EXCLUSIVE ONCHAIN COVERAGE:

Stablecoins 💰

👥 Kyle Waters

📈 Tether share over 2/3 for the first time in 2 years

🔗 Website | Jobs | Dashboard

The $120B+ stablecoin market has undergone significant changes in 2023, catalyzed by a bumpy regulatory environment and new challenges brought on by the US banking sector. Since the beginning of the year, the market cap of Tether (USDT) has risen $17B from $64B to $81B—an all-time high—pushing USDT’s market share to 67%. Meanwhile, USDC supply has fallen from 40B to 27B since the collapse of SVB, while BUSD supply is down to just 5B, falling from 16B at year-start.

Looking at total supply by address size shows that the lion’s share of stablecoins (92B) are still held by large addresses (exchanges, DeFi protocols, bridges, whales) with >1M in supply. Most of the supply being shed this year has come from the top, with this segment of the market falling by 12B.

At the same time, the amount of daily burnt and issued supply has fallen recently, with an average of 250M units being burnt/redeemed daily, and 170M units being issued daily. The decrease in turnover comes amid ongoing challenges in crypto on/off-ramps to the fiat banking system.

② crvUSD (Curve)

👥 nagaking

📈 crvUSD launch sees initial growth and price stability

🔗 Website | Dashboard

Curve Finance recently launched crvUSD, a crypto-backed stablecoin that offers "soft" liquidation and de-liquidation to borrowers. In contrast to typical crypto-backed stablecoins, crvUSD uses a novel AMM mechanism to gradually trade between crvUSD and crypto collateral, allowing for smooth transitions between liquidated and "de-liquidated" states. Over ~1 week, crvUSD approached its initial "debt ceiling" of 10M crvUSD (left), and amassed significant liquidity in its stabilizer pools (right).

Over the initial ~1 week since launch, crvUSD has adhered closely to its $1 peg. Prices have largely remained within a narrow range between $0.996 and $1.004. (Left) Timeseries of hourly prices since contract launch; (Right) Histogram of hourly prices (bin size = $0.001).

Example liquidity distribution for the LLAMMA (lending-liquidating AMM algorithm) market-maker underlying the crvUSD/sfrxETH lending market (block 17388685). As the price traverses each band, LLAMMA shifts its holdings between sfrxETH and crvUSD, allowing for smooth liquidation and de-liquidation.

③ Dai (Maker)

👥 Vishesh Choudhry

📈 Dai is now 38% backed by RWA vaults

🔗 Website | Jobs | Dashboard

Dai supply has fallen below $4.8B. Of this, ~$1B comes from ETH & staked ETH vaults, ~$1.6B from PSM/Stablecoins, ~$1.8B from Real World Asset vaults, including the recently added $500M Dai coinbase custody vault. There is additionally ~$43M from CRV stETH/ETH, ~$95.6 from WBTC, $20M from RETH, and 5M from the recently launched Spark protocol. This means that ~$63M of Maker's ~$92M annual projected fees come from RWA vaults, $10M from PSM-GUSD, ~$19M from onchain collateral.

MakerDAO signaled its desire (99.9% Yes) to change a number of risk parameters, including large increases in the fees for onchain collateral-backed vaults (ETH,stETH,rETH,WBTC, etc) ranging from ~3.5% to ~6%. Conversely, MakerDAO has also signaled a desire to increase the Dai Savings Rate to 3.49%.

Over the past 3 months, according to makerburn.com, the average monthly protocol expenses for MakerDAO have risen to ~$5M (~$4M in Dai and ~$1M in MKR). Using makerburn's projected revenue estimate of ~$92M, minus the current rate of expenditure, would yield ~$32M in annual protocol profit.

