📝 Editor’s Note:

Welcome to OurNetwork's latest issue covering DePIN, a subsector of crypto that arguably hasn't entered the mainstream, but has diehard proponents who think that it's only a matter of time before that changes.

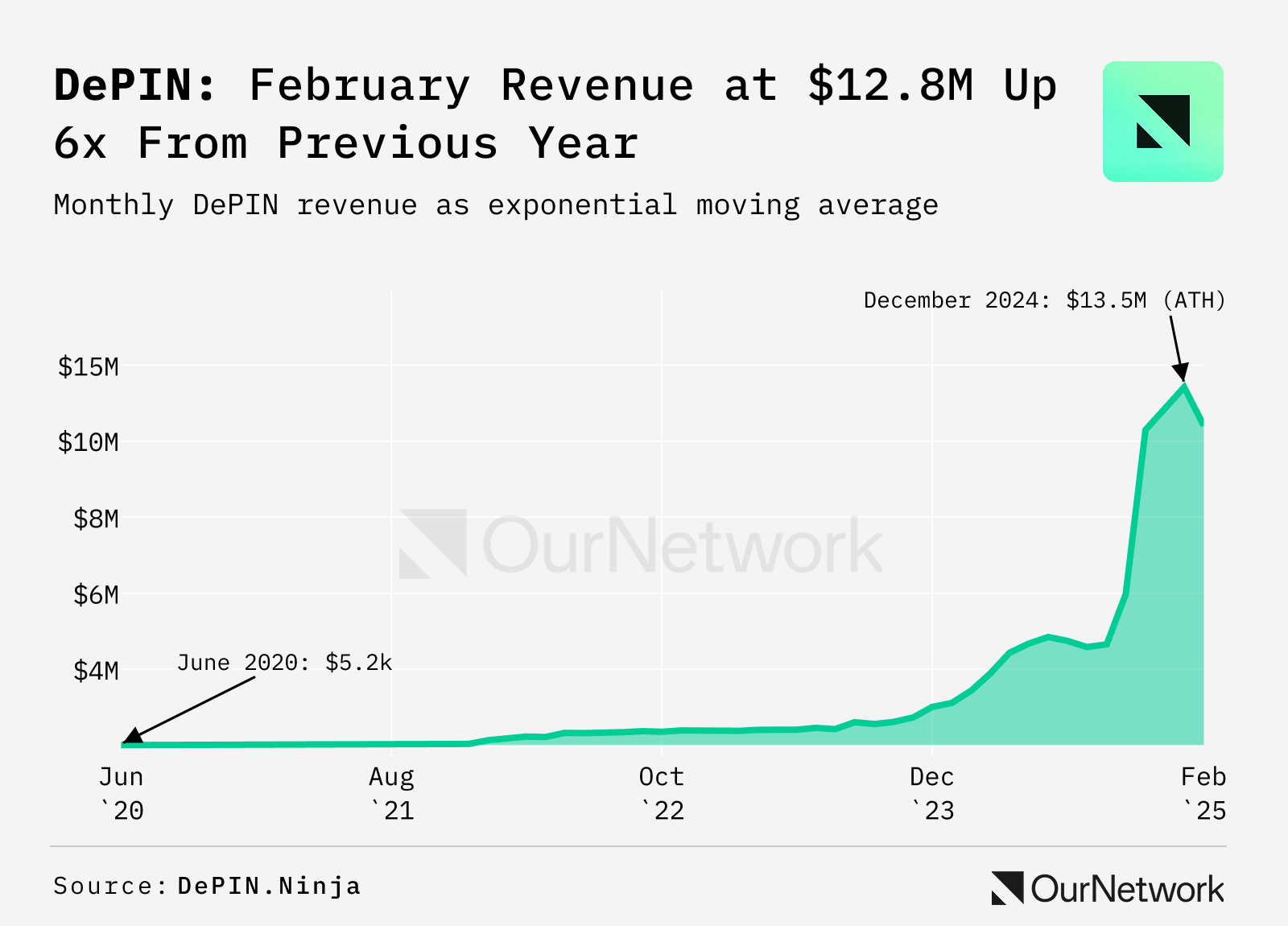

There's evidence that DePIN is poised for broader adoption — the sector’s revenue hit a high of $13.5M in December, according to DePIN.Ninja.

To dig deeper into the sector we've fielded an overview from Salvador Gala, co-founder of EV3, the DePIN-focused investing and research firm. We also connected with Joe Bender of DIMO, Doug Petkanics of Livepeer, and Zoey Zhang of GEODNET for network-specific coverage.

– ON Editorial Team

DePIN 🛜

Sector Update | DIMO | Livepeer | GEODNET

👥 Salvador Gala | Dashboard

📈 New DePINs are Trading Significantly Below their Token Generation Event Price — and Even VC round — Valuations, While Old DePINs are Growing Revenues Faster than DeFi.

An analysis of 20 DePIN token generation events (TGEs) in 2024 and 2025 year-to-date found that only the top 10% — 2 of 20 — are currently trading above the TGE price. Half the group has actually had the token price decline by over 50% since TGE. A third — 7 of 20 — are trading at below $30M fully diluted value (FDV), almost certainly below VC round valuations. The two DePINs whose price is up from the TGE, Grass and Auki, have not yet disclosed onchain revenue statistics.

✏️ Note: TGE price is defined here as the token price after the first $500k in trading volume.

The top revenue-generating projects are proving that DePIN onchain revenues are more resilient than the rest of crypto. GEODNET, Helium and Akash have all already grown revenues significantly from their monthly 2024 peak, while Layer 1s and DeFi revenues are down -50% or more on average from their monthly 2024 peak.