their transactions with the requested data get processed and confirmed on-chain in a timely manner. This chart below shows how much ETH was spent on Ethereum transactions during each of the past 26 days. The average gas price paid by these nodes was around 9 Gwei.

The reason for the fluxuations in ETH spent each day is not only due to changes in Ethereum gas prices, but it is also because many oracle networks update not just on a heartbeat schedule (eg every hour) but also on a deviation schedule (eg every 1% change). More volatility in market prices means more oracle updates need to be processed on-chain. This means nodes will get paid more LINK but they will also need to spend more ETH to pay for the gas required to process response transactions. Also, the more ETH spent for a given transaction, the less profit a node earns as more of their LINK payment is used to cover gas expenses.

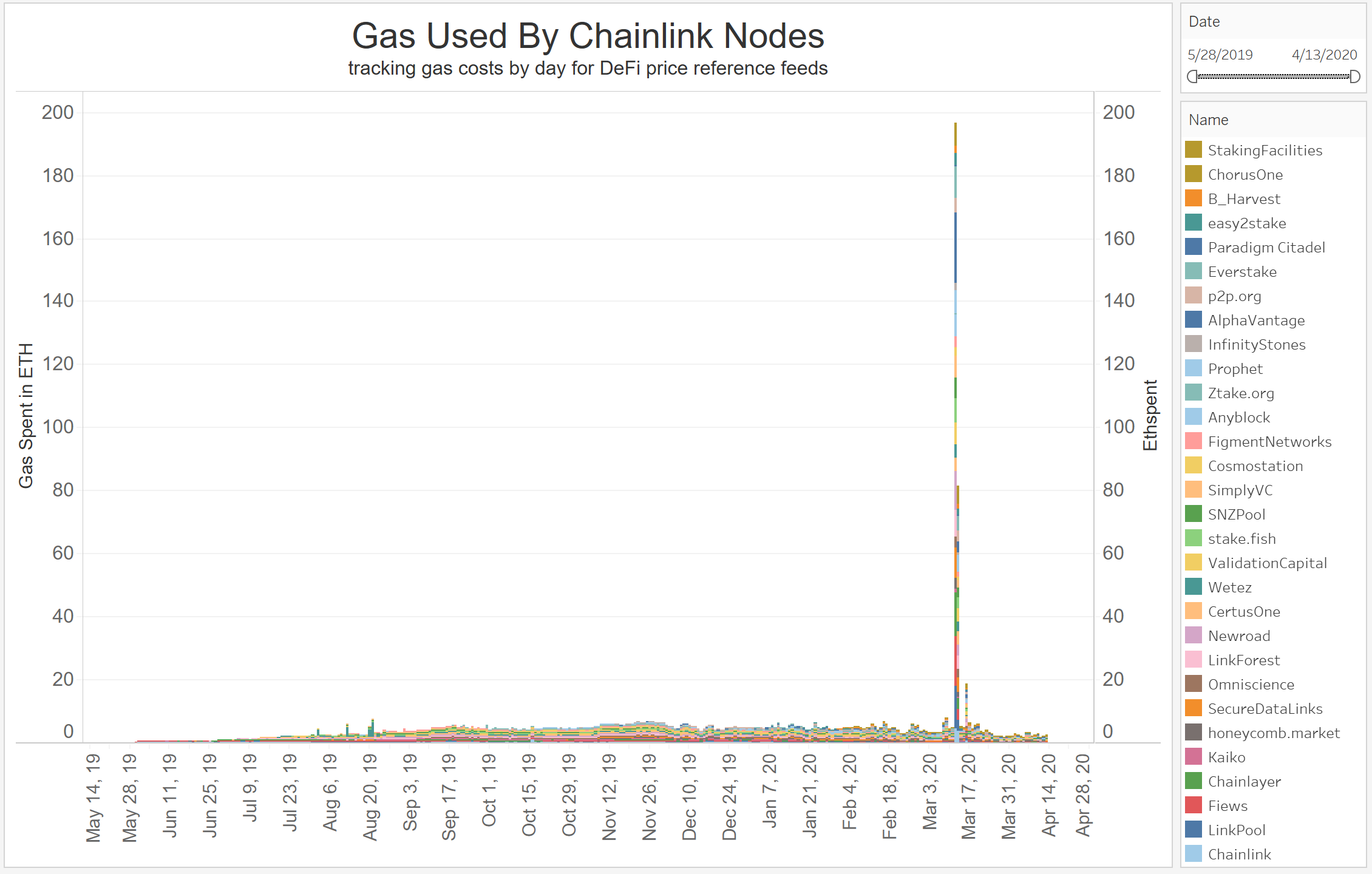

This second gas consumption chart is when things get really interesting. As you may know, on March 12th a black swan event happened in the DeFi space. During the global financial panic in the equities markets caused by Coronavirus fears, the cryptocurrency market cratered just as well. In particular this caused the ETH price to drop nearly 50% in value causing a massive cascade of on-chain liquidations and flurry of DEX arbitrageurs bidding up the gas price to extreme levels (as these liquidations/trades were still profitable at these gas prices) and congesting the overall Ethereum network. In order to get transactions to confirm on the Ethereum network, Chainlink nodes paid gas prices in excess of over 250 Gwei.

This is visualized as a large irregular spike on March 12th where the total ETH spent on gas that day from all active Chainlink nodes went from just ~6 ETH a day to nearly 200 ETH (33x spike). This was due to the extreme rise in gas prices, but also from the onslaught of countless oracle update requests due to volatile market prices (some price feeds had a deviation of 0.5%).

A good way to measure token liquidity is by tracking how much LINK is stored on high volume exchanges. In the early days of 2017, trading occurred mainly on the EtherDelta DEX, but later that year Binance listed LINK and captured the vast majority of its liquidity. Binance’s monopoly on LINK trading markets lasted from late 2017 to mid 2019, after which Coinbase listed LINK and funds started to transition over.

During this monopoly period, Binance steadily held between 110M to 125M LINK tokens (31% to 35% of the circulating supply), but sharply decreased to 100M LINK (28% of circulating supply) in June 2019 with the Coinbase listing. Afterwards, Binance’s holdings of LINK continued to drain outwards due to user withdraws over the next ten months down to where it is today at 70M LINK (20% of the circulating supply).

Coinbase’s holdings on the other hand have continued to grow from the initial 20M to now 70M LINK tokens (5% to 20% of the circulating supply). Binance and Coinbase together now account for over 40% of the circulating supply of LINK. LINK’s distribution across the two exchanges have just recently come to parity with each other with both exchanges holding 70M LINK. It should be noted however Coinbase does not make their wallet addresses public, so this information was aggregated by tracking particular wallets that exhibited identical robotic accumulation behavior which started at the same exact time as the Coinbase listing.

Subscribe to Our Network for free crypto insights every week:

About the editor: Spencer Noon leads investments for DTC Capital, a fundamentals-focused crypto fund. He actively tweets about on-chain metrics.