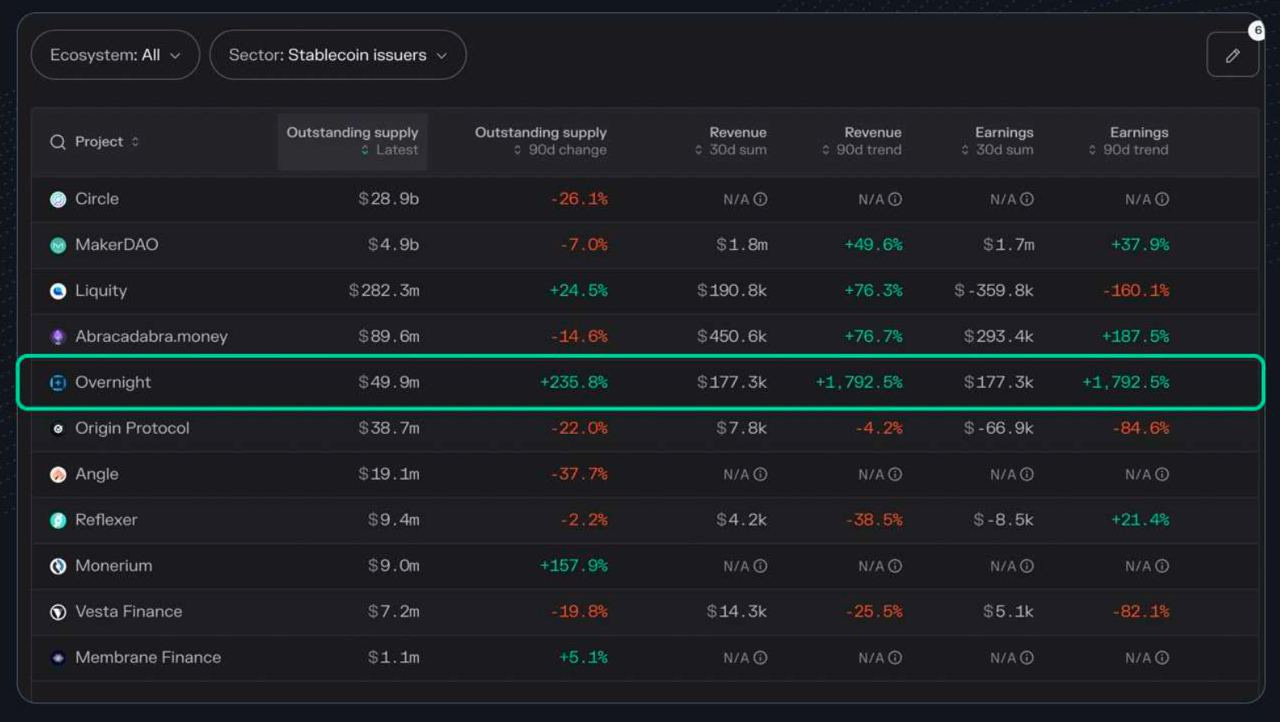

④ USD+ (Overnight)

👥 Max Ermilov

📈 Overnight exceeds 50M TVL and 170K monthly revenue

🔗 Website | Dashboard

Overnight, the protocol behind yield-bearing stablecoin USD+. The protocol is currently live on Arbitrum, Optimism, BNB Chain, zkSync, and Polygon, and has exceeded 50M TVL organically (i.e. pre-TGE, with no rewards). USD+ is fully collateralized backed mostly by delta-neutral strategies. The yield comes from collateral that's deployed onchain in fully transparent contracts. The protocol’s collateral value is marked-to-market with Chainlink oracles daily and its profit is passed to users via rebase daily as well.

Per TokenTerminal, Overnight's 30-day revenue has exceeded 180K USD (~2.2M annualized). Overnight's revenue comes from a fee retained from the yield generated by its delta-neutral strategies and skimming rebase from USD+ liquidity pools.

Finally, relative to peers, Overnight has also seen strong growth in terms of revenue (both 30d and 90d). Note: this revenue is organic, i.e. achieved prior to issuing a token that could be used for incentives.

Quick Links: Disclosures